Key Stats for Pfizer Inc.

- 52-Week Range: $23.11 to $28.75

- Current Price: $24.80

- Street Mean Target: $28.79

- Market Cap: ~$138 billion

- Dividend Yield: 7.1%

- Q1 2026 Revenue: $14.5 billion, up 5% year-over-year

- Q1 2026 Adjusted EPS: $0.75, down 18% year-over-year

- Q1 2026 Launched and Acquired Products Revenue Growth: 22% operationally

- Full-Year 2026 Revenue Guidance: $59.5 billion to $62.5 billion

- Full-Year 2026 Adjusted EPS Guidance: $2.80 to $3.00

Value your favorite stocks like Pfizer with TIKR’s Guided Valuation Model (It’s free) >>>

A Slow Grind Lower That Has Nothing to Do With Q1 Results

Pfizer (PFE) is not having a dramatic 2026. The stock is not down 40% due to a blow-up quarter or a failed drug trial. It has simply been selling off steadily, grinding from near its 52-week high of $28.75 in early April to a 17% drawdown on June 25, and sitting about 15% off that high today.

For a company of this size and stability, it is a meaningful decline, and the driver is not recent news. It is a slow reset in investor expectations about what Pfizer’s earnings power actually looks like now that the COVID windfall is behind it.

The Q1 results themselves were not the problem. Revenue of $14.5 billion came in ahead of expectations, and Pfizer reaffirmed its full-year guidance for both revenue and adjusted EPS. Excluding Comirnaty, the COVID vaccine, and Paxlovid, the COVID antiviral, revenue grew 7% on an operational basis.

Products launched and acquired since the Seagen deal grew 22% operationally. CEO Albert Bourla struck a confident tone: “I’m particularly encouraged by what we’re seeing in oncology and obesity, two areas where I believe Pfizer is positioned to lead.”

The company is also investing $2.5 billion per quarter in R&D, with around 20 pivotal studies planned for 2026. None of this is the profile of a business in distress. What the market is struggling with is simpler: how much should you pay for a pharmaceutical company whose peak earnings are almost certainly behind it?

See analysts’ growth forecasts and price targets for PFE (It’s free) >>>

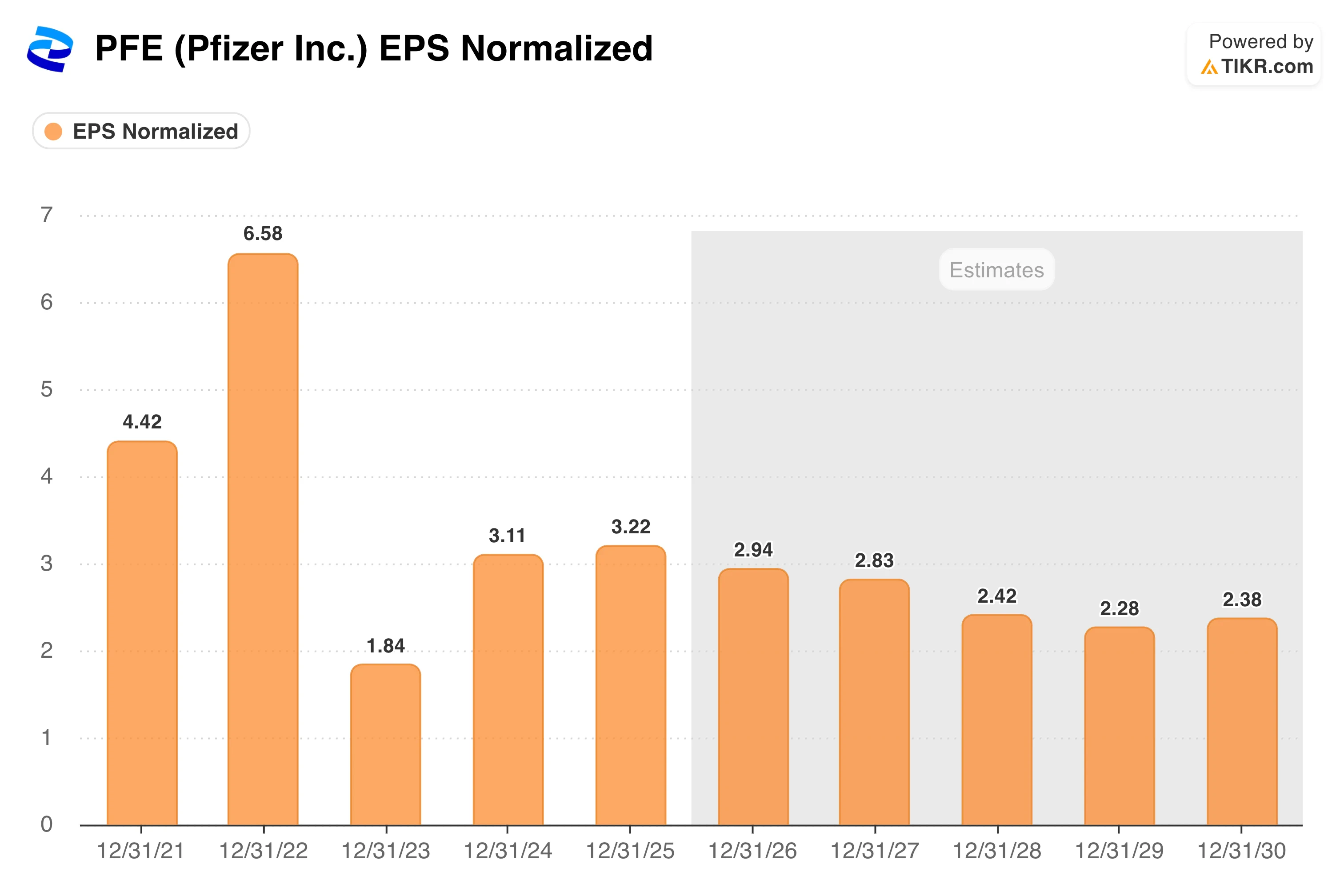

The EPS Chart Shows the Whole Story in One Picture

Few charts tell an investment story as cleanly as Pfizer’s normalized EPS history. The bars below show a company that earned $4.42 per share in 2021, then $6.58 per share in 2022 as Comirnaty and Paxlovid revenues flooded in, and then collapsed to $1.84 per share in 2023 as COVID demand evaporated almost overnight.

The partial recovery to around $3.22 in 2025 reflected the early contribution of acquired assets and cost cuts. And then the forward estimates show the next chapter: a gradual step down to roughly $2.94 in 2026, stabilizing around $2.30 to $2.40 through 2029 and 2030.

The shape of this chart is the core debate about PFE stock. Bears read it as a company in structural decline, with a dividend that currently costs more to sustain than the company earns on a reported basis, a payout ratio above 130%, and no clear catalyst to return EPS to pre-COVID levels.

Bulls read it differently: strip out the COVID windfall years entirely, and Pfizer’s underlying earnings power of $2.30 to $3.00 per share is actually close to where it was in 2020 and 2021, which means the business has not fundamentally deteriorated.

The oncology pipeline, including Padcev, which grew 39% in Q1, Lorbrena, up 32%, and Elrexfio, up 34%, alongside an emerging obesity platform, provides a credible set of growth drivers that consensus may be underweighting.

The critical question is timing. Pfizer has more than $51 billion in net debt following the Seagen acquisition, which limits financial flexibility and continues to put pressure on the dividend coverage ratio until earnings recover.

Estimate a company’s fair value instantly (Free with TIKR) >>>

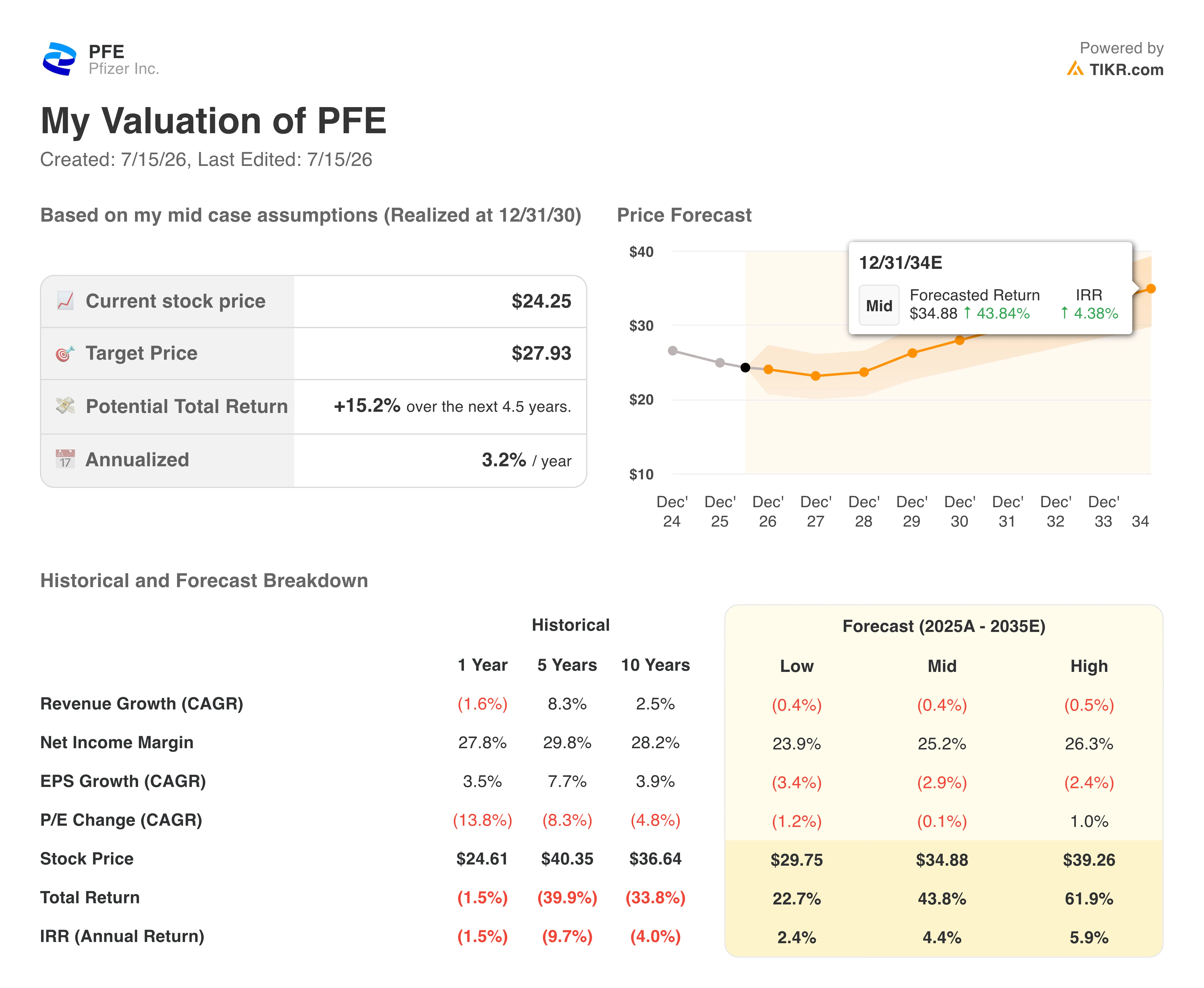

What the Valuation Model Says About a Stock at a 7% Yield

The TIKR valuation model puts a mid-case target of around $28 on PFE, implying roughly 15% total return from today’s price over approximately 4.5 years, or about 3% annualized. The low case yields an IRR of roughly 2%, while the high case approaches 6% annually.

It is worth being direct about what these numbers mean. A 3% annualized mid-case return is not a capital appreciation thesis. The model assumes flat-to-slightly negative revenue growth and declining EPS across all three scenarios, with the P/E change contributing almost nothing.

The return is essentially the dividend yield minus slippage, with a modest price target based on a stabilizing multiple applied to a lower earnings base. The scenario range is narrow and skews only modestly to the upside, reflecting the limited consensus on how quickly the pipeline can offset the COVID-era earnings cliff. For investors who need growth, Pfizer at current prices is a difficult pitch.

For income-oriented investors with a longer horizon and a view that the oncology and obesity pipeline is undervalued by the Street, the 7% yield at a below-market multiple is a more interesting conversation.

Should You Invest in Pfizer Inc.?

Pfizer is a company with a credible pipeline, a 7% dividend, and a stock trading near multi-year lows on a valuation basis.

The core challenge is that the path back to meaningful earnings growth requires oncology and obesity drugs to deliver at scale, while COVID product revenues continue to decline and debt levels constrain capital allocation flexibility.

The TIKR model’s mid-case return of around 3% annualized is honest: this is primarily an income stock with optionality on the pipeline, not a growth stock in recovery. Use TIKR to track adjusted EPS trends, Padcev and Lorbrena revenue trajectories, and any updates to the obesity pipeline heading into the Q2 report.

Build your own Pfizer valuation model in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!