Key Takeaways:

- Intel runs two businesses at once, designing its own chips and manufacturing chips for others, and each half needs to be judged on its own terms before calling this stock cheap or expensive.

- CFO David Zinsner says Intel’s newest 18A manufacturing process is improving yields by about 7% per month and is running roughly a quarter ahead of its internal targets, with the next node, 14A, already tracking ahead of where 18A was at the same stage.

- The real test is whether outside customers actually commit money to Intel’s factories, and early signs, including a Foxconn rack partnership and customers prepaying for scarce packaging materials, suggest interest is turning into real business.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Intel (INTC) stock has jumped close to 350% in the past year. That kind of move usually means one of two things. Either a real turnaround is underway, or the market got ahead of itself.

For a company like Intel, the honest answer is both possibilities are still on the table. This isn’t a simple growth stock story. It’s a company betting its future on two businesses succeeding simultaneously.

Sorting out which one you’re getting requires understanding what Intel actually does, and what would need to go right for the bet to pay off.

See what analysts think about INTC stock right now (Free with TIKR) >>>

Intel is really two companies wearing one ticker

Most chip companies do one job. They either design chips, like Nvidia, or they manufacture chips for other companies, like TSMC. Intel does both.

That’s the old Intel model. What’s changed is that Intel now wants to open its factories to outside customers too, essentially becoming a landlord for other chipmakers’ designs while still building and selling its own processors.

Intel CEO Lip-Bu Tan has called this a full-stack approach, and it depends on winning back the trust of customers who left Intel’s factories years ago.

This matters because a design business and a factory business behave nothing alike financially. Design businesses can carry high margins with light capital spending.

Factory businesses need enormous, continuous investment before they ever turn a profit. Judging Intel with one blended number hides more than it reveals.

Why valuing Intel as one business misleads investors

A company mid-turnaround can look cheap on trailing numbers and expensive on forward numbers at the same time, and Intel is a textbook case.

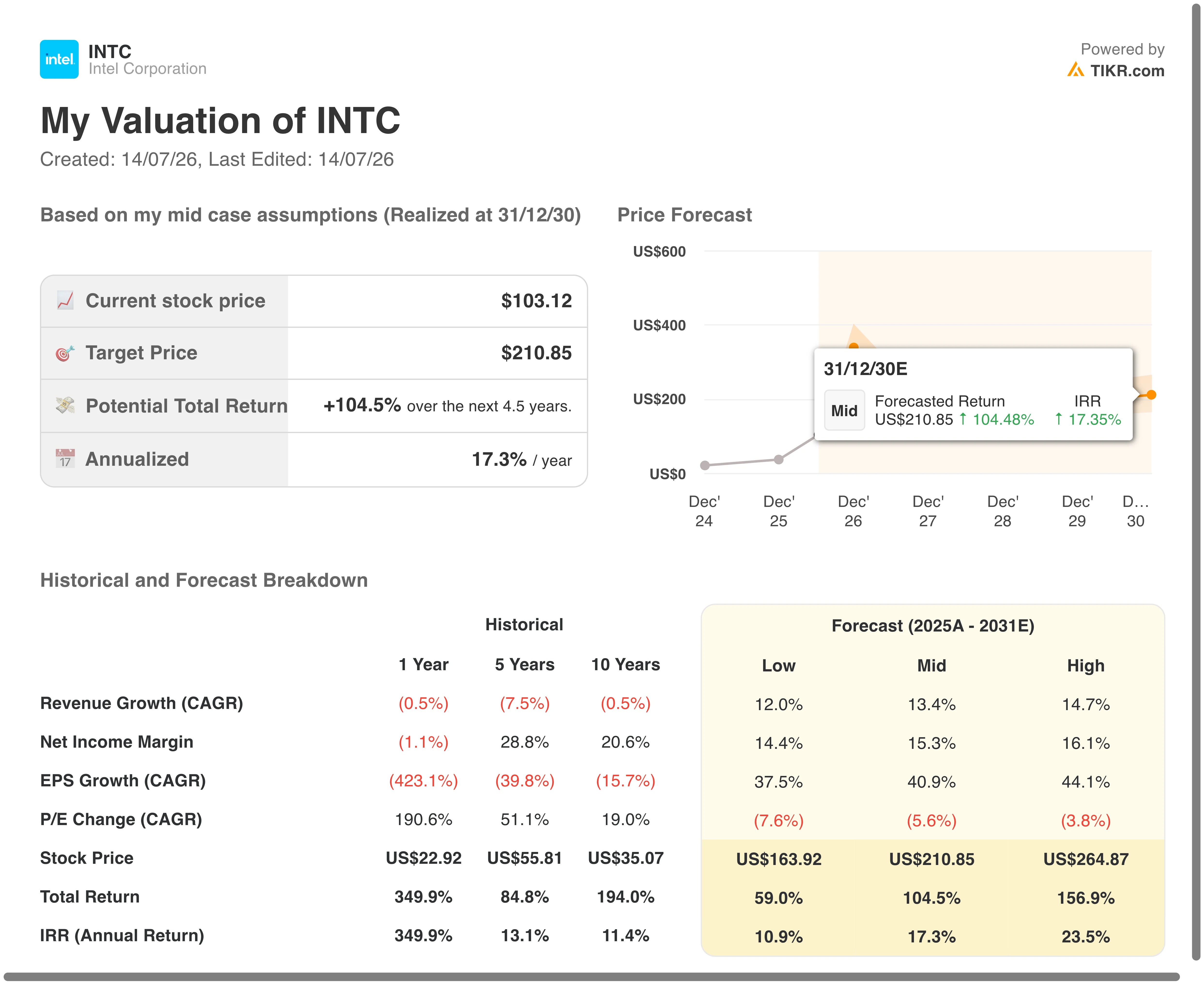

According to TIKR.com valuation data, Intel’s stock has already returned nearly 350% over the trailing year, a scenario that the same model identifies as an outlier relative to its five-year and ten-year historical returns of 84.8% and 194.0%.

Depending on the assumptions used, TIKR’s model puts fair value anywhere from about $138 by the end of 2028 to roughly $211 by the end of 2030 in a mid-case scenario, implying annualized returns between roughly 12.7% and 17.3%.

That’s a wide range. It tells you the market hasn’t settled on a single story for Intel yet. The smarter move is to separate the chip design business from the foundry business and value each on its own merits, then track the operational milestones that would justify either the low end or the high end of that range.

Build your own Valuation Model to value any stock (It’s free!) >>>

The financial signals worth tracking

TIKR.com financial estimates show Intel’s revenue is expected to climb from $52.85 billion in 2025 to $98.96 billion by 2030, with net income normalized turning from under $2 billion to over $30 billion over that same stretch.

Free cash flow is the number that matters most right now. Intel’s free cash flow was negative $4.95 billion in 2025 and is estimated to stay negative in 2026 before turning positive in 2027 and climbing to over $20 billion by 2030, per TIKR.com estimates.

That path from cash burn to cash generation is the clearest sign of whether the turnaround is holding up.

See analysts’ growth forecasts and price targets for Intel stock (It’s free) >>>

Manufacturing milestones are the make-or-break signal

Intel CFO David Zinsner told analysts at Bank of America’s Global Technology Conference on June 2 that the company’s 18A process is improving yields roughly 7% every month and that Intel is likely to pull its 2027 profitability milestones in by at least a quarter.

Zinsner also said Intel still targets breakeven for its foundry business by the end of 2027, and that the company’s next process, 14A, is already ahead of where 18A stood at the same point in development.

At JPMorgan’s technology conference on May 19, Tan said Intel released a 0.5 process development kit for 14A this year, with a more mature 0.9 kit targeted for external customers around October.

Are real customers showing up

Progress on paper means little without customers willing to pay for it. At Intel’s COMPUTEX keynote on June 1, the company announced a rack-scale computing partnership with Foxconn and highlighted existing collaborations with SambaNova, Google and Ericsson.

Zinsner noted that customers have agreed to prepay for scarce advanced packaging materials tied to Intel’s technology, calling it evidence they are serious about using it. That kind of financial commitment is harder to fake than a press release.

A simple checklist for judging Intel stock

Before deciding if Intel is a turnaround or a trap, watch three things. Is free cash flow actually turning positive on schedule? Are manufacturing yield targets being hit or beaten, not just promised? And are outside customers putting real money behind Intel’s factories, not just issuing supportive quotes.

If those three keep improving together, the turnaround has legs. If anyone stalls, the stock’s recent run may be pricing in more good news than Intel has delivered yet.

Estimate a company’s fair value instantly (Free with TIKR) >>>

How Much Upside Does Intel Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!