Key Takeaways for Capital One Stock as of July 2026

- 20 of 24 analysts rate Capital One stock Buy or Outperform, with a consensus mean target of $258 leaving a 23% gap to the current $209.

- TIKR’s mid-case model targets $342 by December 2030: 64% total return, 12% annualized.

- Undervalued. Normalized EPS is set to reaccelerate to 25-27% growth by early 2027 as Discover expense synergies hit and quarterly buybacks compress the share count, yet Capital One stock sits 19% below its 52-week high.

- Following Q1’s $2.5 billion buyback, Capital One’s CET1 still sits at 14%, and at the June Morgan Stanley conference CEO Rich Fairbank committed to “lean into capital return” from here.

Capital One Stock’s Q1 Miss Masks an Earnings Reacceleration Starting Q4 2026

Capital One (COF) posted adjusted EPS of $4.42 in Q1 2026, up 9% year over year but missing the Street’s $4.57 estimate by 3%. Revenue of $15.2 billion also fell short of the $15.4 billion consensus.

The shortfall traced to a deliberate Discover brownout. Capital One tightened credit on high-balance revolvers and shrank Discover’s card loans 1.2% year over year ahead of the full platform conversion, which management expects to finish by Q1 2027.

That tightening drove domestic card delinquencies down 55 basis points year over year to 3.7%, with trends tracking better than normal seasonality through April. Auto charge-offs held at 1.64%, near pre-pandemic levels, while auto delinquencies fell 72 basis points year over year.

Strong credit across both portfolios let Capital One fund an aggressive capital return program. Management repurchased $2.5 billion in shares during Q1, and the CET1 ratio still sat at 14.4%, nearly 200 basis points above the 12.5% baseline in Capital One’s deal model.

At the Morgan Stanley conference in June, CEO Rich Fairbank framed the buyback pace as structural rather than tactical: “We can simultaneously have that conservatism and still lean into capital return, and that’s what we intend to do.”

Fairbank confirmed the $2.5 billion Discover synergy target remains intact, with expense savings weighted toward mid-2027 when platform conversions finish. Over the same period, revenue synergies from the completed debit network conversion will flow through at their full run rate.

In the near term, normalized EPS faces tough comparisons for two more quarters, with analysts modeling $4.74 in Q2 (down 13% year over year) and $5.50 in Q3 (down 8%). By Q4 2026, estimates flip to $4.88 (up 27%), and the Street projects $5.93 by Q2 2027, a 25% year-over-year gain.

Beyond the synergy timeline, Capital One closed the $4.5 billion Brex acquisition on April 7. The deal added a corporate expense management platform built on a vertically integrated tech stack that Fairbank said mirrors Capital One’s own architecture.

In April, Capital One also brought its travel technology in-house by acquiring the Hopper platform and engineering team behind its booking app.

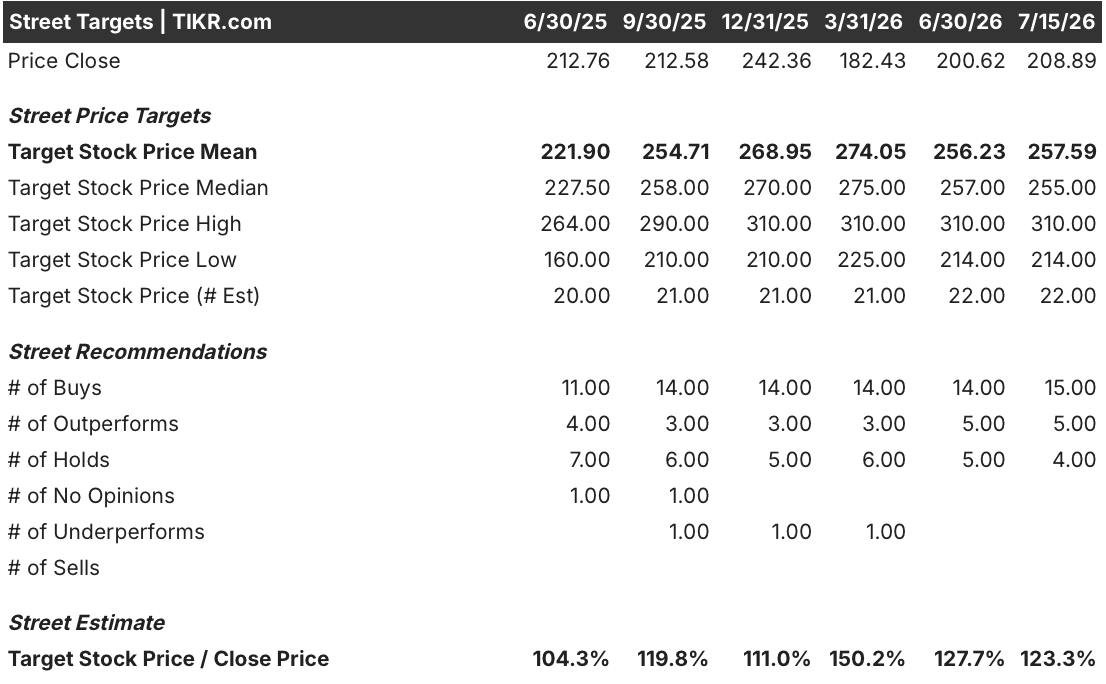

Wall Street Sees 23% Upside in Capital One Stock at $258

Of the 24 analysts covering Capital One stock, 15 rate it Buy and 5 rate it Outperform, with just 4 Holds and zero Sell ratings. The consensus mean price target sits at $258 against the current $209, putting the implied upside at 23%. Targets range from $214 at the low end to $310 at the high, with 22 analysts contributing price target estimates, up from 21 earlier in the year. Over the past 12 months, Buy ratings have climbed from 11 to 15.

Wall Street Expects Capital One Stock’s Normalized EPS to Reaccelerate 27% by Q4 2026

Capital One delivered normalized EPS of $4.42 in Q1 2026, up 9% year over year but decelerating from the 25-75% growth the Discover acquisition powered through mid-2025. Two more quarters of negative comparisons follow before growth resumes.

Analysts model Q2 2026 at $4.74 (down 13% year over year) and Q3 at $5.50 (down 8%), both pressured by the strong mid-2025 baseline when Discover’s first full quarters inflated results.

By Q4 2026, that trajectory reverses to $4.88, a 27% year-over-year gain. The Street then models $5.93 by Q2 2027 (up 25%), with growth holding in the 25-27% range across the first half of next year.

Q2 earnings on July 21 will show the first full quarter with Brex in the numbers and test whether Capital One stock’s near-term EPS trough has already passed.

TIKR Values Capital One Stock at $342, Pricing In the Full Earnings Ramp

TIKR’s mid-case model values Capital One at $342 by December 2030, a 64% total return from the current $209 or 12% annualized over 4.5 years.

The TIKR target sits 33% above the $258 Street mean, reflecting a longer horizon that captures both the full Discover synergy ramp and a buyback-fueled EPS compounding effect the 12-month consensus window misses.

Both drivers are already in motion. Fairbank confirmed the $2.5 billion synergy target in June, and Q1’s $2.5 billion buyback pace signals management views the 14.4% CET1 as well above any operating floor.

The stock prices in the near-term EPS dip without yet capturing the 25-27% reacceleration that begins just three quarters from now.

Should You Invest in Capital One Financial Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Capital One Financial Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Capital One Financial Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze COF stock on TIKR for Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!