Key Stats for PayPal Stock

- Today’s Performance: 16%

- 52-Week Range: $38 to $80

- Valuation Model Target Price: Around $53

- Implied Downside From Today’s Price: Around 3%

Analyze your favorite stocks like PayPal Holdings with TIKR (It’s free) >>>

What Happened?

PayPal Holdings stock surged about 16% today to roughly $55 per share as a takeover report abruptly changed the narrative around a company previously weighed down by slow growth and intensifying competition. Reuters reported that payments platform Stripe and private equity firm Advent International jointly offered $60.50 per share for PayPal, valuing the company at more than $53 billion and representing a 28% premium to Tuesday’s closing price.

The stock rose specifically because investors began pricing in the possibility that PayPal could be acquired at a substantial premium to its unaffected share price. The proposal was reportedly submitted earlier this month and is backed by about $50 billion in committed bank financing, but PayPal had not responded when the report was published, and the companies declined to comment. Shares remain below the $60.50 offer because the market is accounting for the risk that negotiations stall, the terms change, or no transaction is completed.

At PayPal’s recent Evercore Global TMT Conference, CTO Srinivasan Venkatesan said the company migrated 150 of roughly 300 C++ applications to Java within six months, while AI-assisted development was producing more than 2,000 pull requests per week and growing 50% month over month. PayPal has also used automation to extend checkout across 154 countries and is combining PayPal and Venmo payment systems, which would allow Venmo to add products such as buy now, pay later without building separate infrastructure. Venkatesan said the modernization effort aims to build “the best platform out there,” with simpler checkout and faster development potentially improving purchase conversion and reducing duplicated technology work.

The proposed transaction would combine Stripe’s merchant-focused payment infrastructure with PayPal’s consumer wallet, Venmo network, and branded checkout button, creating a payments business handling around $3.7 trillion annually. That scale would strengthen PayPal’s position against Adyen, Block’s Square ecosystem, Apple Pay, and Google Pay. Adyen processed €382 billion during the first quarter, up 21% year over year, while Block’s Square business remains a major rival in merchant payments and Cash App competes more directly with Venmo for consumer engagement.

Value PayPal Holdings instantly (Free with TIKR) >>>

Is PayPal Fairly Valued?

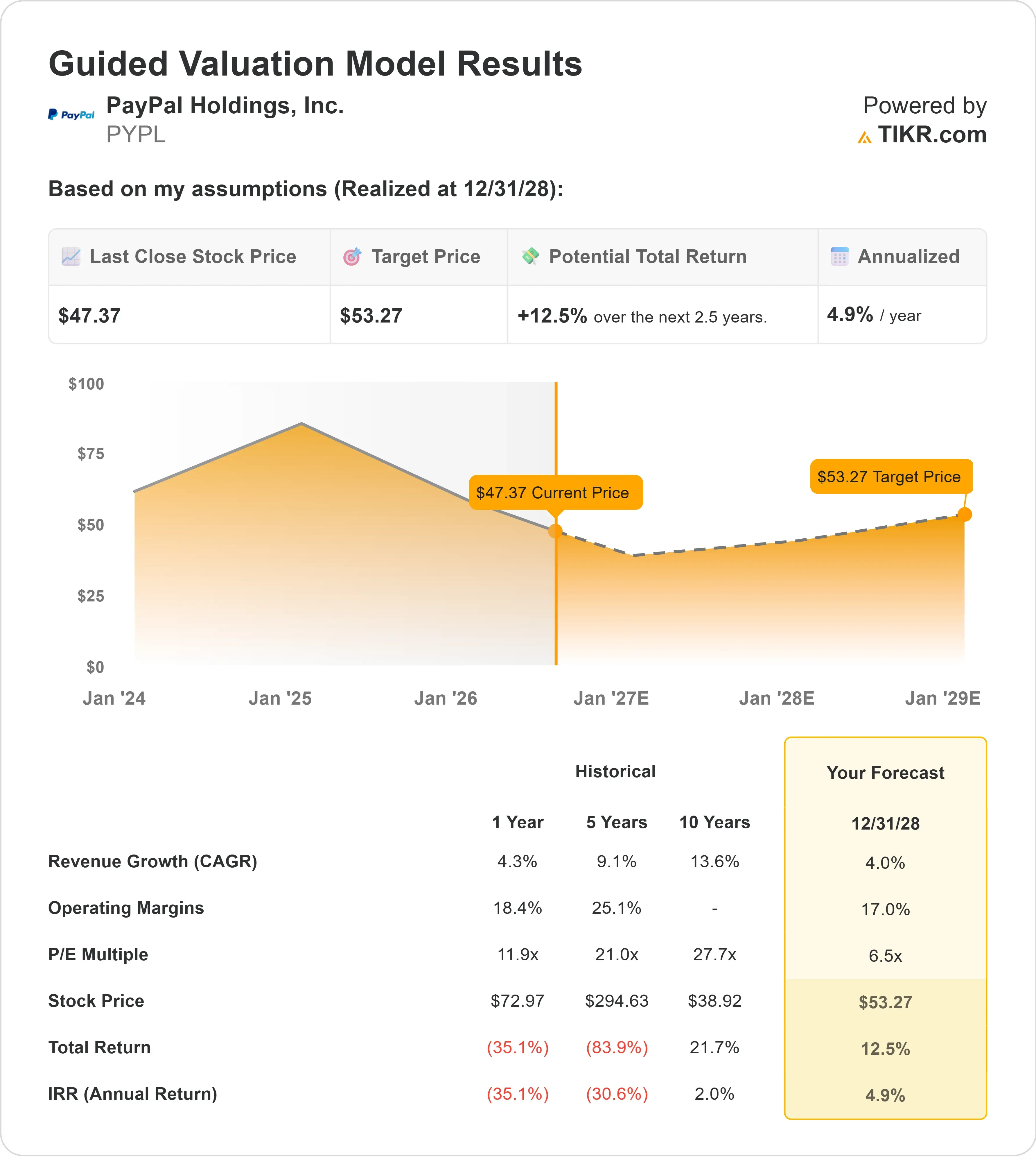

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 4%

- Operating Margins: Around 17%

- Exit P/E Multiple: Around 7x

TIKR’s model originally estimated that PayPal could reach around $53 over roughly 2.5 years from a starting price near $47, implying about 13% upside when the model was created.

Today’s rally has moved the stock to roughly $55, slightly above that target, leaving PayPal looking fairly valued on a standalone basis rather than clearly undervalued.

The 4% revenue-growth assumption reflects PayPal’s mature core business, making checkout conversion and the amount of profit retained from each transaction more important than payment-volume growth alone.

See analysts’ growth forecasts and price targets for PayPal Holdings (It’s free) >>>

PayPal’s operating income increased from $4.85 billion in 2023 to $6.20 billion in 2025, while its operating margin expanded from 16.3% to 18.7%. That historical improvement supports the model’s margin assumption, but further gains depend on PayPal making checkout easier and converting more payment activity into profitable transactions.

Reducing checkout from several screens to a one-page or one-click experience could increase completed purchases, while connecting Venmo to PayPal’s payment infrastructure could broaden merchant acceptance and support products such as buy now, pay later. Cloud migration and AI-assisted development could also reduce duplicated engineering work and accelerate product launches, although management expects the broader technology transformation to take two to three years.

Through the rest of 2026, PayPal’s performance will depend on whether the $60.50 proposal advances and, if it does not, whether management can strengthen branded checkout, expand Venmo monetization, and convert its large payments network into faster profit growth.

How Much Upside Does PayPal Stock Have From Here?

Investors can estimate PayPal Holdings’ potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value PayPal Holdings in under 60 seconds with TIKR (It’s free) >>>