Key Stats for Astera Labs Stock

- Monday Performance: -12%

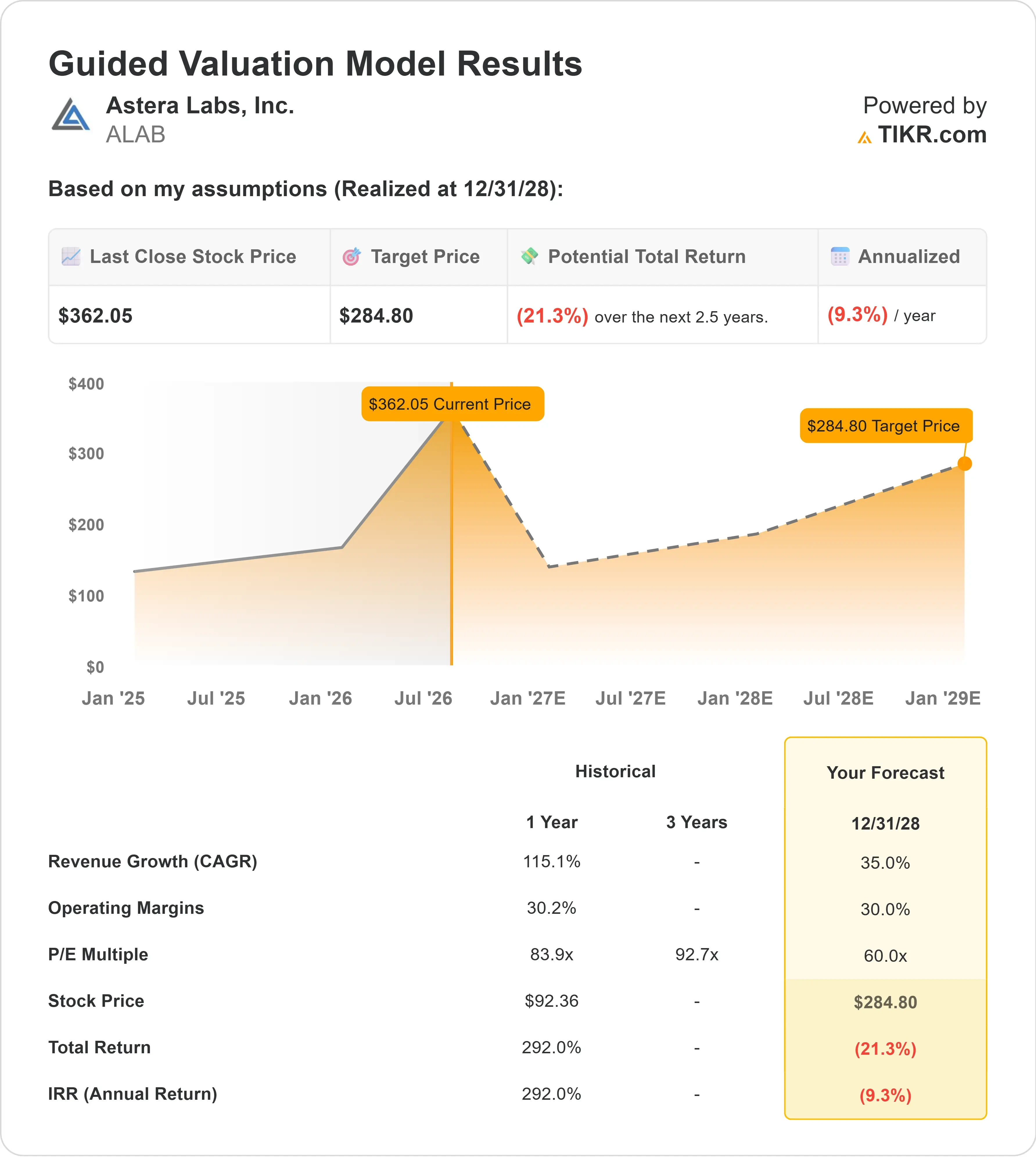

- 52-Week Range: $89 to $499

- Valuation Model Target Price by 2028: Around $285

- Implied Downside: About 21%

Analyze your favorite stocks like Astera Labs with TIKR (It’s free) >>>

What Happened?

Astera Labs has become one of the market’s most direct bets on a critical bottleneck inside AI data centers: moving data quickly and reliably between expanding clusters of processors. That excitement drove ALAB to a demanding valuation, leaving the shares vulnerable when investors retreated from semiconductor stocks Monday. Astera Labs fell 12% to close near $362 as escalating U.S.-Iran tensions, higher oil prices, and weaker risk appetite weighed on technology and semiconductor shares.

The stock fell as the sector-wide chip selloff prompted investors to reduce exposure to highly valued AI infrastructure companies, rather than following a new negative operating announcement from Astera Labs. The Philadelphia Semiconductor Index declined nearly 5%, while AI-connectivity competitors Credo Technology and Marvell Technology fell about 8% each. ALAB’s steeper decline suggests its premium valuation and sharp prior rally made it particularly vulnerable as investors became less willing to pay elevated prices for future AI growth.

Recent management commentary continued to support the underlying growth story. At the Evercore conference, Astera Labs said Scorpio accounted for about 15% of 2025 revenue and could expand further as its new 320-lane Scorpio X switch enters volume production in the second half of 2026, while two hyperscalers begin contributing to P-Series revenue. Scorpio switches connect many AI processors so they can function as one larger computing system, potentially giving Astera Labs more revenue per AI rack than its original signal-conditioning products. CFO Desmond Lynch said, “Scorpio will become our largest product line” by year-end, with additional X-Series design wins expected late in 2026 that could contribute in 2027 and beyond.

Analyst activity captured the tension between Astera Labs’ growth prospects and its valuation. TD Cowen raised its price target from $225 to $425 on Monday but maintained a Hold rating, while Bank of America recently increased its target from $240 to $450 and maintained Neutral. The substantial revisions reflect stronger expectations for AI connectivity demand and upcoming product launches, but the unchanged ratings show that analysts remain cautious about how much future growth is already reflected in ALAB’s share price.

Value Astera Labs instantly (Free with TIKR) >>>

Is Astera Labs Overvalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): Around 35%

- Operating Margins: Around 30%

- Exit P/E Multiple: 60x

The model assumes Astera Labs can sustain around 35% annual revenue growth through 2028. Delivering that pace requires the company to expand beyond Aries retimers, which restore weakened high-speed signals inside dense servers, and generate meaningful sales from Scorpio switches, Taurus cable modules, CXL memory controllers, optical products, and custom connectivity solutions.

Scorpio represents the most important near-term growth lever because switches can add considerably more Astera Labs content to each AI system. The new 320-lane Scorpio X product can connect an entire 72-processor AI rack in a single step, while the broader 32-to-320-lane portfolio gives the company more opportunities across customers using different AI architectures. Management expects the 320-lane solution to enter volume production during the second half of 2026.

Astera Labs’ latest results explain why investors have assigned the company a premium valuation. First-quarter revenue reached a record $308.4 million, rising 14% sequentially and 93% year over year, while non-GAAP operating margin reached 36.2%. Management guided for second-quarter revenue of $355 million to $365 million, with the midpoint implying around 17% sequential growth and providing an important test of whether the current trajectory can support the share price.

Competition remains intense despite Astera Labs’ early position in PCIe 6 connectivity. Credo competes directly in active electrical cables and other high-speed data links, while Marvell and Broadcom offer broader AI networking and custom-chip portfolios. Credo reported quarterly revenue of $437.0 million, up 157.0% year over year, compared with Astera Labs’ $308.4 million and 93% growth, showing that ALAB is competing against another rapidly scaling connectivity specialist rather than growing in isolation. Astera Labs differentiates itself through its COSMOS software, which helps data-center operators monitor connection health, temperatures, and traffic, and through its early delivery of PCIe 6 switching and signal-conditioning products.

The model’s roughly 30% operating-margin assumption appears defensible relative to Astera Labs’ latest 36.2% non-GAAP result, but maintaining that profitability for several years will still require disciplined execution. The company must preserve pricing while funding switching, optical-connectivity, memory, and custom-chip development, with product mix, research spending, customer concentration, and large hyperscaler contracts all capable of affecting margins.

The 60x exit P/E multiple is the model’s most demanding input. It assumes investors will continue treating Astera Labs as an unusually fast-growing semiconductor company several years from now, which requires Scorpio to become a major revenue contributor, PCIe Gen 6 adoption to remain strong, and the company to defend its position as open standards attract additional competitors.

See analysts’ growth forecasts and price targets for Astera Labs (It’s free) >>>

The revenue chart illustrates both the opportunity and the uncertainty embedded in ALAB’s valuation. Consensus estimates show revenue rising from about $853 million in 2025 to around $2.8 billion in 2028, although the less consistent forecasts beyond 2028 show why long-term projections should be treated as directional rather than precise.

Based on these assumptions, the model estimates a target price of around $285 by the end of 2028. That represents about 21% downside from the $362 closing price, even though the model already assumes rapid revenue growth, strong margins, and a premium earnings multiple. The $285 figure is a longer-term valuation output and does not represent a prediction for ALAB’s price at the end of 2026.

Performance over the next 12 months will depend heavily on whether the 320-lane Scorpio X switch progresses from early shipments into sustained production volumes. Contributions from two P-Series hyperscaler customers would broaden the revenue base and demonstrate that demand extends beyond Astera Labs’ lead customer. PCIe Gen 6 could provide another meaningful lift because these products already represented about one-third of recent quarterly revenue and typically carry 20% to 25% higher average selling prices than the prior generation. Optical and CXL design wins add longer-term opportunities, although several programs are unlikely to contribute materially until 2027 or later.

At current levels, Astera Labs appears overvalued, with stronger returns requiring rapid Scorpio adoption, broader customer penetration, and earnings growth beyond the model’s already-demanding assumptions.

How Much Upside Does Astera Labs Stock Have From Here?

Investors can estimate Astera Labs’ potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Astera Labs in under 60 seconds with TIKR (It’s free) >>>