Key Stats for Roku, Inc.

- 52-Week Range: $78.53 to $148.88

- Current Price: $141.76

- Street Mean Target: $153.64

- Market Cap: ~$21 billion

- Q1 2026 Revenue: $1.25 billion, up 22% YoY

- Q1 2026 Platform Revenue: $1.13 billion, up 28% YoY

- Q1 2026 Adjusted EBITDA: $148 million, up 165% YoY

- Free Cash Flow (TTM): $539 million, an all-time high

- Streaming Households: 100 million+

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Fox Is Paying $160 for Roku. The Stock Is Still at $140.

On June 15, Fox Corporation announced it would acquire Roku, Inc. (ROKU) for $160 per share in a cash-and-stock deal valued at roughly $22 billion.

The strategic rationale is easy to follow: Fox pairs its live sports, news, and the Tubi free streaming service with Roku’s connected TV operating system, 100 million streaming households, and The Roku Channel. Together, they form one of the most complete distribution and advertising stacks in streaming.

The chart tells you exactly why investors are hesitant to close that $20 gap. Roku dropped nearly 28% from its highs by mid-February before recovering sharply through the spring. Anyone who has watched this stock knows it can move quickly in either direction.

The deal is expected to close in 2027, and that time horizon, combined with regulatory uncertainty, is why the market is applying a discount. Investors buying today are pricing in roughly 14% upside if the transaction closes at the announced terms, with volatility risk in either direction along the way.

See historical and forward estimates for Roku stock (It’s free!) >>>

The Platform Business Is What Made This Deal Happen

Before the acquisition news, something more fundamental had changed at Roku: the business had turned a corner. Platform revenue grew 28% in Q1 2026 to $1.13 billion. Within that, Advertising grew 27% to $613 million, and Subscriptions grew 30% to $519 million, both outpacing the broader streaming ad market.

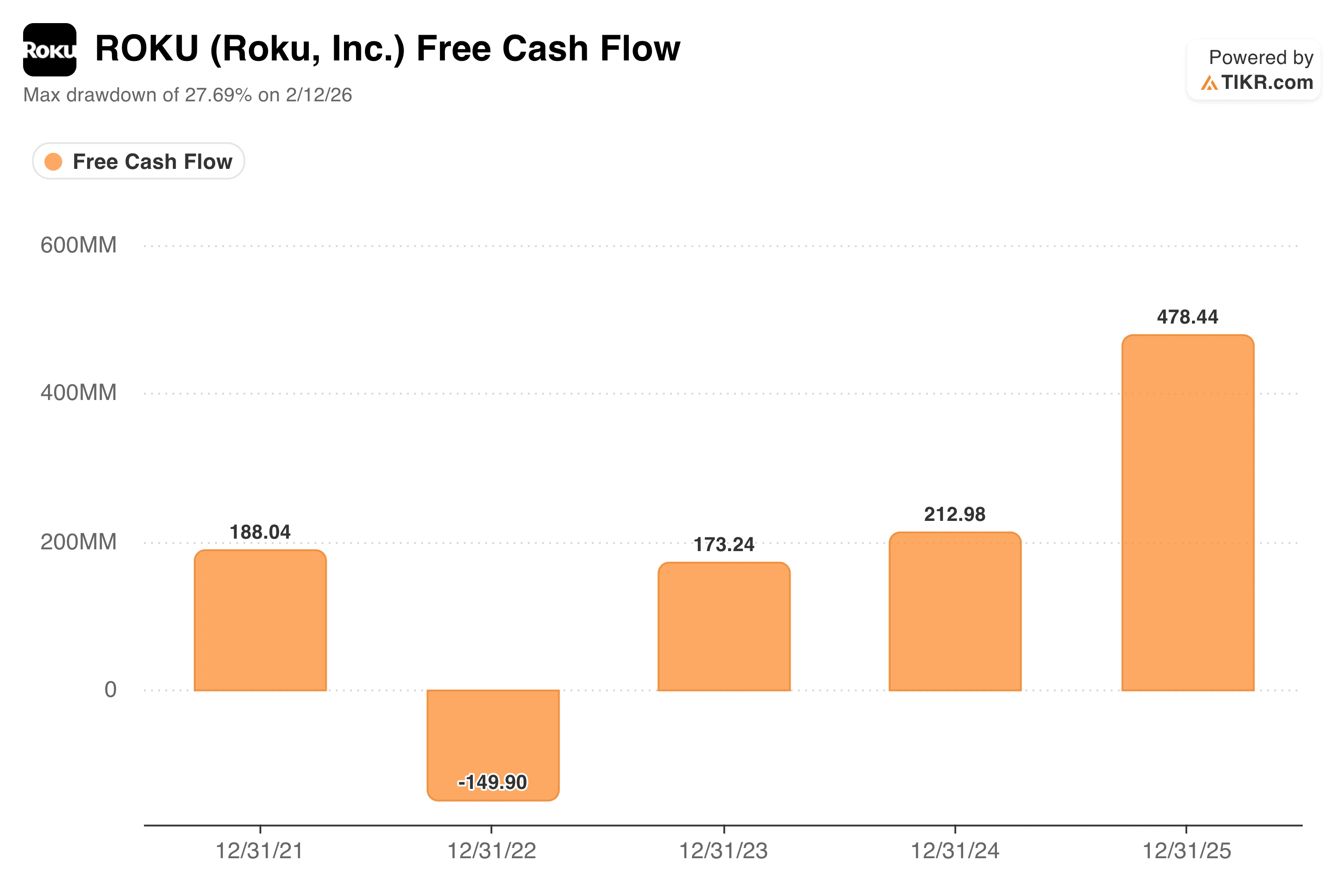

The free cash flow chart makes the inflection hard to argue with. FCF went negative in 2022, recovered to $173 million in 2023 and $213 million in 2024, then surged to $478 million in 2025 as Roku’s monetization finally caught up with its scale.

On a trailing twelve-month basis through Q1 2026, FCF has reached $539 million, an all-time high. CEO Anthony Wood and CFO Dan Jedda noted in the shareholder letter that the company is targeting $1 billion in annual free cash flow by 2028, if not sooner.

Programmatic advertising is a big part of what’s driving that: ad spend through third-party platforms grew more than 40% year over year, and Roku’s inventory can now be purchased through virtually every major buying platform, including Google’s DV360, Amazon DSP, and The Trade Desk.

The platform had become genuinely attractive on its own merits, likely catching Fox’s attention.

See how Roku performs against its peers in TIKR (It’s free!) >>>

What Does the Valuation Model Suggest If the Deal Falls Through?

The $160 offer sets a near-term ceiling for most investors. But it’s worth understanding what Roku looks like as a standalone business, partly because deals don’t always close at the announced price, and partly because it helps frame whether Fox is getting a good deal or a great one.

The TIKR valuation model’s mid case points to a target of around $263 by the end of 2030, implying roughly 87% total return from today’s price, or about 15% annualized. The assumptions behind that are around 10% annual revenue growth and net income margins expanding toward 10%, which is a reasonable extension of the operating leverage already visible in the numbers.

EPS is projected to grow around 30% annually as the company scales past breakeven. If those projections hold, Fox is acquiring Roku well below what the platform might be worth on its own in four or five years.

For investors considering the stock today, the decision is really about deal confidence. Buying at $140 with a $160 offer on the table is a straightforward return if the transaction closes. The longer-term model suggests the platform itself has more runway than the buyout price implies.

Roku’s underlying business is strong, the FCF trajectory is compelling, and the Fox deal adds strategic credibility to the platform thesis. Use TIKR to track how both the financials and the deal timeline evolve before making your own call.

Should You Invest in Roku, Inc.?

Roku’s underlying business is in the best shape it has ever been, with platform revenue accelerating, free cash flow at an all-time high, and a strategic acquirer willing to pay $160 per share to own it.

The question for investors today is really a deal-confidence question: if Fox’s acquisition closes on its announced terms, buying at $140 offers a straightforward 14% return with a defined timeline. If the deal runs into regulatory trouble or gets renegotiated, you are left holding a high-quality streaming platform that a major media company valued at $22 billion just months ago.

Put TIKR to work tracking Roku’s financials, the deal timeline, and how Wall Street’s price targets shift as the close date approaches.

See analysts’ growth forecasts and price targets for Roku stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!