Key Takeaways for Walmart Stock as of July 2026

- Forty-four analysts cover Walmart stock, 37 rating it buy or outperform against one sell, and the $138.59 mean target sits 22% above the July 14 close of $113.70.

- TIKR’s mid case model prices Walmart stock at $148 by early 2031.

- Normalized EPS growth accelerates from 9% next quarter to 13% by mid fiscal 2028, a trend the current price does not yet reflect.

- The May 21 fiscal first quarter print showed free cash flow swinging to negative $1.95 billion as capital spending jumped 34%, overshadowing an 8% revenue beat.

Walmart stock sits well below both Wall Street’s mean target and TIKR’s model price. See exactly what is driving the gap and analyze the numbers on TIKR for free →

Walmart Stock Beats on Revenue But Free Cash Flow Turns Negative

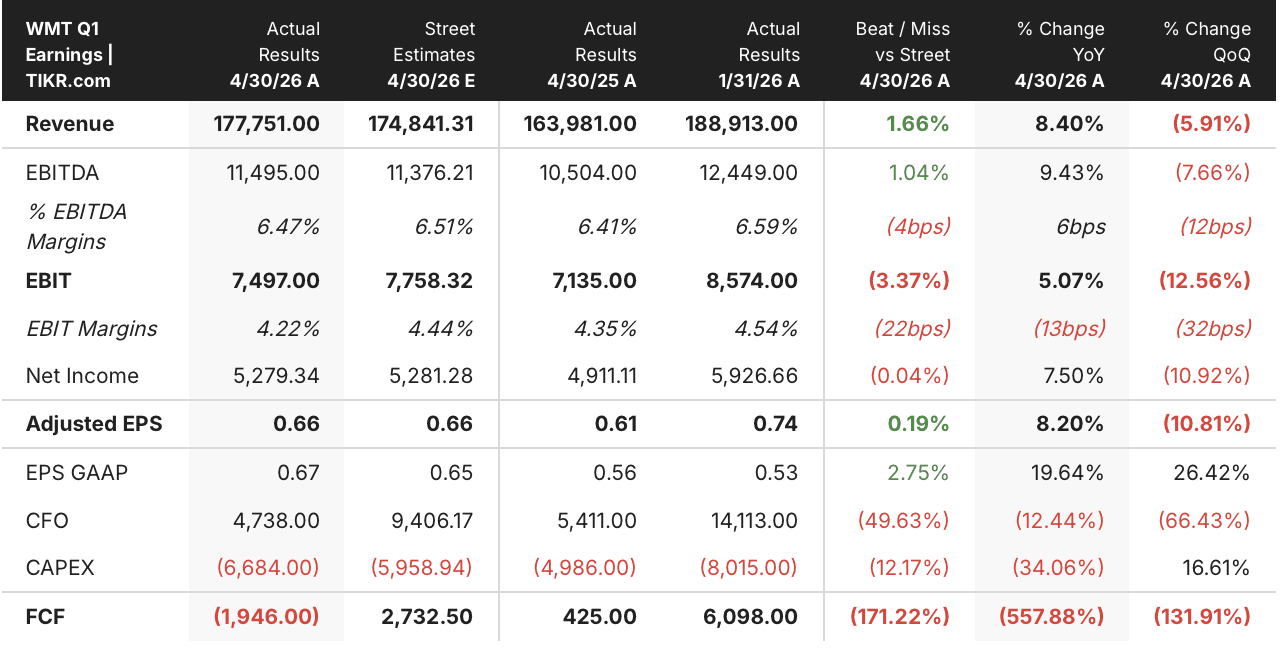

Walmart (WMT) posted fiscal first quarter 2027 revenue of $177.75 billion on May 21, beating the Street’s $174.84 billion estimate by 1.66% and growing 8.40% year over year. Adjusted earnings per share of $0.66 matched consensus exactly, but free cash flow swung to negative $1.95 billion, a 557.88% collapse from the prior year.

That FCF reversal traces directly to capital spending, which climbed 34% year over year to $6.68 billion as Walmart pours money into automated distribution centers, fulfillment capacity and its drone delivery network. Cash from operations fell 12.44% year over year to $4.74 billion, missing the Street’s $9.41 billion estimate by nearly half.

CFO John Rainey tied part of the profit pressure to costs outside the company’s control, telling analysts on the earnings call that fuel expenses cut into results directly in Q1 2027 earnings call: “We absorbed approximately $175 million or about 250 basis points of operating income growth from higher-than-anticipated fuel costs in our global distribution and fulfillment operations.” EBIT of $7.50 billion missed the Street’s $7.76 billion estimate by 3.37%, with margins contracting 22 basis points versus consensus.

Despite the fuel drag, Rainey argued the spending itself is the right allocation of capital, saying Walmart would rather fund price investment and infrastructure than protect a single quarter’s margin: “We think the single best return that we can have on one dollar of capital right now is to invest in the customer and invest in price.” That framing matters because the areas absorbing the capital, U.S. eCommerce, marketplace and Walmart Fulfillment Services, are also where the growth is showing up.

Those growth areas back up the framing. U.S. eCommerce grew 26% and carried incremental margins near 12% in the quarter, while marketplace sales rose almost 50% and advertising revenue grew 37% globally.

Membership fee revenue increased 17.5% on top of that, and those three higher margin lines, advertising, marketplace and membership, now account for roughly a third of enterprise operating income. Same day and next day delivery under three hours now reaches 36% of U.S. store fulfilled orders, up 800 basis points in two years.

The mix shift explains why Walmart stock fell just 0.94% to $113.70 on July 14 rather than selling off harder on the FCF miss. The cash burn is investment led, not demand led, and revenue, adjusted EPS and delivery speed all moved in the right direction even as free cash flow and EBIT missed.

Walmart stock just posted a free cash flow miss investors cannot ignore. See how TIKR’s model weighs that against the growth numbers and analyze it on TIKR for free →

Wall Street Analysts Remain Overwhelmingly Bullish on WMT Stock

Wall Street’s consensus on Walmart stock leans decisively bullish, with 28 buy ratings and 9 outperforms against just 5 holds and one sell among 44 analysts covering the name. The $139 mean target sits 22% above the July 14 close of $114, unchanged since June 30 despite the stock’s pullback from its $135 fifty-two week high. That target has climbed steadily from $110 a year ago, tracking the same acceleration in Walmart’s high margin businesses that shows up in the forward numbers below.

Wall Street Expects WMT Stock’s Normalized EPS to Grow 13% by Fiscal 2028

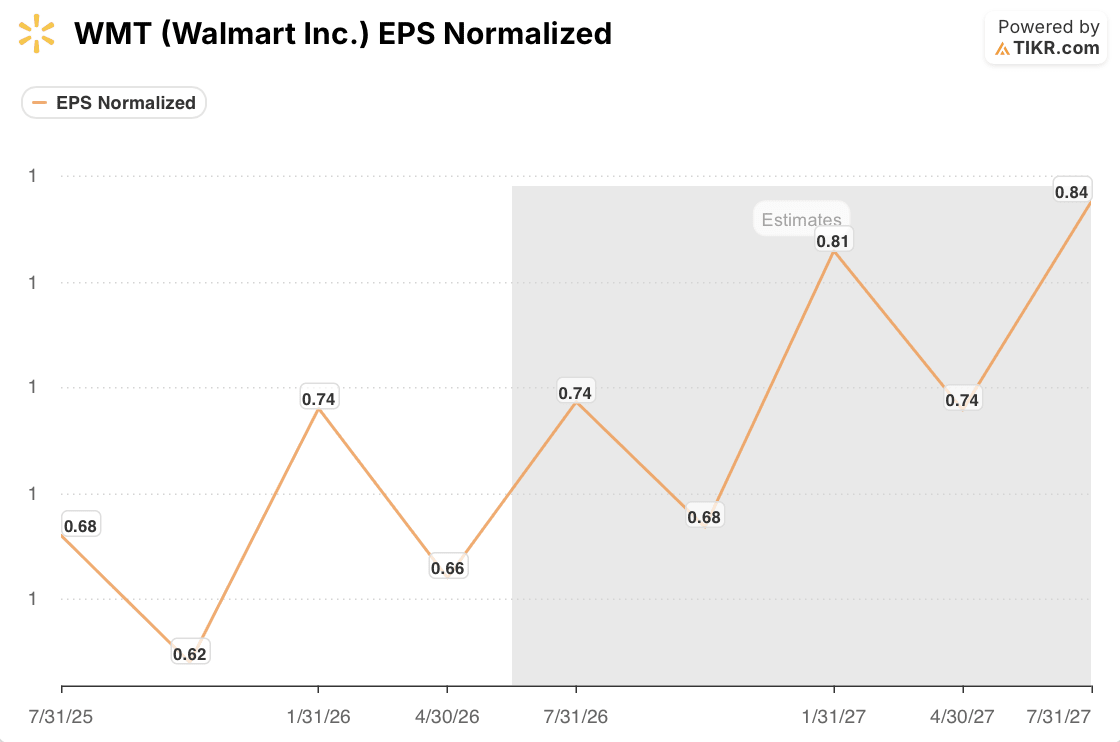

Walmart’s fiscal first quarter normalized EPS of $0.66 grew 8.20% year over year and matched the Street’s estimate exactly. Analysts expect that growth rate to accelerate to 9% in the fiscal second quarter and 10% in both the third and fourth quarters of fiscal 2027.

That trajectory keeps building into fiscal 2028, with normalized EPS growth reaching 12% in the first quarter and 13% by the second, the fastest pace on record.

GAAP EPS tells a different story over the same stretch, declining 15% and 12% year over year in the fiscal second and third quarters before rebounding 54% in the fiscal fourth quarter.

That GAAP swing reflects tough comparisons against prior year one time items, not a change in the underlying earnings trend, since normalized EPS keeps climbing through every one of those same quarters. The question for Walmart stock is whether the market keeps pricing the GAAP headline instead of the normalized trend that the Street’s own model already expects to accelerate.

TIKR Prices Walmart Stock at $148, a 30% Total Return by 2031

TIKR’s mid case model values Walmart stock at $148.01 by January 2031, a 30% total return from the current $113.70 price, or 6% annualized over the next 4.5 years.

That 6% annualized return sits below what growth investors typically demand, but it comes from a mega cap retailer trading near the low end of its fifty-two week range, a combination that limits downside while the model still prices in real upside.

The target is reachable because the same forces already showing up in the numbers, eCommerce growth of 26%, marketplace growth near 50% and advertising growth of 37%, continue compounding against a store network that reaches 90% of U.S. households within 10 miles. Those businesses carry higher margins than the core retail business, and as they take a larger share of operating income, normalized EPS growth accelerates even while capital spending and GAAP comparisons create short term noise.

Walmart stock’s path to a 30% total return runs through the same growth engines driving today’s numbers. Dig into the full model and forecast on TIKR for free →

Should You Invest in Walmart Inc.?fr

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Walmart Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Walmart Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WMT stock on TIKR for Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!