Key Stats for Snowflake Inc.

- 52-Week Range: $118.30 to $284.99

- Current Price: $275.94

- Street Mean Target: $292.53

- Market Cap: ~$93 billion

- Q1 FY2027 Total Revenue: $1.39 billion, up 33% YoY

- Q1 FY2027 Product Revenue: $1.33 billion, up 34% YoY

- Net Revenue Retention Rate: 126%

- Non-GAAP Operating Margin: 12%, up around 300 basis points YoY

- FY2027 Product Revenue Guidance: $5.84 billion, implying ~31% growth

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Snowflake Dropped 48% by April. Then Earnings Hit.

Snowflake, Inc. (SNOW) entered 2026 carrying a familiar burden: a premium valuation and a market that had grown impatient waiting for the AI story to show up in the numbers. The stock started sliding in January and never really stopped, grinding lower through February, March, and into April without any single catastrophic event driving it. It was more like a slow exhale of skepticism.

The drawdown chart captures exactly how painful that stretch was. Starting from near zero in January, the line drops quickly to around -30% by early February, bounces, then resumes its slide before hitting the max drawdown of 48% on April 10. What happened next is the part worth paying attention to: the line shoots almost vertically back toward zero in a matter of weeks.

That recovery was triggered by Snowflake’s Q1 fiscal 2027 earnings on May 27, which came in well ahead of market expectations. Total revenue reached $1.39 billion, up 33% year over year, beating consensus by around 5%. Product revenue, which is the metric Snowflake and its investors treat as the truest measure of platform health, grew 34%, up from 30% the prior quarter.

CEO Sridhar Ramaswamy called it “the strongest sequential dollar growth in our history.” The stock recovered nearly the entire drawdown almost immediately.

See historical and forward estimates for Snowflake stock (It’s free!) >>>

The Revenue Trajectory Makes the Case for Patience

Snowflake is a data cloud company, meaning it provides the infrastructure that enterprises use to store, analyze, and increasingly run AI workloads on their data. The more data customers process on the platform, the more they pay.

It is a consumption-based model, which means revenue accelerates when customers lean in and slows when they pull back. The reason investors stayed involved through a 48% decline is that the underlying growth curve had been remarkably consistent for years.

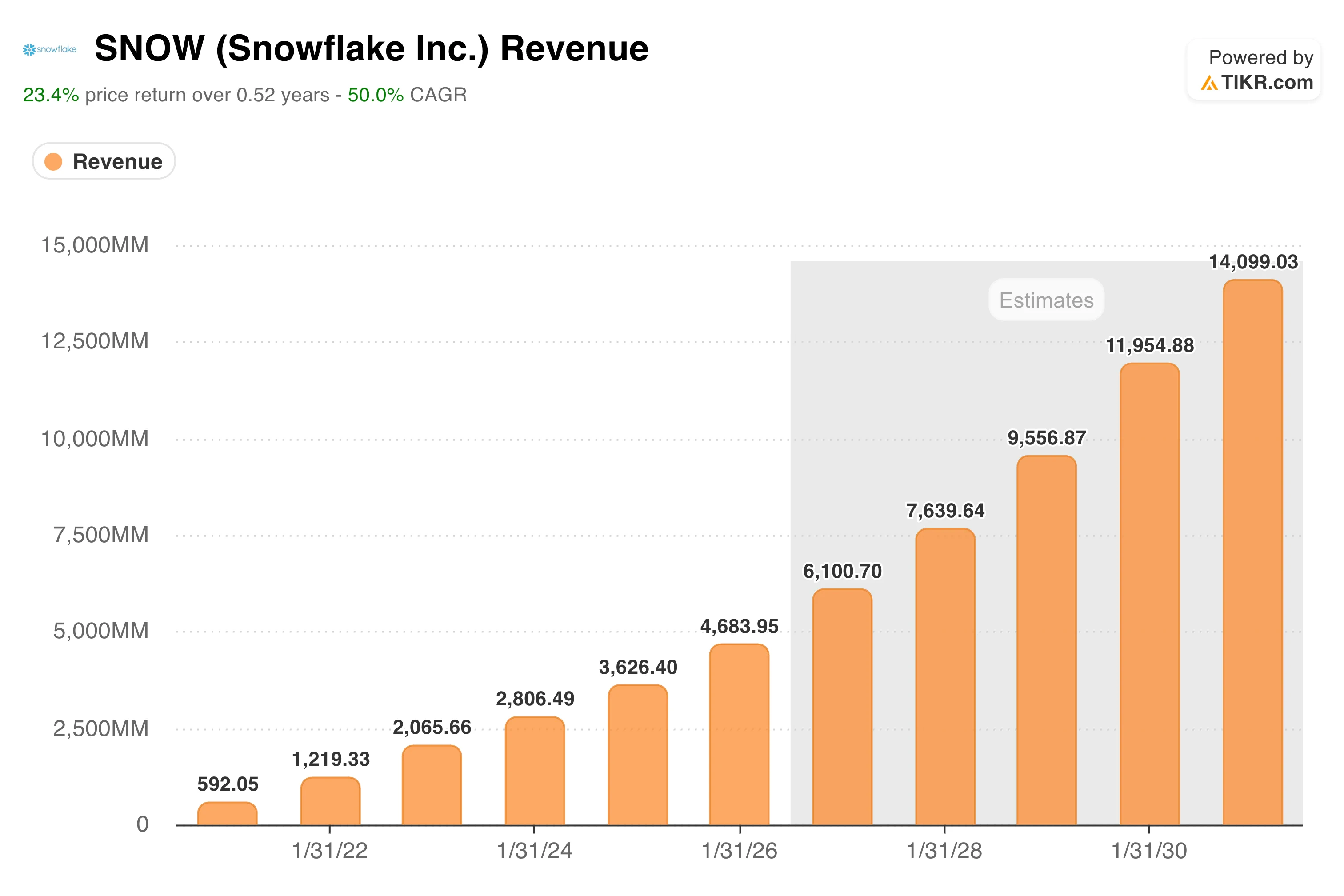

The chart makes that consistency impossible to argue with. Revenue climbed from $592 million in fiscal 2022 to $1.2 billion, $2.1 billion, $2.8 billion, $3.6 billion, and $4.7 billion in fiscal 2026, with every bar taller than the last and no interruptions along the way. Consensus estimates project that continuing toward $6 billion next year and climbing to around $14 billion by fiscal 2030.

What the Q1 results suggested is that AI is now actively pulling that curve steeper. Accounts using Snowflake Intelligence, the company’s agentic AI layer that lets enterprises query and act on their data in plain language, more than doubled quarter over quarter.

The company also surpassed $7 billion in lifetime AWS Marketplace sales and expanded a $200 million partnership with OpenAI. These aren’t peripheral deals. They signal Snowflake embedding itself deeper into the infrastructure stack that large enterprises are building around AI.

See how Snowflake performs against its peers in TIKR (It’s free!) >>>

What Does the Valuation Model Say?

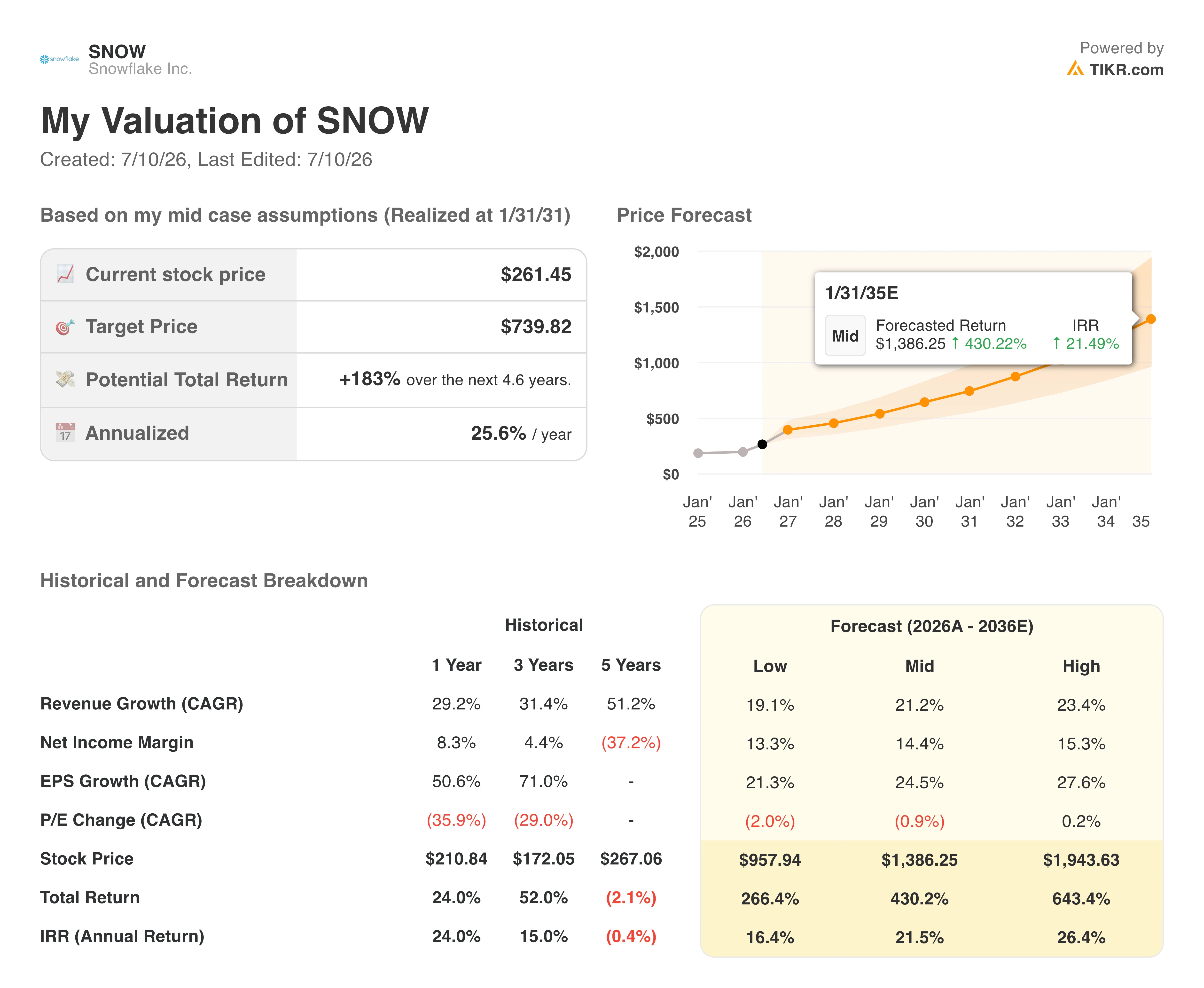

Snowflake still trades at a premium multiple, at around 14 times forward revenue and roughly 124 times forward earnings. For a company that remains GAAP unprofitable, that requires some conviction in the forward curve. The TIKR valuation model helps frame what that curve might actually be worth.

The mid case targets around $740 by January 2031, implying roughly 183% total return from today’s price, or about 26% annualized. The model assumes around 21% annual revenue growth and net income margins expanding toward 14% as operating leverage builds.

Those assumptions are grounded in what the business is already doing: the three-year revenue CAGR sits at 31%, and non-GAAP margins have been expanding steadily for several quarters. The key variable is whether AI consumption sustains.

If enterprises continue deepening their Snowflake workloads as AI adoption grows, the revenue assumptions may prove conservative. If spending stalls, the multiple has room to compress further.

Should You Invest in Snowflake, Inc.?

Snowflake is not a cheap stock, and the GAAP losses are real. What Q1 established is that the AI narrative has finally found its footing in the actual numbers, with product revenue accelerating, the retention rate holding above 125%, and full-year guidance raised meaningfully.

Investors who held through the April drawdown were rewarded quickly. Whether the same patience pays off from here depends on how strongly you believe the consumption model will continue to compound.

Most investors never know if a stock is truly undervalued or overpriced. TIKR’s professional-grade valuation tools give you a clear, data-backed answer across 60,000+ stocks for free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!