Key Stats for Snowflake Stock

- 52-Week Range: $118 to $285

- Current Price: $238

- Street Mean Target: $288

- Street High Target: $500

- Analyst Consensus: 35 Buy, 9 Outperform, 6 Hold, 1 Sell

- TIKR Model Target (Dec. 2030): $677

Snowflake Q1 FY27 Results: The Quarter That Changed How Analysts See SNOW

Snowflake (SNOW), the enterprise data cloud platform, surged around 38% on May 28 after reporting Q1 fiscal 2027 revenue of $1.39 billion, beating analyst estimates of around $1.32 billion and accelerating product revenue growth to 34% year-over-year.

That growth rate matters because it was 26% a year ago and 30% last quarter.

The catalyst behind the acceleration was Cortex Code, Snowflake’s AI coding agent known internally as CoCo, which reached general availability on February 5 and drove what the company described as the strongest sequential dollar growth in its history.

Net revenue retention climbed to 126%, and remaining performance obligations grew 38% year-over-year to around $9.2 billion, signaling that the demand locked in ahead is expanding, not contracting.

The company added 616 net new customers, up 38% year-over-year, with 13 Global 2000 additions compared to 4 in the same period last year.

Snowflake also signed a five-year, $6 billion infrastructure commitment with Amazon Web Services, its largest AWS deal ever, deepening integrations across Graviton compute, Cortex AI, and enterprise workload migrations.

“Based on a combination of strength in our core data platform business and meaningful uplift from AI capabilities, including CoCo and Snowflake Intelligence, we are increasing our FY ’27 outlook from 27% to 31% year-over-year growth,” said CEO Sridhar Ramaswamy on the Q1 2027 earnings call.

The company raised its full-year product revenue forecast to $5.84 billion, up from $5.66 billion, and guided Q2 product revenue of approximately $1.42 billion against prior analyst expectations of around $1.37 billion.

At an Investor Day held June 2 alongside the Snowflake Summit conference, management announced a path to GAAP profitability in Q4 fiscal 2028 and raised full-year non-GAAP operating margin guidance from 12.5% to 13.5%.

Snowflake also announced the planned acquisition of Natoma, an enterprise Model Context Protocol platform designed to give AI agents governed, auditable access to external business systems, extending the company’s agentic control plane beyond data into the full enterprise workflow stack.

Wall Street Raises Targets Across the Board After Snowflake Stock Earnings

At 48 combined Buy and Outperform ratings against 6 Holds and 1 Sell, analyst conviction on Snowflake stock is near its highest level in over a year.

Following earnings, more than 30 analysts raised price targets in a single day. The Street mean target now sits at around $288, implying approximately 21% upside from the current price of $238. The Street high target stands at $500.

The metric driving the consensus upgrade is revenue growth. Q1 product revenue of $1.33 billion came in meaningfully above estimates, and the full-year guidance of $5.84 billion implies 31% growth — a step-change from the 27% the company had projected entering the quarter.

The consensus estimates table reflects that repricing. Q2 revenue is estimated at around $1.48 billion, implying roughly 30% year-over-year growth. Revenue for the January 2027 quarter is estimated at around $1.65 billion.

One risk: Snowflake’s consumption-based model means revenue guidance is anchored in observed usage patterns, not committed bookings. CFO Brian Robins stated on the earnings call that there was no change to the company’s guidance philosophy, and that a 3% beat is considered a strong quarter. The guidance raise was driven by one quarter of observable CoCo behavior — if adoption plateaus or usage efficiency improvements dampen token consumption, forward estimates could moderate.

The catalyst to watch in Q2 is whether CoCo-driven consumption acceleration holds through the summer quarter, given that Q4 renewals remain heavily weighted and early-cycle consumption data will be the first read on whether the Q1 inflection was structural.

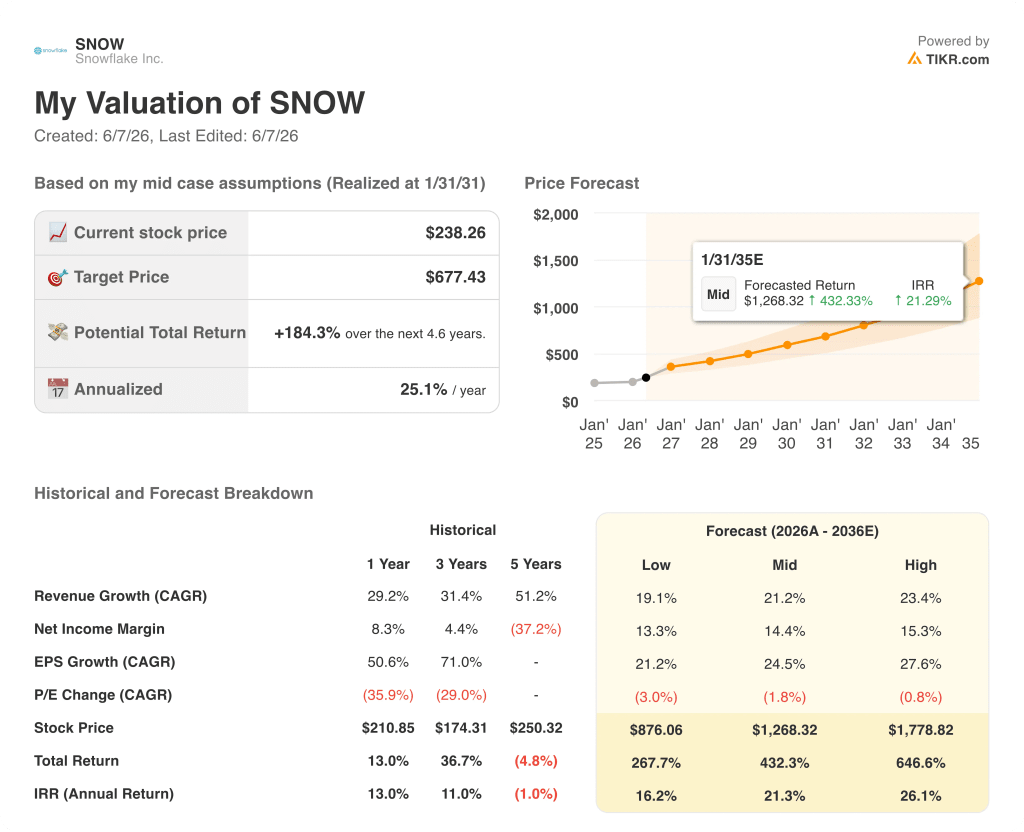

Is Snowflake Stock Undervalued in 2026? TIKR’s $677 Target Makes the Case

TIKR’s base case values Snowflake at approximately $677 by January 2031, implying around 184% total return from the current price of $238, or roughly 25% annualized over approximately 4.6 years.

The model’s scenario range reflects how much depends on whether Snowflake’s AI revenue contribution expands beyond CoCo into the broader agentic control plane the company is building.

If revenue growth stays in the low 19% range over the forecast period, the TIKR low case puts Snowflake stock at around $876 by January 2031, implying roughly 268% total return and around 16% annualized.

If the mid case at roughly 21% revenue CAGR plays out as CoCo adoption scales and CoWork gains enterprise traction, the model reaches around $1,268 by January 2035 with an IRR of roughly 21%.

Under the high case, where revenue grows at roughly 23% and net income margins expand toward 15%, the model projects around $1,779 by January 2031, implying around 647% total return and approximately 26% annualized.

The bear case is not zero-growth — it is that CoCo adoption stalls before reaching the full customer base, the consumption model limits revenue visibility, and the market rerates Snowflake back toward pre-earnings sentiment. The low-case IRR of roughly 16% still implies a stock significantly above today’s price.

Snowflake stock is undervalued if the Q1 AI inflection is structural. The TIKR model, built on roughly 21% revenue CAGR with expanding margins, implies the market has not yet repriced for what the last quarter made visible.

Is Snowflake stock a buy right now?

Snowflake stock carries 44 Buy or Outperform ratings from 48 analysts covering the stock, with a Street mean target of around $288 against a current price of $238.

The TIKR base case model puts fair value at approximately $677 by January 2031, implying around 25% annualized returns.

The bull case rests on CoCo driving sustained consumption acceleration across Snowflake’s 13,912 customers. The key variable: whether Q2 product revenue confirms the 34% growth rate seen in Q1.

What happened to Snowflake stock in Q1 FY27 earnings?

Snowflake surged around 38% on May 28 after Q1 FY27 revenue of $1.39 billion beat estimates of around $1.32 billion, with product revenue growing 34% year-over-year, up from 26% a year earlier.

The company raised its full-year product revenue outlook to $5.84 billion and signed a five-year, $6 billion deal with AWS. More than 30 analysts raised price targets on the same day.

Should You Invest in Snowflake Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Snowflake Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Snowflake Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SNOW stock on TIKR for Free →