Key Fundamental Metrics for CDNS Stock

- 52-Week Range: $262.75 to $416.69

- Current Stock Price: $376.19

- Street Consensus Target Price: ~$384

- Q1 2026 Revenue: $1.474B (+20% YoY)

- Q1 2026 Non-GAAP Operating Margin: 44.7%

- Q1 2026 Non-GAAP EPS: $1.96 (+25% YoY)

- Record Backlog: $8.0B

- FY2026 Revenue Guidance: ~17% YoY growth

- Mid-Case 10-Year Forward Stock Price Target: ~$848

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

The Software Layer Every AI Chip Can’t Skip

Cadence Design Systems (CDNS) makes electronic design automation (EDA) software that engineers use to design semiconductors. EDA is the environment where a chip is conceived, simulated, verified, and prepared for manufacturing before a single wafer is touched. Without it, modern chip design at advanced nodes wouldn’t be possible.

Every Nvidia GPU, every custom AI accelerator, every HBM memory chip runs through EDA tools before it reaches TSMC or Samsung’s fabs. As chip complexity has compounded alongside AI demand, so has the value of Cadence’s software.

The latest development takes that positioning further. At Computex last week, Cadence unveiled ChipStack AI Super Agent, which the company describes as the semiconductor industry’s first fully autonomous virtual engineer for chip design.

Built in partnership with Nvidia, it can independently execute complex workflows that previously took human engineers weeks to complete. CEO Anirudh Devgan said Cadence is leading the agentic AI transformation in semiconductor and system design, with its AgentStack platform now spanning the entire chip design spectrum from individual chips to 3D-IC and systems.

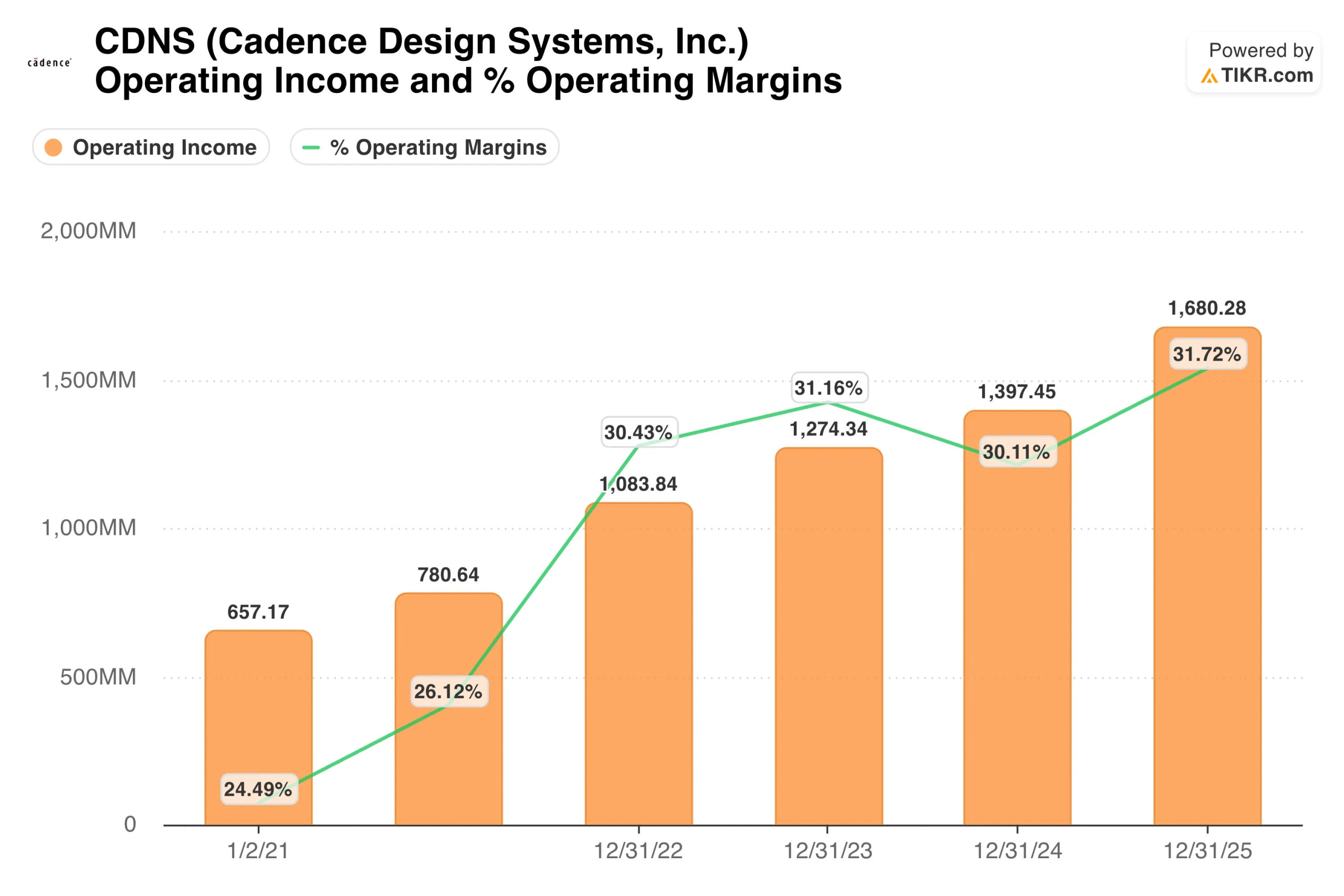

Operating income has grown from $657 million in 2021 to $1.68 billion in 2025, while GAAP operating margins expanded from around 24% to nearly 32%. The non-GAAP operating margin reached 44.7% in Q1 2026, meaning nearly half of every revenue dollar drops to operating income before tax. That is the quality characteristic that justifies the premium multiple and makes this business genuinely difficult to replicate.

See historical and forward estimates for Cadence Design Systems stock (It’s free!) >>>

A Record Backlog and a Guidance Raise That the Market Hasn’t Fully Priced

Q1 2026 results were strong across every meaningful line. Revenue grew 20% year over year to $1.474 billion. Non-GAAP EPS of $1.96 beat the prior year by 25%. Core EDA revenue grew 18%, hardware delivered a record quarter driven by AI and high-performance computing customers, and IP revenue grew 22%.

The backlog reached $8.0 billion at quarter end, with $4.0 billion expected to be recognized in the next twelve months. That forward visibility is unusual for a software business and reflects the multi-year subscription structure underpinning most of Cadence’s revenue. Management raised full-year 2026 revenue guidance to approximately 17% growth, with non-GAAP operating margins holding near current levels.

The stock sits about 10% below its 52-week high of $416.69, and the Street consensus target of around $384 sits just above the current price. That compressed upside to consensus is the honest tension in the setup: the fundamentals are excellent, but the valuation requires sustained execution.

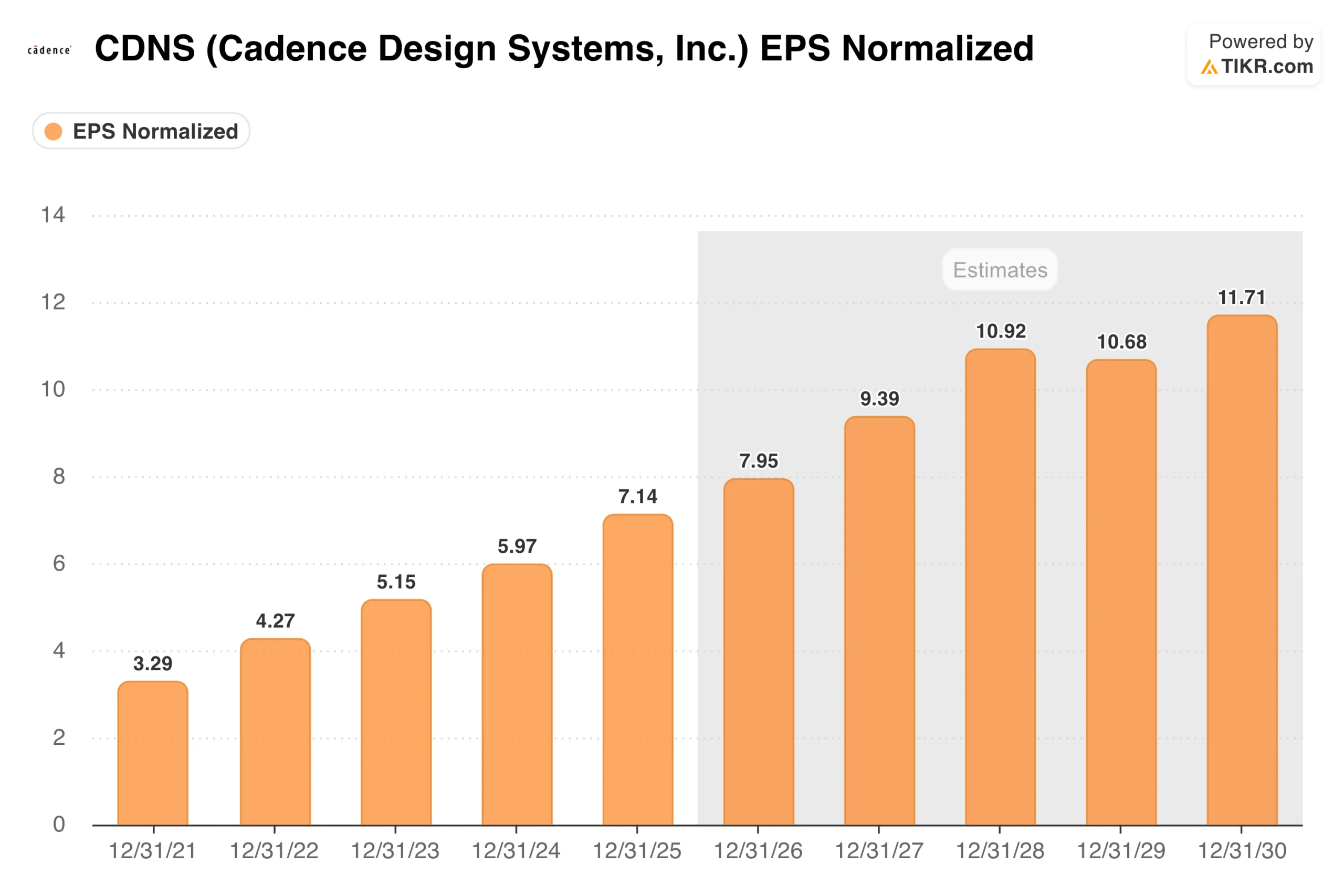

Normalized EPS has compounded from $3.29 in 2021 to $7.14 in 2025, a five-year CAGR of around 21%. Street estimates project continued growth to around $7.95 in 2026, stepping toward $9.39 in 2027 and $10.92 in 2028. That trajectory reflects both revenue growth and the operating leverage of a high-margin software business that doesn’t need proportional cost increases to grow earnings.

What the TIKR Valuation Model Says About CDNS at $376

TIKR’s mid-case valuation model targets around $848 for CDNS over a roughly nine-year horizon, implying a total return of around 125% or about 10% annualized. The model assumes revenue growing at around 10% annually, net income margins expanding to around 38%, and EPS growing at roughly 11% per year.

The low case lands at around $652 and the high case reaches around $1,076. Notably, the mid-case revenue assumption of around 10% is more conservative than the 17% Cadence is guiding to in 2026, making it a measured baseline rather than an optimistic one.

The key assumption worth examining is margin expansion toward 38% net income, which is plausible given the current non-GAAP operating structure but depends on continued pricing power and limited disruption from open-source EDA alternatives.

Build your own Valuation Model to value any stock (It’s free!) >>>

What the Bulls Are Betting On

- The EDA duopoly is structurally durable. Cadence and Synopsys together control the vast majority of the EDA market. Switching costs are extraordinarily high because chip designs are built around specific tool flows that engineers spend years learning.

- ChipStack AI Super Agent further raises switching costs. An autonomous design agent embedded into existing workflows makes Cadence’s tools increasingly central to how chips get built, not just necessary. Early access rolls out in the second half of 2026.

- The backlog provides genuine earnings visibility. $8.0 billion in performance obligations, with $4.0 billion recognized in the next 12 months, means a significant portion of 2026 revenue is already contracted, which is rare at this growth rate.

- The TSMC alliance deepens the moat. An expanded collaboration across N3, N2, A16, and A14 nodes ties Cadence’s tools directly to the world’s most advanced manufacturing processes.

What the Bears Are Watching

- The valuation leaves no room for disappointment. At around 46x NTM P/E, any guidance miss or margin pressure would quickly put meaningful pressure on the multiple.

- China exposure is a persistent tail risk. Revenue from China runs in the 12% to 13% range, and any tightening of export controls would remove a meaningful revenue stream with limited ability to replace it quickly.

- Cash declined sharply in Q1. Cash fell from $3.0 billion to $1.4 billion as acquisitions were funded, and total debt rose to nearly $2.9 billion. Still manageable at 0.74x net debt to EBITDA, but less pristine than a year ago.

Should You Invest in Cadence Design Systems?

The fundamental case is as clean as it gets in technology: a duopoly position in mission-critical software, 86% gross margins, a record backlog, and a new autonomous design product that generated one of the biggest single-day moves in the stock’s recent history.

The TIKR mid-case of around $848 reflects what a decade of compounding at a conservative growth rate produces, while the Street consensus of around $384 suggests the market sees the stock as roughly fairly valued today.

The constraint is valuation. At 46x forward earnings, there is limited tolerance for execution stumbles. For long-term investors who believe the AI chip design cycle is durable and that agentic tools deepen an already formidable moat, the current price is a reasonable entry.

For those who need more margin of safety, waiting for a pullback closer to the 52-week low range would be the more patient approach.

See how Cadence Design Systems performs against its peers in TIKR (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!