Key Fundamental Metrics for TT Stock

- 52-Week Range: $348.06 to $503.47

- Current Stock Price: $456.84

- Street Consensus Target Price: ~$520

- Q1 2026 Revenue: $4.97B (+6% YoY organic)

- Q1 2026 Adjusted EPS: $2.63 (+7% YoY)

- Q1 2026 Record Backlog: $10.7B (up 30%+ vs year-end 2025)

- FY2026 Adjusted EPS Guidance: $14.75 to $14.95

- Mid-Case 10-Year Forward Stock Price Target: ~$863

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

The Boring Industrial That Became an AI Infrastructure Play

Trane Technologies (TT) makes the heating, ventilation, and air conditioning systems that keep buildings comfortable and data centers from overheating. That second use case has become the more interesting one. As hyperscalers pour capital into AI infrastructure at a pace that shows no signs of slowing, the demand for high-performance cooling has become one of the most durable spending commitments in the market.

The numbers from Q1 2026 reflect that directly, as America’s commercial HVAC bookings were up around 40% year over year, with Applied bookings, the large-scale custom systems that go into data centers, hospitals, and university campuses, up over 100%.

The company’s total backlog hit a record $10.7 billion, up more than 30% from year-end 2025. A book-to-bill ratio of around 150% in commercial HVAC means TT is booking orders significantly faster than it can ship them, which is a different problem than most industrials face right now.

Revenue has grown steadily from $14.1 billion in 2021 to $21.3 billion in 2025, while gross margins have expanded from around 31% to nearly 36% over the same period. That combination, consistent revenue growth alongside margin expansion, is what separates a quality compounder from a commodity industrial. Most companies that scale this quickly experience margin pressure. TT has done the opposite.

See the exact moment Wall Street upgrades a stock before the rest of the market piles in — track analyst rating changes in real time with TIKR for free →

Bookings Lead Revenue, and the Backlog Points to Acceleration in the Second Half

Q1 organic revenue grew 3%, a modest headline that understates the trajectory. The bookings picture tells a more interesting story about where the business is heading. Management guided for around 10% commercial HVAC revenue growth in Q2, accelerating to low-teens growth in the second half as the record backlog converts to shipped revenue.

CEO Dave Regnery noted on the Q1 earnings call that the project pipeline across key verticals remains robust and rapidly growing, and that services revenue, which represents about a third of total enterprise revenue and has compounded at a low-teens rate since 2020, continues to grow at double digits. Services matter here because they are recurring, higher-margin, and tied to installed equipment that TT has been placing at a record pace.

The Stellar Energy acquisition, a modular energy and cooling systems provider with a backlog of roughly $1 billion that TT expects to convert largely in 2026, adds another layer of data center exposure. It’s the kind of deal that doesn’t move headline revenue immediately but deepens TT’s position in exactly the vertical driving the bookings surge.

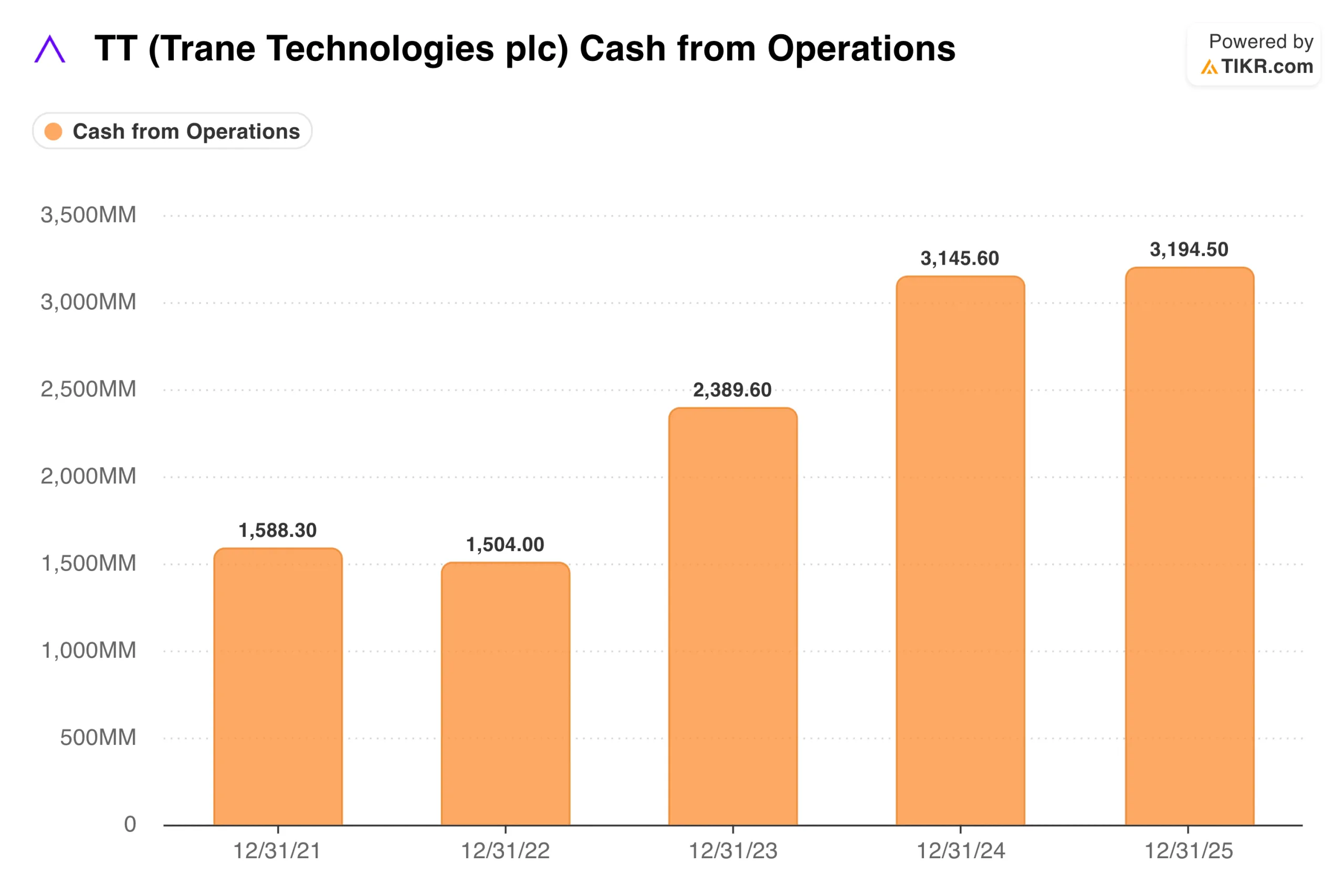

Cash from operations grew from $1.6 billion in 2021 to $3.2 billion in 2025, nearly doubling over four years. Management targets free cash flow at or above 100% of adjusted net earnings, and the Q1 2026 YTD free cash flow of $573 million compares favorably to $230 million in the same period last year.

That cash generation is what funds the $2.8 to $3.3 billion in planned capital deployment for 2026, including a 12% dividend increase to $4.20 per share annualized, share repurchases, and continued M&A.

See what analysts think about TT stock right now (Free with TIKR) >>>

What the TIKR Valuation Model Says About TT at $457

TIKR’s mid-case valuation model targets around $863 for TT over a roughly nine-year horizon, implying a total return of around 89% or about 8% annualized. The model assumes revenue growing at around 7% annually and net income margins expanding to around 15%, with EPS growing at roughly 8% per year as the P/E multiple stays roughly stable.

The low case is around $687, and the high case is around $1,055. The Street consensus target of around $520 is considerably more conservative, reflecting a nearer-term view, and still implies about 14% upside from the current price.

The TIKR mid-case is more constructive simply because it runs out a full decade, allowing the compounding of both earnings growth and the data center tailwind to accumulate over time.

The key assumption separating the cases is whether the data center cooling cycle sustains long enough to justify a re-rating toward growth-company multiples, or whether chip efficiency improvements eventually reduce cooling intensity and leave TT trading on its traditional industrial earnings profile.

What the Bulls Are Betting On

- The backlog provides unusual visibility. A $10.7 billion backlog with a book-to-bill of 150% in commercial HVAC means the second-half revenue acceleration is not a forecast; it’s already in the order book.

- Services provide a durable earnings floor. Low-teens compounding in a business that represents a third of revenue and is tied to installed equipment creates a reliable base that doesn’t disappear when new construction softens.

- Cash generation funds compounding. Nearly $3.2 billion in operating cash flow supports a growing dividend, buybacks, and M&A without straining the balance sheet. Net debt-to-EBITDA is a conservative 0.78x.

- The margin trajectory is still moving in the right direction. Gross margins have expanded roughly 500 basis points over five years on a business that was already considered high quality.

What the Bears Are Watching

- EMEA softness adds another layer. Middle East headwinds cost TT roughly $25 million in Q1 revenue, and around $50 million is expected in Q2, a modest but real drag that management is navigating rather than solving.

- The data center cycle is the swing variable. If chip efficiency improvements reduce cooling intensity, the Applied bookings surge could moderate faster than the current backlog suggests, and the premium multiple would need to come down with it.

- The stock is not cheap. At nearly 30x NTM P/E on a business growing organically at 7%, TT requires continued execution on margin expansion and backlog conversion to justify the current price, let alone the Street target.

- Transport remains a drag. Thermo King, TT’s transport refrigeration business, faces a mid-single-digit market decline in 2026, with recovery not expected until late 2026 or into 2027. It’s a manageable headwind, but it limits the upside on total reported revenue growth.

Access Professional Tools to Analyze TT stock on TIKR for Free →

Should You Invest in Trane Technologies?

TT sits in an unusual position for an industrial company: it has a century-old HVAC core business that has become structurally more valuable because of a technology trend it didn’t create. The record backlog, the services flywheel, the cash generation, and the margin expansion all point in the same direction.

The Street consensus target of around $520 implies meaningful upside from current levels, and the TIKR mid-case of around $863 assumes the compounding continues over a full decade.

The honest tension is valuation, and at roughly 30x forward earnings, TT is priced for continued execution, and any meaningful slowdown in data center orders would put pressure on both earnings estimates and the multiple simultaneously.

For long-term investors who believe the cooling infrastructure buildout is durable and that TT’s services base provides a reliable earnings floor underneath it, the current price offers a reasonable entry into a genuinely high-quality business.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!