Key Fundamental Metrics for SMCI Stock

- 52-Week Range: $19.48 to $62.36

- Current Stock Price: $41.64

- Street Consensus Target Price: ~$38

- Q3 FY2026 Revenue: $10.2B (+123% YoY)

- Q3 FY2026 Non-GAAP Gross Margin: 10.1%

- Q3 FY2026 Non-GAAP EPS: $0.84 (beat estimates by ~36%)

- FY2026 Full-Year Revenue Guidance: $38.9B to $40.4B

- Mid-Case 10-Year Forward Stock Price Target: ~$112

Value your favorite stocks like SMCI with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

The March Collapse: What Happened and Where the Stock Stands Now

On March 19, 2026, the DOJ unsealed a federal indictment charging three individuals with ties to Super Micro Computer (SMCI), including co-founder Yih-Shyan “Wally” Liaw, with conspiring to illegally divert approximately $2.5 billion worth of AI servers containing advanced Nvidia GPUs to customers in China, in violation of U.S. export control laws. SMCI itself was not named as a defendant, and the company publicly stated that the alleged conduct directly contravened its own policies and compliance controls.

The market didn’t wait for nuance, with shares falling 33% in a single session, touching a 52-week low of $19.48.

The stock has since recovered to $41.64, nearly doubling from that low, but it hasn’t come close to reclaiming the $62.36 52-week high. Super Micro responded by appointing a new acting Chief Compliance Officer, engaging a forensic accounting firm to conduct an independent internal investigation, and reshuffling its board.

The legal cloud hasn’t fully lifted, and a class action lawsuit with a lead plaintiff deadline in late May adds another layer of headline risk that the market is still working through.

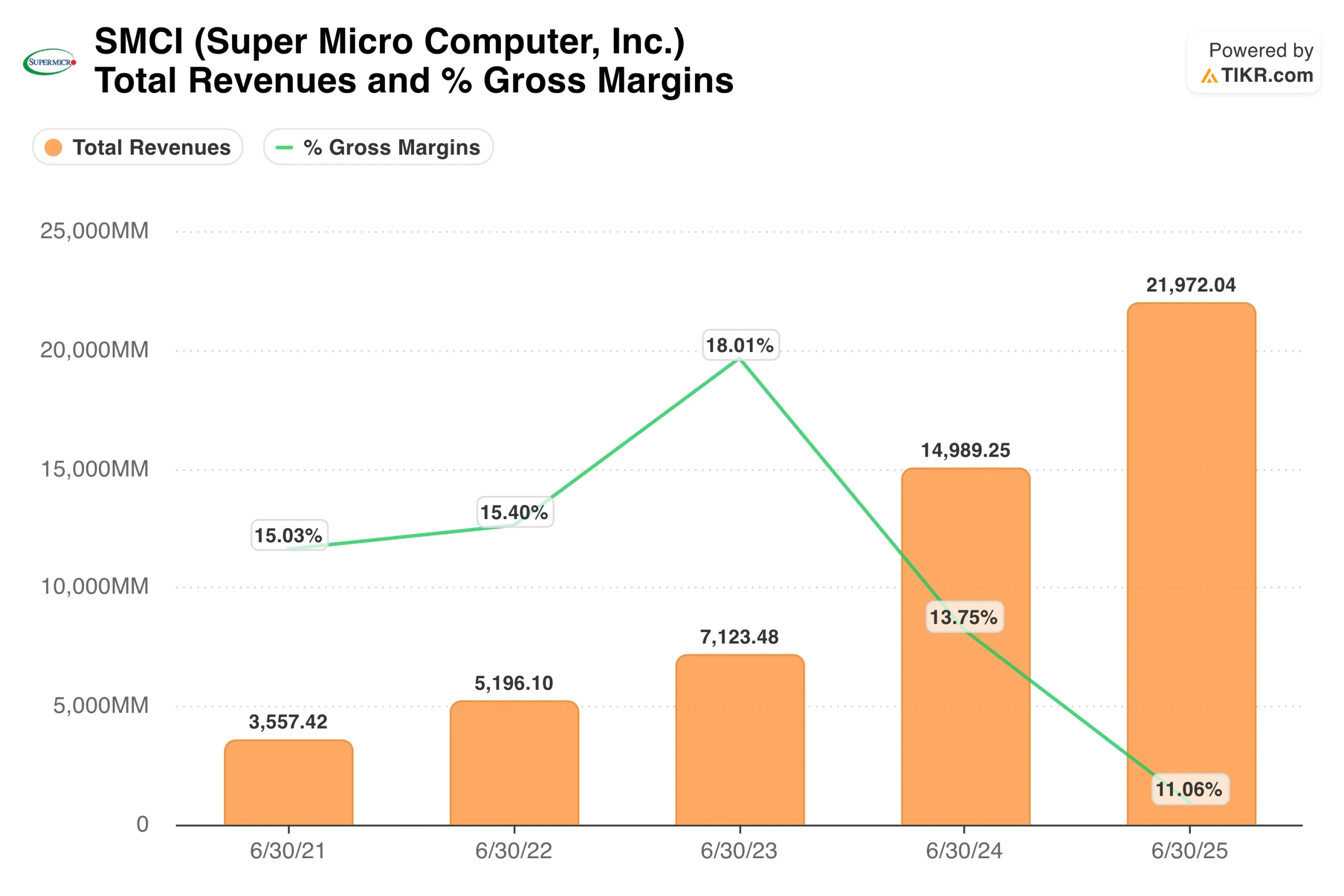

The revenue chart captures a business that has scaled at a pace most hardware companies never approach. Revenue grew from $3.6 billion in fiscal 2021 to nearly $22 billion in fiscal 2025, a compounded rate of around 57% over four years.

The gross margin line tells a different story, as margins peaked at 18% in fiscal 2023 and have steadily compressed since, reaching 11% in fiscal 2025 as the company prioritized market share in AI server buildouts over pricing discipline.

That compression is the central tension in the SMCI thesis. Scale is not the question. Whether margins can stabilize and recover while the company navigates a legal overhang remains to be seen.

Analyze your favorite stocks like Super Micro Computer with TIKR (It’s free) >>>

123% Revenue Growth, a Margin Recovery, and a Revenue Miss All in the Same Quarter

Q3 fiscal 2026 results, reported May 5, captured the contradiction that defines SMCI right now. Revenue came in at $10.2 billion, up 123% year over year, but missed the $12.3 billion consensus by a wide margin.

The shortfall wasn’t demand, as CEO Charles Liang told analysts on the earnings call that several large customers lacked the power and networking infrastructure required to accept shipments on schedule, and that the company expected to capture that revenue in the coming quarters.

The gross margin recovery was the number that moved the stock. Non-GAAP gross margin came in at 10.1%, up from 6.4% in Q2 and nearly 50% above what analysts had expected. Non-GAAP EPS of $0.84 beat the $0.62 consensus by around 36%.

For Q4, management guided revenue of $11 billion to $12.5 billion and raised full-year guidance to $38.9 billion to $40.4 billion. The stock jumped roughly 20% in after-hours trading on the print.

The EPS chart provides important context for how the earnings trajectory has evolved. Normalized EPS grew from $0.25 in fiscal 2021 to $2.21 in fiscal 2024, before dipping to $2.06 in fiscal 2025 as margins compressed.

Street estimates project a meaningful step-up from here, reaching around $2.60 for fiscal 2026 and climbing toward $3.71 by fiscal 2028. The Q3 beat, at $0.84 on a non-GAAP basis versus $0.62 expected, puts the full-year 2026 estimate within reach and suggests the margin recovery is at least partially real.

The enterprise channel data reinforces that read. Enterprise revenue hit $2.8 billion in Q3, or 28% of total, up 46% year over year and 45% quarter over quarter. Enterprise deployments tend to carry higher margins and more service content than hyperscale OEM work, which is what drove the Q2 margin trough. The shift in customer mix toward enterprise is exactly what the bull case has been waiting for.

See what analysts think about SMCI stock right now (Free with TIKR) >>>

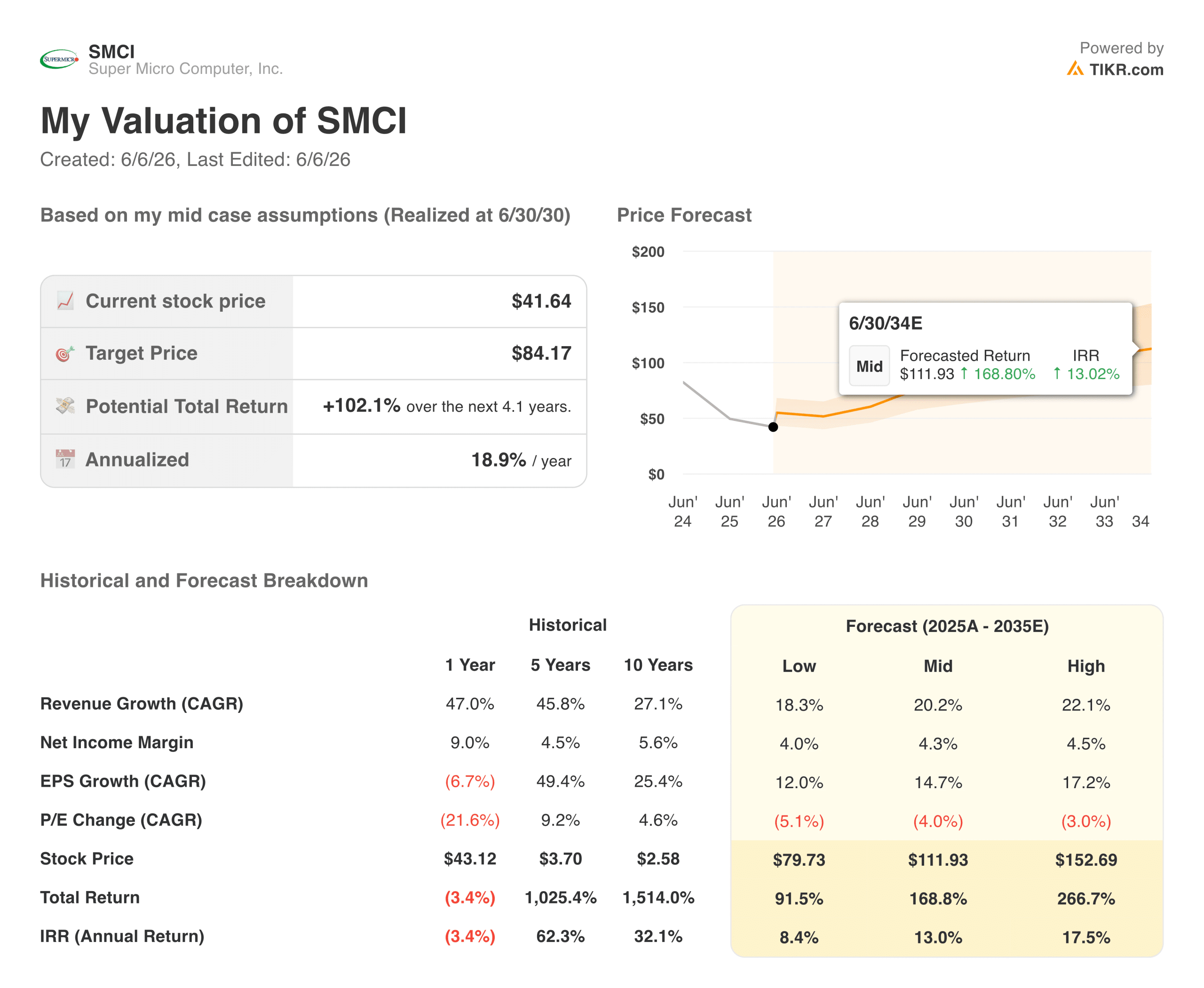

What TIKR’s Valuation Model Says About SMCI at $41

TIKR’s mid-case valuation model targets around $112 for SMCI, implying a total return of around 169% from the current price over roughly eight years, or around 13% annualized. The model assumes revenue growing at around 20% annually and net income margins expanding to around 4%, with EPS growing at roughly 15% per year as the P/E multiple compresses gradually from current levels.

The low case lands at around $80, still nearly double the current price over the same horizon. The high case reaches around $153. That range is wide, and the width is intentional, given that the outcome here depends heavily on factors outside the income statement.

One honest note on the Street consensus: the average analyst target of around $38 sits below where the stock currently trades, meaning the consensus view is that SMCI is already fairly valued or slightly stretched at $41.

The TIKR model’s more constructive output reflects a longer time horizon and assumes the margin recovery continues, the legal overhang resolves without direct liability to the company, and the AI infrastructure buildout sustains the revenue ramp. Those are real assumptions, not certainties.

Value Super Micro Computer instantly (Free with TIKR) >>>

What the Bulls Are Betting On

- The margin recovery is structural, not seasonal. The Q3 non-GAAP gross margin of 10.1% came in well above expectations and reflected a genuine shift in customer mix toward higher-margin enterprise deployments. If Q4 holds at or above 9%, the recovery has legs.

- Revenue timing, not demand, drove the Q3 miss. Management’s explanation that customer site readiness caused the shortfall is consistent with what large-scale AI infrastructure deployments look like in practice. The Q4 guidance range of $11 billion to $12.5 billion implies the deferred revenue is real and coming.

- SMCI is not the defendant. The DOJ indictment names three individuals, not the company. Super Micro’s swift compliance response, including a new chief compliance officer, a forensic accounting firm, and board changes, is the playbook for a company trying to get ahead of regulatory risk rather than ignore it.

- The valuation is genuinely inexpensive for the growth rate. At roughly 0.67x NTM EV/Revenue and 13.8x NTM P/E on a business growing over 100% year over year, SMCI trades at a significant discount to AI infrastructure peers.

What the Bears Are Watching

- The Street isn’t buying it. A consensus target below the current stock price is a meaningful signal. Most analysts covering SMCI are not modeling a clean recovery from here, and the governance uncertainty makes it difficult to assign a clean multiple.

- The legal situation is not resolved. An ongoing SEC investigation, an open DOJ case, multiple securities class action lawsuits, and a forensic accounting review running in parallel create a headline risk environment that could pressure the stock at any moment, regardless of operating results.

- Gross margins remain structurally thin. Even after the Q3 recovery, 10% gross margins leave almost no room for error. Competitors like Dell and HPE are chasing the same hyperscale customers, and pricing pressure has historically been SMCI’s biggest margin headwind.

- The cash conversion cycle doubled in one quarter. Days of inventory jumped from 63 to 106, and days sales outstanding rose from 49 to 85 in Q3, reflecting the operational strain of the revenue timing issues. Net debt sits at $7.8 billion. A prolonged revenue delay would put real pressure on working capital.

Should You Invest in Super Micro Computer?

SMCI is one of the harder stocks to frame cleanly right now, and that’s by design of the situation rather than a flaw in the analysis. The business is growing faster than almost any hardware company in the public markets. The margin recovery in Q3 was real and came in well ahead of expectations. The Q4 guidance implies the revenue timing story holds.

But the legal overhang is genuine, and dismissing it entirely would be a mistake. The Street consensus sitting below the stock price is a signal worth taking seriously, not because analysts are always right, but because it reflects how much uncertainty remains embedded in the outcome.

For investors who believe the DOJ and SEC situations will resolve without direct corporate liability, and that the enterprise channel mix shift continues to drive margins higher, the TIKR mid-case of around $112 represents a compelling long-term entry.

For investors who need cleaner governance and more margin visibility before committing capital, there is no shame in waiting for Q4 results to confirm whether the recovery is durable.

See analysts’ growth forecasts and price targets for Super Micro Computer (It’s free) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!