Key Takeaways for Cisco Systems Stock as of July 2026

- Cisco returned $2.9 billion to shareholders in its fiscal third quarter of 2026, split between $1.7 billion in dividends and $1.3 billion in buybacks, with $9.6 billion still authorized for repurchases.

- The quarterly dividend rose to $0.42.

- Cisco’s payout ratio fell to 49%, down from 74% two years earlier, even as the stock’s run higher pushed the dividend yield down to 1.5% as of mid-July, a shift that leaves the payout better covered but less rewarding to chase for yield alone.

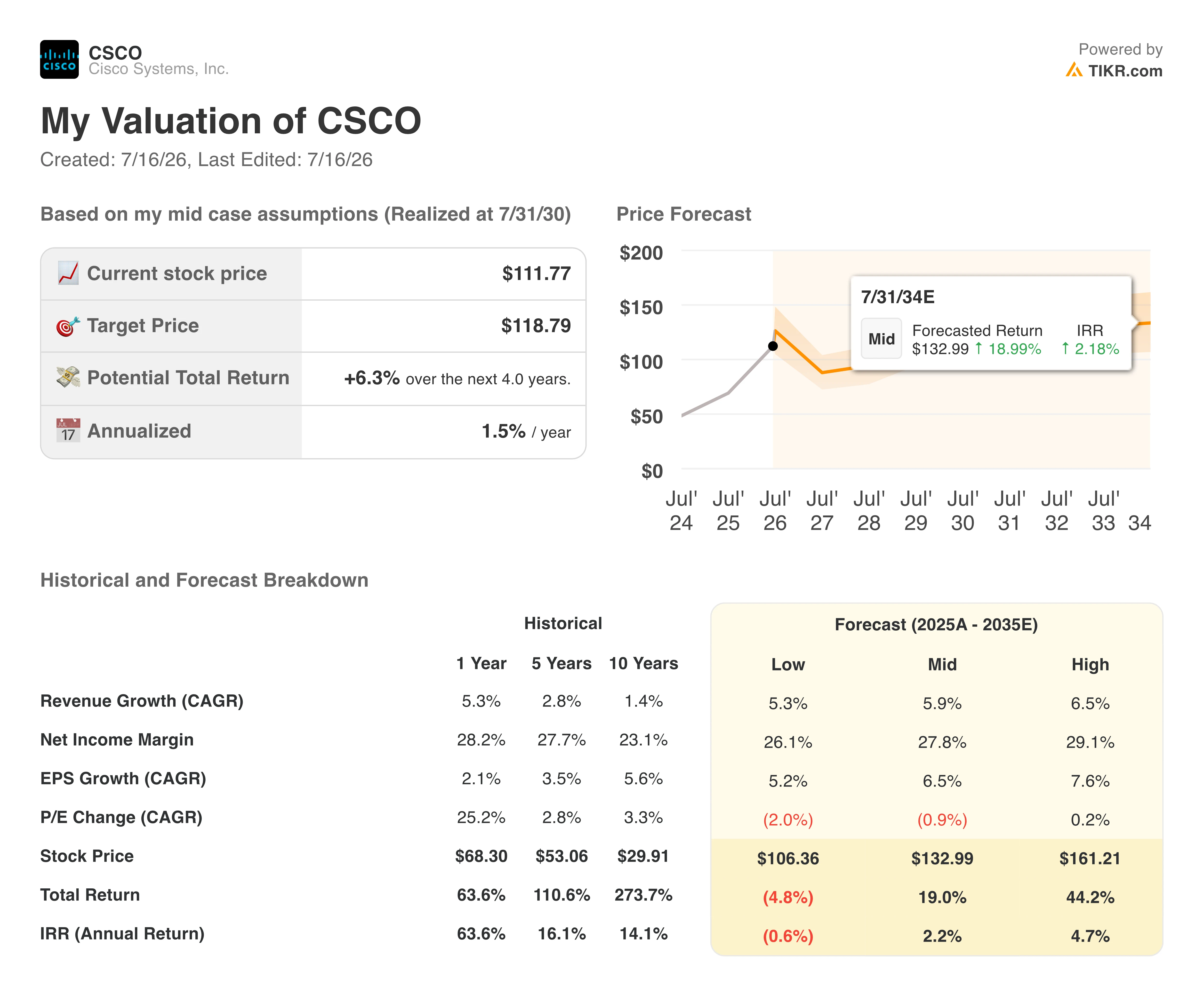

- TIKR’s mid-case model puts Cisco stock’s target price at $119 by July 2030, worth a 6% total return, or roughly 2% annualized, from today’s $112 share price.

Cisco Systems Turns AI Infrastructure Growth Into Cash Cisco Stock Investors Can Bank On

Cisco Systems (CSCO) closed its fiscal third quarter of 2026 with record revenue of $15.8 billion, up 12% year over year, a figure CFO Mark Patterson tied directly to what the company is now returning to shareholders. On the Q3 earnings call, held May 13, 2026, Patterson said Cisco returned $2.9 billion to shareholders in the quarter, made up of $1.7 billion for the quarterly cash dividend and $1.3 billion in share repurchases, pushing the year-to-date capital return total past $9 billion with $9.6 billion still available under the buyback program.

That figure follows a quarter in which non-GAAP earnings per share reached $1.06, up 10%, a pace CEO Chuck Robbins attributed to record product orders. Robbins told analysts total product orders grew 35% year over year, with AI infrastructure orders from hyperscalers alone hitting $1.9 billion in the quarter, up from $600 million a year earlier. Set against that order strength, Robbins raised the company’s full-year AI infrastructure order target to approximately $9 billion, 4.5 times the prior year’s total.

Even so, the dividend commentary stayed narrowly framed around capital return mechanics rather than a specific payout target. Patterson noted operating cash flow fell 7% in the quarter to $3.8 billion, a decline he attributed to continued investment to meet AI infrastructure demand. He also flagged a restructuring plan carrying up to $1 billion in pretax charges, with $450 million landing in fiscal Q4, framed not as a savings program but as a reallocation toward silicon, optics, security and AI.

For Cisco stock holders watching the dividend, the message from the call is that capital return is riding alongside an aggressive reinvestment cycle, not competing against it. Management’s own words point to a company generating enough scale, in record revenue, record orders and double-digit earnings growth, to fund both the buildout and the payout at once.

Cisco’s Payout Ratio Keeps Falling Even As Its Dividend Keeps Rising

Cisco’s quarterly dividend climbed to $0.42 as of the most recent declaration, up from $0.41, where it had held for four consecutive quarters dating back to April 2025.

Before that, the payout sat at $0.40 for three straight quarters through January 2025. The pattern reads as a steady climb rather than a single outsized raise.

Cisco’s payout ratio has fallen sharply over the same stretch, from 74% in July 2024 to 49% as of the most recent quarter. That decline corroborates what Patterson described on the call: earnings growing faster than the dividend itself, freeing up room in the payout even as the per-share amount ticks higher.

Cisco stock’s dividend yield has moved in the opposite direction, falling from 2.4% in July 2025 to 1.5% as of July 15, 2026, with the NTM yield dipping as low as 1.4% at the end of June. That decline says less about the dividend than about the stock. Cisco shares have climbed enough that the same, growing payout now buys less yield, leaving Cisco stock’s income case resting more on durability than on current yield.

Bulls will point to a payout ratio under 50% as room to keep raising the dividend for years. Bears will note a 1.5% yield gives income-focused buyers little reason to chase Cisco stock at $112 a share.

TIKR’s $119 Target Makes Cisco Systems Stock A Modest Grower, Not A Reinvented One

TIKR’s mid-case valuation model puts Cisco Systems stock’s target price at $119 by July 2030, a potential total return of 6% from the current $112 share price, working out to an annualized return of 2% per year.

That return profile positions Cisco stock as a name priced for stability rather than a re-rating. The model’s mid-case assumes revenue growth near 6% annually and a net income margin holding near 28%, with the dividend contributing one piece of the total return rather than driving it.

The case for reaching that target rests on the AI infrastructure order book Robbins described on the call, orders already running ahead of the company’s own prior full-year expectations, plus a networking portfolio that has now grown orders in double digits for seven straight quarters.

If that order strength converts to revenue at the pace management guided for fiscal 2026, Cisco’s scale and its 34% non-GAAP operating margin in the third quarter give the target room to hold.

Should You Invest in Cisco Systems, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Cisco Systems, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Cisco Systems, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CSCO stock on TIKR for Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!