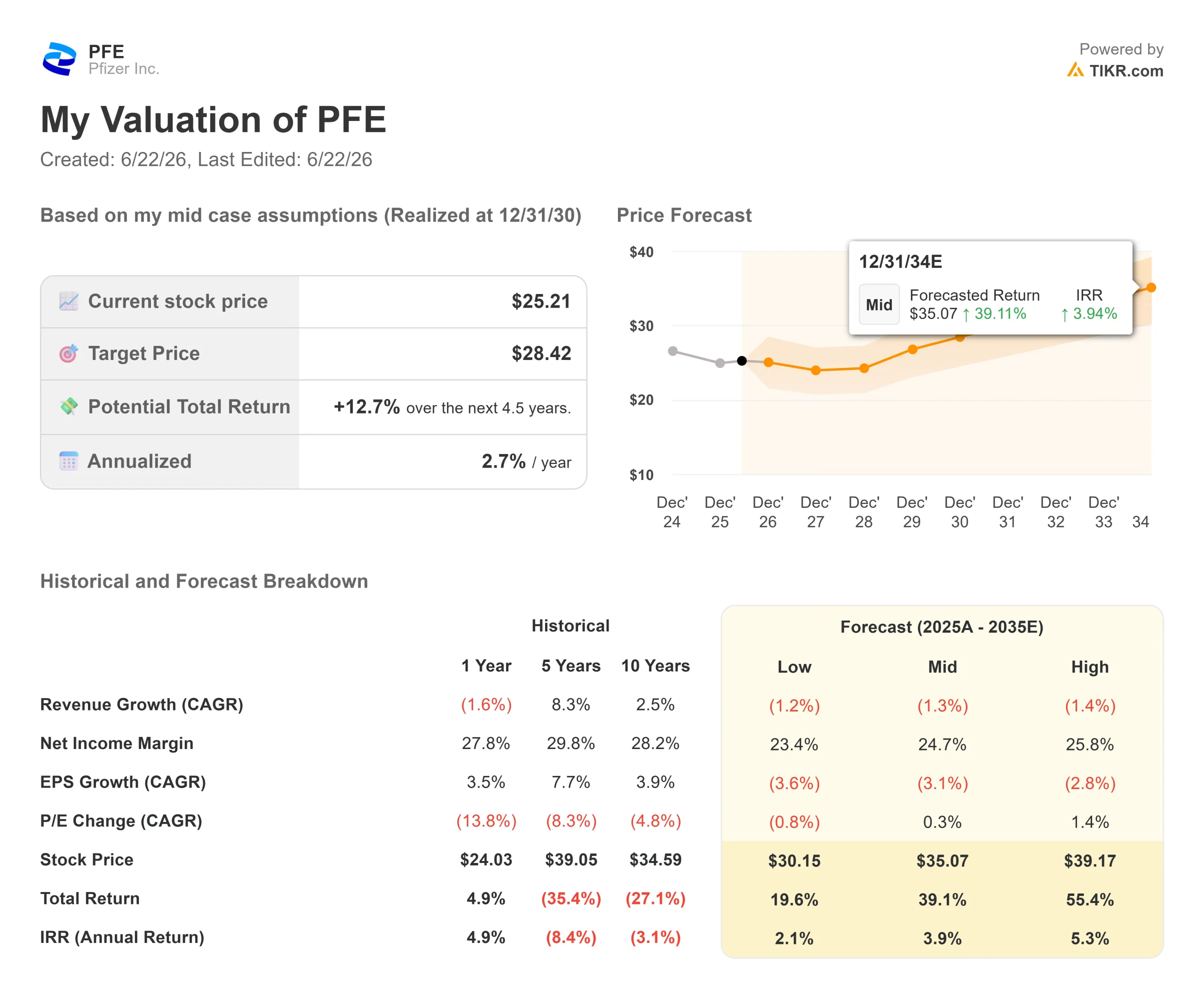

Key Stats for Pfizer Stock

- Current Price: $25.21

- Target Price: ~$28

- Street Target (Mean): ~$29

- Potential Total Return (Mid): ~13%

- Annualized IRR (Mid): ~3% / year

- Q1 2026 Earnings Reaction: +0.30% (5/5/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Pfizer Inc. (PFE) is worth less than half of what it was at the end of 2021. The stock closed at $25.21 on June 18, down roughly 57% from the $59.05 it fetched when COVID sales were peaking. Investors keep circling one question: Is anything large enough coming to replace that lost revenue?

Pfizer’s answer is obesity. The company has built a weight-loss pipeline around its roughly $10 billion acquisition of Metsera, and it is racing to launch its first product in 2028. That timing is deliberate because a patent cliff hits over the same window. So the debate is whether a late entrant can build a franchise big enough to matter in a market Eli Lilly and Novo Nordisk already own. The stock price says the market is not convinced.

Why The Obesity Bet Exists

Start with the hole it is meant to fill. Several of Pfizer’s largest franchises lose U.S. patent protection between 2025 and 2028, including its blood thinner Eliquis and part of its Prevnar pneumococcal vaccine family. The heaviest cluster falls in the next two years, with cancer drugs Ibrance and Xtandi following in 2027, according to BioSpace.

The foundation is Metsera, bought for an upfront enterprise value of about $7 billion, with milestones that can reach about $10 billion. Its lead asset is berobenatide, an investigational GLP-1 receptor agonist, a class of injectable weight-loss drugs that mimic a gut hormone to curb appetite. What sets it apart is the dosing: Pfizer is developing it as a once-monthly maintenance shot, against the weekly injections that define the market today.

The Data Is Solid, Not Spectacular

The latest proof point came just before the company’s June 8 appearance at the Goldman Sachs healthcare conference. On June 6, Pfizer presented Phase 2b data showing berobenatide delivered up to 15.9% non-placebo-adjusted weight loss at 32 weeks, with no plateau. Shares slipped about 1.3% on the day as analysts split on the read.

The skeptical case is simple. Guggenheim, BMO Capital Markets, and Leerink called the results solid but undifferentiated. For context, Eli Lilly’s tirzepatide produces roughly 22% weight loss, and its next-generation retatrutide has reached nearly 30%. Berobenatide is not winning on the headline number.

CEO Albert Bourla’s rebuttal is that the headline number is not the whole contest. He pointed to switch studies, where berobenatide only has to prove it is not inferior when patients move over from a weekly drug at their weight plateau. “I think we will achieve significant number of switches just because of this convenience,” he said. He also argued the salesforce is a structural edge: “When it comes to commercial capabilities, Pfizer is not Novo Nordisk.” On cost, he cited a manufacturing advantage of “a factor of 10 to 14 or 15 in terms of syringes” and active ingredient versus rivals, meaning Pfizer can scale without the heavy capacity spending Lilly and Novo are making.

The Core Business Can Fund The Wait

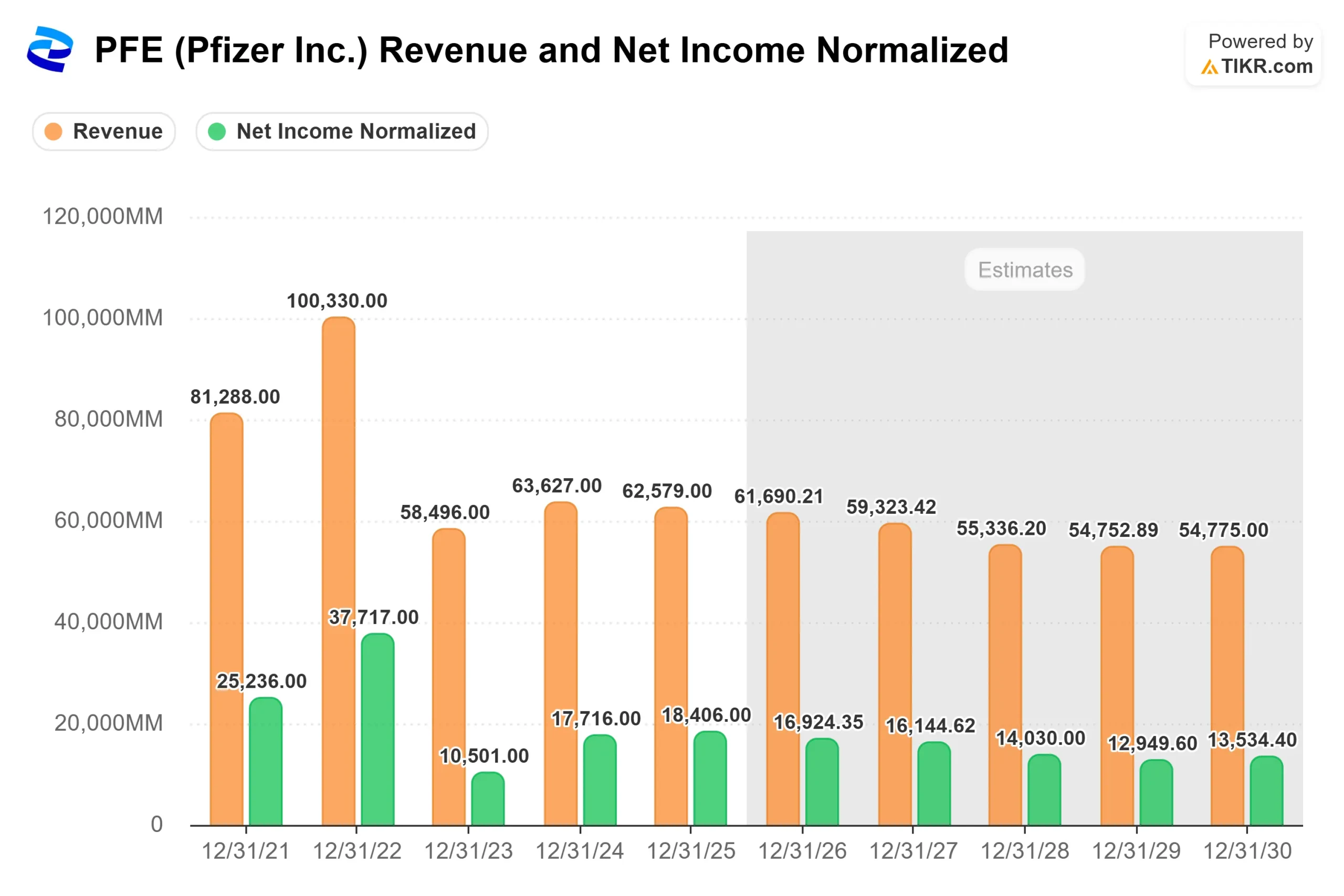

Because this is a multiyear story, the near-term question is whether today’s business pays the bills while the pipeline matures. It largely does. Pfizer’s portfolio of new and acquired products generated $3.1 billion in Q1 2026, up 22% operationally, which Bourla called a “$12 billion annualized business.” Its Seagen oncology unit grew 20% in the quarter, and migraine drug Nurtec grew 42%, both figures he cited at the conference.

That execution supports a 6.9% NTM dividend yield, per TIKR, giving investors a reason to wait. The drag is COVID: management cut 2026 COVID revenue guidance to about $5 billion from $6.5 billion, and Bourla flagged the treatment piece as the wild card because it tracks infection waves the company cannot forecast.

See historical and forward estimates for Pfizer stock (It’s free!) >>>

What The Stock Already Reflects

The skepticism shows up in the multiple. Pfizer trades near 8.9x NTM P/E, a steep discount to peers: Eli Lilly sits around 29.5x and Johnson & Johnson around 19.4x, while only Bristol-Myers Squibb, near 8.8x, keeps Pfizer company, per TIKR’s Competitors data. The market is pricing PFE like a high-yield bond, not a company about to enter a major new market.

Whether that discount is a trap or an opportunity hinges on the pipeline. Recent news did not help: on June 18, Pfizer said CFO Dave Denton would leave on August 15 for a consumer-goods role, with Cecile Guegan named interim. The stock fell about 3% as Scotiabank flagged the timing, though Pfizer reaffirmed full-year 2026 guidance the same day.

See how Pfizer performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $25.21

- Target Price (Mid): ~$28

- Potential Total Return (Mid): ~13%

- Annualized IRR (Mid): ~3% / year

See analysts’ growth forecasts and price targets for Pfizer stock (It’s free!) >>>

The model leans on two revenue assumptions that tell the story: a mid-case revenue CAGR of around negative 1% through 2030 and a net income margin near 25%. In other words, it gives Pfizer almost no credit for obesity and relies on cost discipline plus the dividend. The margin driver is the manufacturing optimization program, targeting about $7.2 billion in net savings by the end of 2026. The primary risk is the patent cliff outrunning new launches before 2028.

The upside: obesity and a stabilizing core reset growth expectations, and the depressed multiple expands.

The downside: Berobenatide lands third in a saturated market, and the stock stays a value trap with a yield.

Conclusion

The obesity thesis comes down to one test: Berobenatide’s Phase 3 program. The first of 10 pivotal studies is already running, with a first approval targeted for 2028. What matters is not peak weight loss but whether the switch and monthly-dosing trials prove non-inferiority cleanly enough to give the commercial team something to sell. A clean readout makes the 2028 launch real and gives the discounted multiple a reason to lift. A messy one leaves Pfizer a high-yield holding fighting a patent cliff with a third-place drug. Watch the Phase 3 data through 2027 ahead of that 2028 window. Until then, the market is paying you nearly 7% to wait.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Pfizer?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Pfizer, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Pfizer alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!