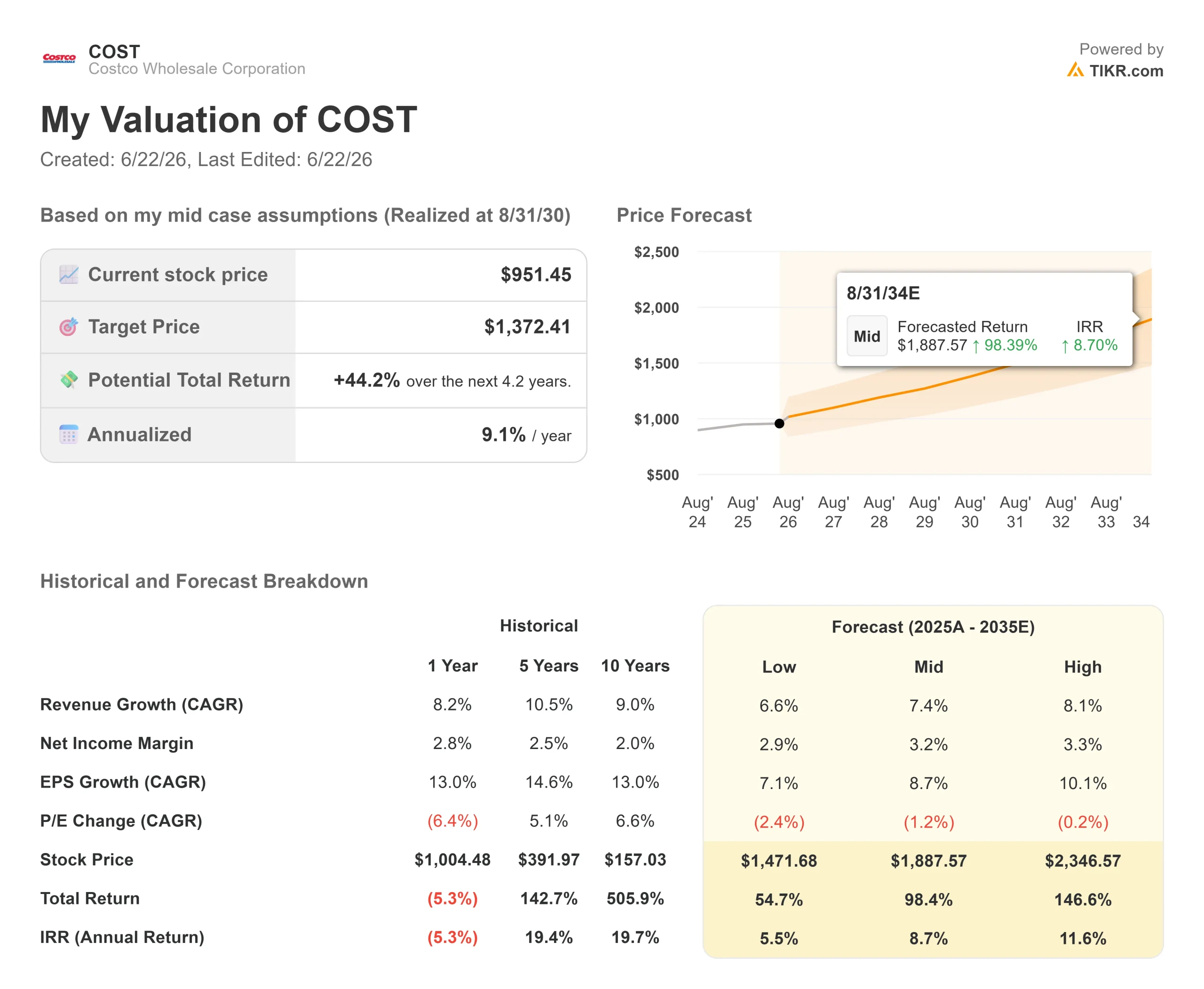

Key Stats for Costco Stock

- Current Price: $951.45

- Target Price (Mid): ~$1,370

- Street Target: ~$1,083

- Potential Total Return: ~44%

- Annualized IRR: ~9% / year

- Earnings Reaction: -3.91% (May 28, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Costco Wholesale Corporation (COST) posted record revenue and 15% earnings growth last quarter, yet the stock sold off anyway. Shares closed at $951.45 on June 18, about 13% below the all-time high of $1,096.50 set on May 19. That gap between strong results and a falling price is the real story, and it puts unusual weight on one comment from the latest earnings call.

Asked about capital allocation, CFO Gary Millerchip said that “at our current valuation, special dividend is typically the most effective way to return excess cash without giving up the flexibility to keep investing in growth.” He added a caveat that reframes the question: because the stock is far higher than at the last special dividend, the cash balance would need to be larger to deliver a similar yield.

Why The Payout Question Is Live

The math is the catalyst. Bernstein’s analysis, reported by CNBC, notes Costco’s last special dividend of $15 per share in January 2024 yielded about 2.4%, so matching that yield today would take roughly $24 per share. Costco can afford it: TIKR data shows LTM net debt of negative $11.76 billion, meaning the company holds far more cash than debt. The question is timing, not capacity.

The Quarter Underneath The Selloff

This was a valuation reaction, not a fundamental one. Net sales rose 11.6% to $69.15 billion and net income grew 15% to $2.192 billion, or $4.93 per share. The catch: adjusted EPS of $4.93 came in just under the $4.97 the Street expected, a miss of under 1%. At a near-48x earnings multiple, that is enough to move the stock, which fell 3.91% on the report.

The quality held up underneath. Comparable sales rose 9.8%, but a cleaner 6.6% after stripping out gas inflation and currency. Membership fee income, the high-margin engine of the model, grew 10.7%, and the U.S. and Canada renewal rate ticked up to 92.2%. Renewal economics like that are what let a retailer run thin merchandise margins, compound earnings year after year.

The standout was gas. CEO Ron Vachris said the final five weeks of the quarter were “becoming our top five volume weeks ever,” as Middle East tensions lifted fuel prices and sent drivers to Costco’s discounted pumps. Cheap gas pulls in members who then shop inside, but the trade-off is margin: gas is low-margin, so the reported gross margin rate slipped, which is part of what spooked the market even though the core business stayed healthy.

See historical and forward estimates for Costco stock (It’s free!) >>>

What The Valuation Demands

At $951.45, Costco trades at an NTM P/E of 43.49x against a Street target of $1,082.94, roughly 14% above the current price. Sentiment is constructive but split: 19 Buys, 3 Outperforms, 13 Holds, 1 Underperform, and 1 Sell.

The friction is the starting multiple. A near-48x trailing P/E for a business with single-digit revenue growth leaves no room for error, which is why the stock corrects on small misses. Bulls call it a certainty premium that the membership model has earned. Bears note that any compression from here erases years of earnings growth, no matter how well the company executes. The special dividend sits in the middle: it is one of the few near-term levers that can return cash to shareholders while the multiple argument plays out.

See how Costco performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $951.45

- Target Price (Mid): ~$1,370

- Potential Total Return: ~44%

- Annualized IRR: ~9% / year

See analysts’ growth forecasts and price targets for Costco stock (It’s free!) >>>

The two revenue CAGR drivers are continued warehouse expansion, with management targeting more than 30 net new openings a year, and steady mid-single-digit same-store sales growth. The margin driver is a gradual lift in net income margin toward around 3%, as membership fee income grows faster than merchandise sales. The primary risk is multiple compression: the model assumes the P/E drifts modestly lower, so the return depends almost entirely on earnings growth, not sentiment.

The upside case points to around 147% total return if international and digital growth stay strong.

The downside case still shows around 55% total return, but at a slower, roughly 6% annual pace.

Conclusion

The catalyst to watch is the fiscal Q4 2026 earnings report, expected in late September. The January 2024 special dividend was announced alongside a quarterly report, so the September call is the most likely window for the next one. An announcement near the $24-per-share level would confirm management sees the stock as fully valued and prefers returning cash over buybacks. No announcement, paired with another sub-1% EPS miss, would tell you the multiple has to do the work alone. Watch the renewal rate too: holding above 92% in the U.S. and Canada keeps the earnings-quality story intact, while a slip below 90% worldwide would hand the bears their best argument.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Costco?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Costco, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Costco alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!