Key Takeaways:

- Exceptional Growth: L3Harris delivered 15% organic revenue growth in Q1 2026, one of the strongest quarters in the company’s history.

- Price Projection: Based on current execution, LHX stock could reach $343 by December 2028.

- Potential Gains: That target points to a 16% total return from the current price of $294.82.

- Annual Return: Investors could see roughly 6% annual growth over the next 2.5 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

L33Harris Technologies (LHX) opened 2026 with one of its best quarters yet. Revenue grew to $5.7 billion, up 15% organically. GAAP EPS rose 33% year-over-year to $2.72. Segment operating margins expanded for the tenth consecutive quarter.

- Backlog reached over $40 billion, not yet including $25 billion in pending Munitions Acceleration Council orders.

- International book-to-bill ratio hit 2.2 in the quarter, with NATO allies driving strong demand for radio and ISR.

- Space & Mission Systems revenue grew 24%, led by classified programs and missionized aircraft.

- Missile Solutions revenue rose 18%, with margins expanding 110 basis points.

- Full-year guidance was reaffirmed: revenue of $23 to $23.5 billion, free cash flow of $3 billion, and GAAP EPS raised by $0.10 to $11.40 to $11.60.

LHX trades around $295. For investors seeking defense exposure with above-average growth and a visible backlog, this stock offers a straightforward case.

See analysts’ full growth forecasts and estimates for LHX stock (It’s free) >>>

What the Model Says for L3Harris Stock

We looked at L3Harris through the lens of its Trusted Disruptor strategy, which positions it between traditional defense primes and newer defense tech companies. The idea is to deliver at prime-contractor scale while moving with the agility of a smaller, more focused business.

That positioning is paying off. Revenue has grown organically in 9 of the last 10 quarters. Revenue per employee has risen nearly 25% over the past two years. The company is simultaneously winning large classified programs, securing NATO radio contracts, and building solid rocket motor capacity for the munitions ramp.

The MAC opportunity is particularly notable. The $25 billion in pending orders from the Munitions Acceleration Council, which are not yet in backlog, could push total backlog toward $60 to $70 billion within the next 12 months.

The company is a key supplier of solid rocket motors to Lockheed and Raytheon across programs, including PAC-3 and THAAD. Management received a $1 billion investment from the Department of War to accelerate that capacity buildout.

Using 7.7% annual revenue growth and 16.1% operating margins, our model projects the stock reaching $343 within 2.5 years. This assumes a 20.1x price-to-earnings multiple, down from the current forward P/E of 24.4x.

The compression reflects normalization after a recent re-rating, while still acknowledging a business with improving growth visibility.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for LHX stock:

1. Revenue Growth: 7.7%

Full-year 2026 guidance calls for 7% organic growth, which management described as conservative given the Q1 outperformance.

The ISR pipeline alone stands at roughly $40 billion internationally, with allies roughly 20% through their 10-year communications modernization cycles.

The Army HMS radio program was funded at $515 million in fiscal 2027, with similar amounts planned for the following five years.

2. Operating margins: 16.1%

EBIT margins were 15.8% over the trailing year, consistent with the 15.3% three-year average and 16.1% five-year average.

Full-year segment margin guidance is the low 16% range.

The company has been expanding margins each quarter even while increasing R&D investment by 44% year-over-year.

3. Exit P/E Multiple: 20.1x

LHX trades near 24.4x forward earnings today, above its three-year average of 20.1x.

We assume compression back toward that level. The stock has historically traded at 18–20x on a longer-term basis, and elevated near-term multiples often normalize as growth expectations get priced in.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

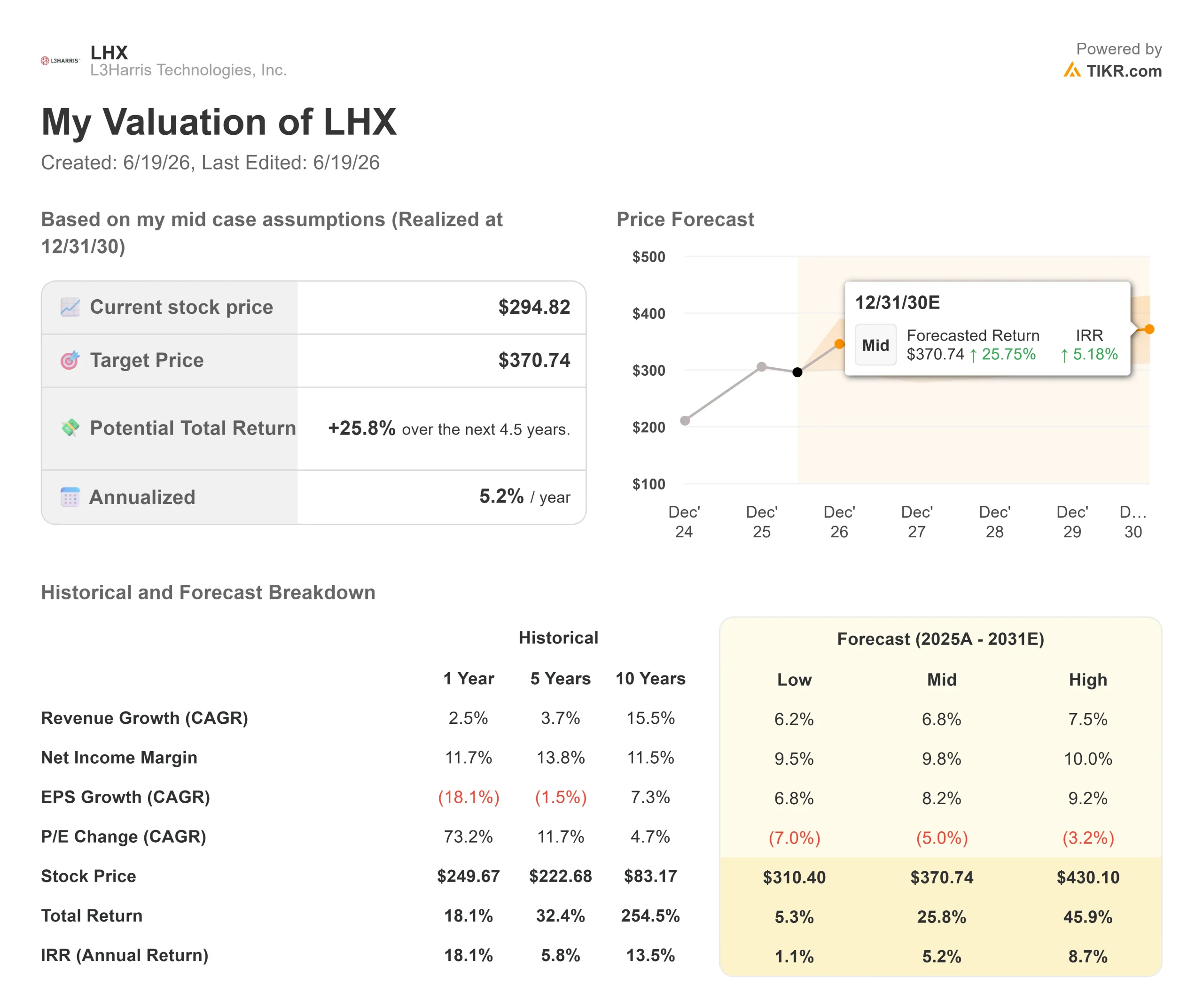

Defense electronics companies face program risk, budget timing, and execution complexity. Here’s how L3Harris stock might perform under different scenarios through December 2030:

- Low Case: If revenue grows 6.2% a year and net margins settle near 9.5%, investors see a 5.3% total return (1.1% annually).

- Mid Case: With 6.8% growth and 9.8% margins, the model points to a 25.8% total return (5.2% annually).

- High Case: If MAC contracts land, classified wins accelerate, and margins reach 10%, returns could hit 45.9% total (8.7% annually).

See what analysts think about LHX stock right now (Free with TIKR) >>>

The range is tighter than most growth stocks because L3Harris is already a mature, well-run business.

In the low case, budget negotiations delay contract definitization, the MAC orders take longer to flow through, and multiple compression weighs on returns.

In the high case, the $25 billion MAC backlog converts on schedule, the HBTSS follow-on is won mid-year, and international radio and ISR demand drives growth well above guidance.

How Much Upside Does L3Harris Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying, so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!