Key Takeaways for Copart Stock as of June 2026

- Analysts rate Copart stock 3 Buys, 3 Outperforms, 5 Holds, 1 Underperform with a street mean target of $41, implying around 36% upside from the current price of $30.

- TIKR’s mid-case model values Copart at around $46 by July 2030, implying around 51% total return from current levels, or roughly 11% annualized.

- Copart stock is undervalued at current levels, with EBIT of $464.3 million in Q3 and a 37.5% EBIT margin demonstrating that pricing power and operating leverage remain structurally intact despite a 4.2% decline in U.S. insurance unit volumes.

- Global average selling prices rose 4.6% in Q3, and U.S. insurance ASPs reached a seasonally adjusted all-time record high, revealing that the market is penalizing volume cyclicality while missing the durable pricing engine underneath.

Copart Reports Record Auction Prices in Q3 Despite a 4% U.S. Volume Decline

Copart (CPRT), the world’s largest online salvage vehicle auctioneer, reported fiscal Q3 2026 revenue of $1,237.1 million on May 21, beating the Street’s $1,195.0 million estimate by 3.5%, even as U.S. insurance unit volumes declined 4.2% year-over-year.

The company operates an online auction marketplace that connects vehicle sellers, principally auto insurers, with buyers across more than 160 countries, generating revenue through service fees rather than primarily owning the inventory.

Global average selling prices rose 4.6% in the quarter, more than offsetting a 2.4% decline in total unit volumes to produce positive revenue growth.

U.S. insurance average selling prices increased 4.1%, reaching what CEO Jeff Liaw described on the Q3 earnings call as a seasonally adjusted record: “Today, for U.S. insurance sellers at Copart, the mix of pure sale units is at all-time highs.”

The volume softness reflected consumers pulling back on auto insurance coverage in response to rising premiums and a shift in policy in-force mix among insurance carriers.

Total loss frequency, the structural metric that drives Copart’s supply pipeline, reached 23.6% in the first calendar quarter of 2026, up nearly 5 full percentage points over four years.

Internationally, total units sold grew 5.9%, international service revenues rose 17.9%, and operating income for the international segment reached $73.8 million at a 31.5% margin, with the U.K., Germany, and Canada all contributing to the momentum.

Free cash flow grew 12% year-to-date, and Copart ended the quarter with $4.2 billion in cash, equivalents, and held-to-maturity securities and no debt.

The company repurchased over 43.4 million shares for more than $1.6 billion in the fiscal year to date, a deployment pace that signals management’s conviction in the long-term value of the business.

CPRT Stock Holds 6 Buy-Side Ratings as Street Targets Price Well Above Cyclical Lows

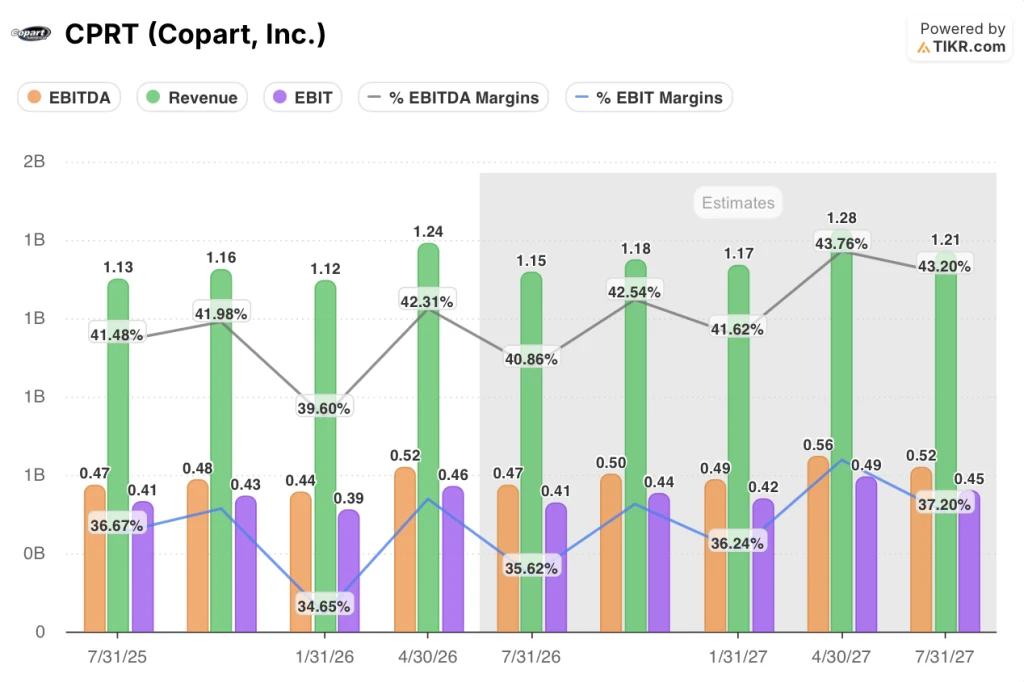

Wall Street expects Copart stock to deliver around 2% EBIT growth in Q4 FY26, with consensus seeing the business sustaining EBIT margins near 36% despite ongoing volume headwinds.

Six of the 12 analysts covering CPRT carry positive ratings (3 Buys, 3 Outperforms), reflecting conviction that the structural ASP growth engine and international momentum outweigh the near-term U.S. volume softness.

Q3 EBIT of $464.3 million came in 4.2% above the $445.6 million consensus estimate and grew 2.8% from $451.6 million in the same quarter a year prior, even as unit volumes declined.

EBITDA reached $523.4 million in Q3, up 3.4% year-over-year and 3.5% ahead of the $505.6 million Street estimate, with EBITDA margins at 42.3%.

Street consensus for Q4 FY26 points to revenue of around $1.15 billion, roughly flat year-over-year, and EBIT of around $0.41 billion, reflecting continued caution about the U.S. claims frequency environment.

For FY27, consensus estimates project revenue growth of around 4% to 6% annually and EBIT expanding toward $0.42 billion to $0.49 billion per quarter, as total loss frequency trends and international scale absorb the cyclical volume drag.

With EBIT margins demonstrating resilience at 37.5% in Q3 against a backdrop of falling unit volumes, Copart stock is undervalued at current levels relative to a business that has generated structural pricing power improvements across multiple economic cycles.

The question the Street has not yet answered is whether U.S. assignment volumes, which declined at a low single-digit pace in Q3, will begin recovering in the back half of calendar 2026 as the consumer insurance retrenchment proves cyclical rather than secular, as Copart’s management believes.

Is Copart Stock Undervalued in 2026? TIKR’s $46 Model Says Yes

TIKR’s mid-case values Copart at approximately $46 by July 2030, implying around 51% total return from the current price of $30, or roughly 11% annualized over approximately 4 years.

The TIKR target depends on the same dynamic Copart demonstrated in Q3: ASP growth absorbing volume cyclicality to sustain EBIT margins above 35%, a threshold the business has now maintained for multiple consecutive quarters.

International expansion, where units grew 5.9% in Q3 and assignment volumes rose at a low double-digit pace, represents the second leg of the target’s credibility, as higher-margin international service revenue mixes up over time.

The condition the TIKR model requires is not a recovery in U.S. insurance unit volumes but rather that total loss frequency continues its long-run upward trend, a trajectory management noted reached 23.6% through Q1 calendar 2026 and which rising repair costs, EV complexity, and ADAS technology all support going forward.

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Copart, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Copart, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CPRT stock on TIKR for Free →

What is total loss frequency and why does it matter for Copart?

Total loss frequency measures the share of vehicle insurance claims where the car is declared a total loss rather than repaired, and it reached 23.6% in Q1 calendar 2026, up nearly 5 percentage points over four years.

A higher rate means more vehicles flow to Copart’s auction platform, expanding supply even when accident rates soften. Rising repair costs, ADAS system complexity, and EV battery replacement economics all structurally push this rate higher over time.

Can Copart sustain EBIT margins above 35% if U.S. volumes keep declining?

Copart demonstrated in Q3 FY26 that EBIT margins can expand even with U.S. unit volumes down 4.2%, as the combination of 4.6% higher average selling prices and 5.6% lower vehicle sale costs produced a 37.5% EBIT margin, up 27 basis points year-over-year.

Sustaining that level depends on whether international revenue growth, now running at 14.1%, continues mixing up and whether ASP growth persists.

The $1.6 billion in share repurchases year-to-date signals management’s confidence in that trajectory.