Key Takeaways for Nucor Stock as of June 2026

- Analysts rate Nucor stock 10 Buys, 3 Outperforms, 3 Holds, and 1 Sell, with a street mean target of $258, implying around 6% upside from the current price of $244.

- TIKR’s mid-case model values Nucor at around $256 by December 2030, implying around 5% total return from current levels, or roughly 1% annualized.

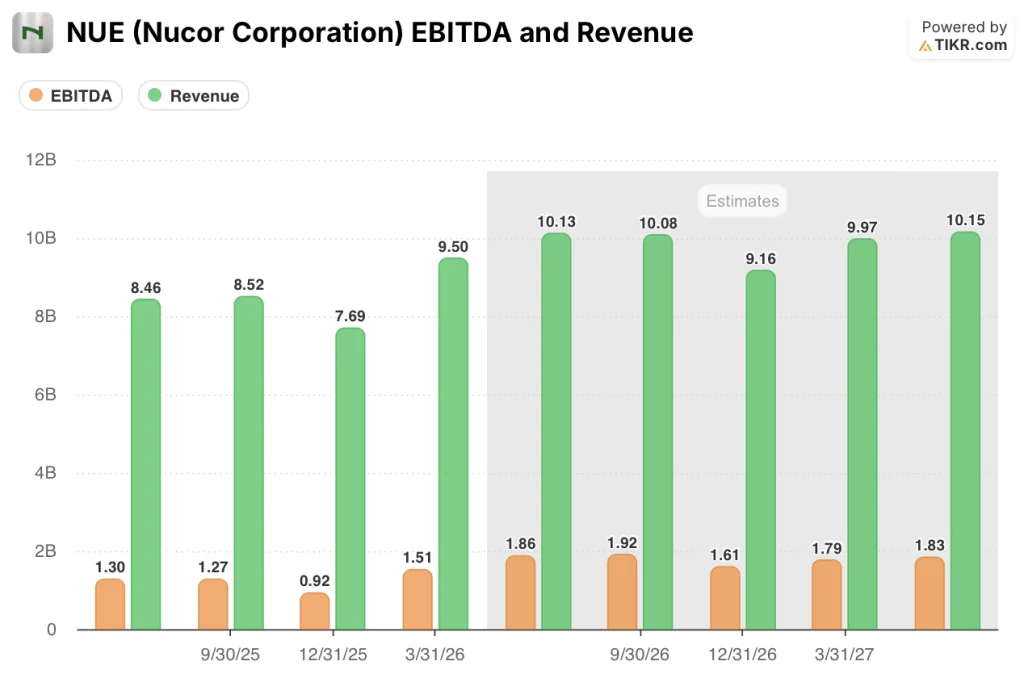

- Nucor stock is fairly valued at current levels, with EBITDA of $1.51 billion in Q1 2026 already priced into a stock that has nearly doubled from its 52-week low.

- Nucor set a record 7 million tons in quarterly steel mill shipments during Q1 2026, with the backlog rising 20% from year-end to 4.7 million tons, the highest level since Q2 2021.

Nucor stock has nearly doubled in twelve months, and the conviction-to-upside gap is tightening. TIKR’s professional-grade tools let you stress-test the math. Explore NUE’s valuation on TIKR for free →

Nucor Stock Sets an All-Time Shipment Record in Q1 2026 While Imports Hit a Multi-Year Low

Nucor Corporation (NUE) stock delivered its strongest quarterly shipment volume in company history during Q1 2026, with the results arriving against a backdrop of tightening import competition and an accelerating capital return program.

The company produces steel in electric arc furnaces (melting scrap metal rather than processing iron ore) across 26 mills nationwide, which gives it a structurally lower cost profile than traditional blast furnace operators.

Revenue reached $9.50 billion in Q1 2026, up 21.3% from the same quarter a year earlier and beating the street estimate of $8.86 billion by more than 7%.

The number that makes the quarter undeniable is 7 million tons.

That figure represents the highest quarterly shipment volume Nucor has ever recorded across its steel mills, achieved with weather-related disruptions early in the period and still clearing the bar.

CEO Leon Topalian captured the tone of the quarter on the Q1 2026 earnings call: “I’ve been in this business a long time. I’ve been in our longs product businesses or sheet group. And from a longs perspective, our customers that I’m talking to today are busier than anything they’ve ever seen in their history.”

Behind the shipment record sits a structural shift in the competitive environment: U.S. finished steel import share fell from over 22% in Q1 2025 to approximately 15% in Q1 2026, as Section 232 tariffs and associated trade remedy orders squeezed foreign supply out of the domestic market.

At 4.7 million tons at the end of Q1 2026, the steel mills backlog climbed 20% from year-end and reached its highest point since Q2 2021, confirming the volume outlook is not a one-quarter event.

Steel products backlog also grew 9% from year-end, with gains across all major product groups.

Nucor’s EBITDA for the quarter came in at $1.51 billion, up 117.5% year over year, beating the consensus estimate of $1.33 billion by nearly 14%.

EPS of $3.23 exceeded the $2.82 street estimate by 14.7% and marked a 319% increase from the $0.77 recorded in the same quarter a year earlier.

Free cash flow turned meaningfully positive at $225 million, reversing the negative $495 million in Q1 2025.

The steel mills segment drove the headline numbers, with pretax earnings of $1.13 billion, more than double the prior quarter, as volumes and average selling prices rose across all four product groups.

Looking ahead, the West Virginia sheet mill project is now 85% through construction, with commissioning underway sequentially through 2026 and commercial shipments targeted to begin ramping in early 2027.

Nucor stock’s backlog data and segment-level performance are live on TIKR. Track the metrics that matter before Q2 results hit. Analyze NUE on TIKR for free →

Wall Street Rates NUE 10 Buys But the $258 Mean Target Signals the Upside Is Getting Thin

Of the 17 analysts covering Nucor stock, 10 rate it a Buy, 3 an Outperform, 3 a Hold, and 1 a Sell, with a street mean target of $258 and a street high target of $290.

The mean target implies around 6% upside from the current price of $244, a modest gap for a name with this degree of buy-side conviction.

Analysts currently project Nucor stock’s EBITDA to reach around $1.86 billion in Q2 2026, up around 44% year over year, as higher realized pricing in the sheet market continues to catch up with the spot price rally that began in the second half of 2025.

Analysts also expect that trajectory to continue through the back half of 2026, with Q3 2026 consensus EBITDA estimates sitting at around $1.92 billion, up around 52% year over year.

Revenue estimates follow the same trajectory, with Q2 2026 consensus sitting at around $10.13 billion, a rise of around 20% year over year, reflecting both volume growth and pricing tailwinds in sheet and structural steel.

At roughly $244 per share, against a 52-week range that bottomed near $123 in mid-2025, the stock has re-rated sharply on the earnings recovery, and the 6% gap to the street mean reflects a market that has already priced in a substantial portion of the fundamental improvement.

Is Nucor Stock Fairly Valued in 2026? TIKR’s $256 Mid-Case Says the Run Is Almost Priced In

TIKR’s mid-case values Nucor at approximately $256 by December 2030, implying around 5% total return from the current price of $244, or roughly 1% annualized over 4.5 years.

The durability of the EBITDA recovery underpins that target, and the Q1 2026 results establish the baseline credibly: EBITDA of $1.51 billion beat estimates by 14% and represented a 118% year-over-year improvement, demonstrating that the earnings power of the modernized fleet is not speculative.

What the TIKR model requires to be credible is the continuation of two dynamics already named: import penetration holding near 15% rather than rebounding toward the 22%-plus levels of early 2025, and the Q1-to-Q2 EBITDA step-up materializing as the forward estimates imply.

Nucor stock’s free cash flow turning positive in Q1 2026 at $225 million, after running deeply negative through most of the heavy-CapEx build cycle, confirms the company is entering the harvest phase of its $20 billion capital program, a transition that supports both the valuation and the case for continued capital returns to shareholders.

TIKR’s mid-case targets $256 for NUE by December 2030. See exactly how the model gets there and build your own assumptions. Explore NUE on TIKR for free →

Should You Invest in Nucor Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Nucor Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Nucor Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NUE stock on TIKR for Free →

What is the biggest risk to Nucor stock’s earnings outlook?

The primary risk is a reversal of the import compression story. Steel import share fell from over 22% in Q1 2025 to approximately 15% in Q1 2026, a structural improvement driven by Section 232 tariff enforcement.

If trade policy enforcement loosens, imports return, or USMCA negotiations reduce the tariff coverage that closed the derivative steel loophole, domestic pricing could soften faster than the backlog implies.

A simultaneous spike in scrap costs would compress the metal spreads that drove the 118% EBITDA improvement in Q1 2026.

When does the Nucor West Virginia mill start generating revenue?

Nucor targets commercial shipments from the West Virginia sheet mill to begin ramping in early 2027, with construction at approximately 85% completion as of Q1 2026.

Commissioning of the pickle line, cold mill, and automotive-grade galvanizing line will sequence through the remainder of 2026.

Management guided for the mill to reach approximately 50% of capacity utilization by the end of 2027, with continued penetration of automotive and consumer durable markets in the Midwest and Northeast, two regions where Nucor is currently underweighted in flat-rolled steel.