Key Takeaways for Okta Stock as of June 2026

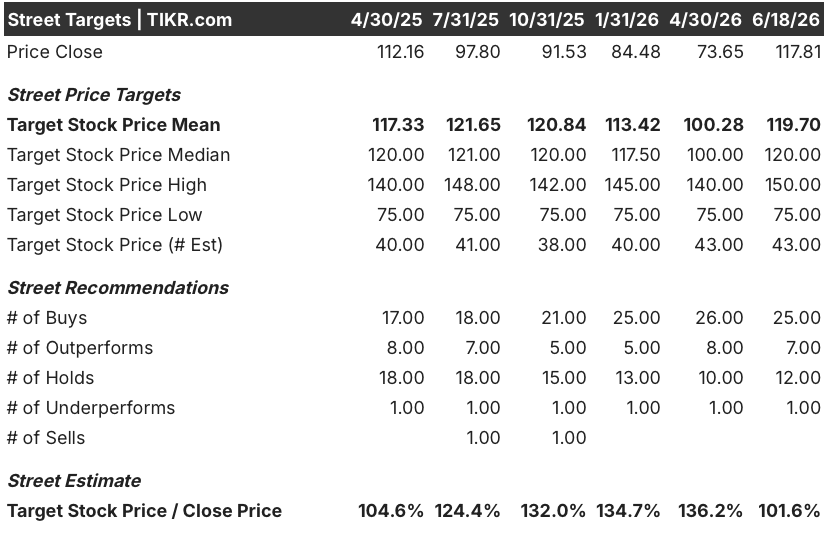

- Analysts rate Okta stock 25 Buys, 7 Outperforms, 12 Holds, 1 Underperform, and 1 Sell, with a Street mean target of $120, implying around 2% upside from the current price of $118.

- TIKR’s mid-case model values Okta at $151 by January 2031, implying 28% total return from current levels, or 6% annualized.

- Okta stock surged 21% on May 29, 2026 after Q1 fiscal 2027 revenue of $765 million beat consensus estimates by nearly $14 million and management raised full-year revenue guidance to 9%–10% growth.

Okta Stock Jumped 21% After Q1 Earnings Release as AI Agent Pipeline Hits a Record

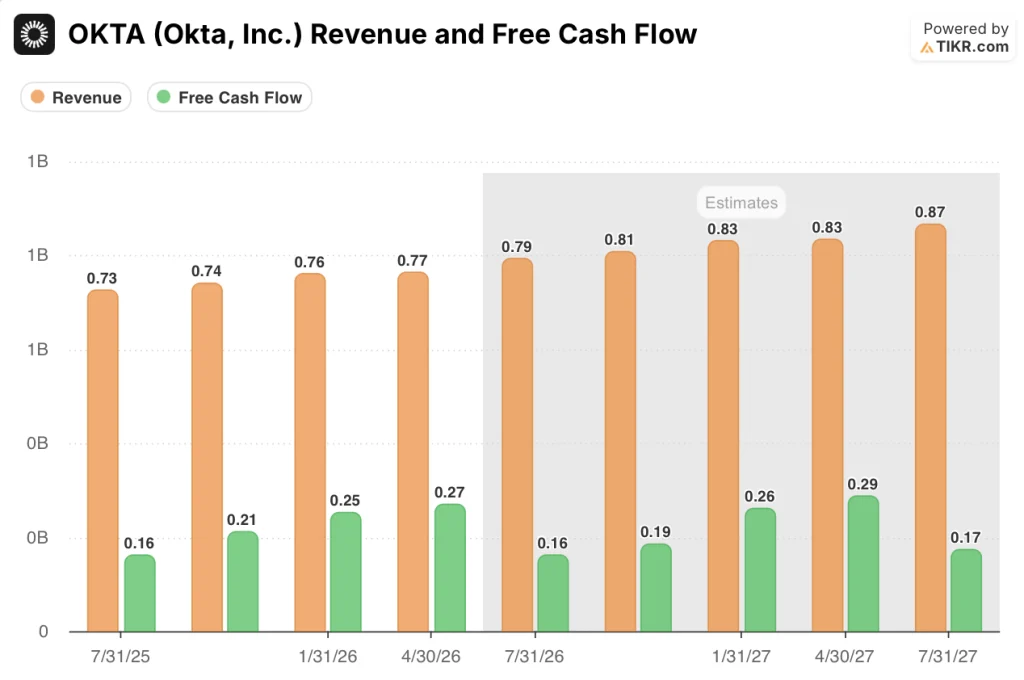

Okta, Inc. (OKTA) surged 21% on May 29, 2026 after reporting Q1 fiscal 2027 revenue of $765 million, up 11% year over year and $13 million above the consensus estimate of $752 million.

Subscription revenue reached $750 million, also up 11% year over year, reinforcing the durability of Okta stock’s recurring revenue base even as the broader software sector traded under pressure.

Free cash flow came in at $271 million, representing a 13.87% increase year over year and outpacing the Street’s $255 million estimate by around 6%.

CEO Todd McKinnon framed the quarter’s momentum in the context of a structural identity shift, saying on the Q1 fiscal 2027 earnings call: “AI agents are rapidly becoming a new workforce inside every organization, creating a wave of identities that must be secured and governed alongside human users.”

New products, particularly Okta Identity Governance, represented 25% of Q1 bookings, a meaningful step up from the year-ago period, and deals that included those new products carried a 40% average contract value uplift over standalone access management deals.

The company ended the quarter with approximately $2.6 billion in cash and repurchased just over 3 million shares at a total cost of $241 million, with $680 million remaining under the $1 billion buyback program.

CFO Brett Tighe also confirmed the repurchase posture directly on the Q1 call: “We look to take advantage of what we believe to be an undervalued share price.”

Management guided Q2 fiscal 2027 revenue to $790 million to $794 million, up 9% year over year, and affirmed full-year revenue growth of 9% to 10% alongside a non-GAAP operating margin of 25% to 26%.

Okta also disclosed that it will settle the $350 million principal of its convertible notes in cash next month, a capital deployment decision that reflects confidence in the balance sheet while absorbing incremental near-term cash outflow.

Current remaining performance obligations grew 12% year over year and net revenue retention rose to 107%, two forward indicators that confirm the subscription base continues to expand beyond simple renewals.

The stock had entered the quarter trading near its 52-week low after a software sector selloff tied to AI disruption fears, making the earnings-driven rebound one of the sharpest single-day moves in Okta stock’s recent history.

Okta Stock Sits at $120 Mean Target While Agentic AI Deals Signal a Re-Rating Ahead

Wall Street rates Okta stock a Buy at a mean price target of $120, with 25 analysts holding outright Buy ratings and 7 holding Outperform calls against only 12 Holds and 2 downside ratings across the 45-analyst coverage universe.

Okta stock’s Q1 revenue of $765 million grew 11% year over year, matching the rate from the prior quarter and landing above the $752 million estimate, while the Q2 guidance midpoint of $792 million implies 9% growth and sets a low bar that management has now demonstrated the ability to exceed.

Analysts following the agentic AI narrative point to deal-size data as the most concrete early signal, with early Okta for AI Agents transactions running approximately 40% larger than the company’s average deal, a spread that management confirmed on the Q1 call.

Current RPO growth of 12% year over year and net revenue retention at 107% confirm that existing customers continue to expand their Okta footprint, a trend the IGA product line drove even before the AI agent products reached general availability on April 30.

Free cash flow of $271 million in Q1 alone, up 14% year over year, gives the company the balance sheet flexibility to sustain the $680 million remaining under its buyback authorization while continuing to invest in the agentic product roadmap.

The Street’s open question centers on whether the AI agent pipeline, which CEO Todd McKinnon called the largest the company has ever generated for a new product, converts into material bookings before fiscal year end or remains a fiscal 2028 contributor.

Okta Stock Grows Revenue at Half the Rate of CrowdStrike and Palo Alto — and the Gap Is the Entire Thesis

Okta stock’s revenue grew 11% year over year in Q1 fiscal 2027, a rate that sits well below CrowdStrike’s 23% and Palo Alto Networks’ (PANW) 31% over the same period, placing Okta at the bottom of the cybersecurity identity peer set on the metric that drives valuation multiples most directly.

CrowdStrike’s (CRWD) revenue growth has held in the 21%–25% range across the past several quarters and consensus estimates project it staying near 22% through fiscal 2028, a durability premium the market prices into the stock’s multiple at a level Okta has not yet earned.

Palo Alto Networks posted 31% revenue growth in its most recent quarter but consensus projects a sharp deceleration toward 12%–15% by fiscal 2028, compressing the gap with Okta’s forward growth trajectory and raising the question of whether Okta stock’s discount is warranted given that its own growth rate is expected to stabilize while PANW’s decelerates toward it.

TIKR’s $151 Target on Okta Stock Is Undervalued at $118 if the AI Agent Inflection Lands

TIKR’s mid-case values Okta at $151 by January 2031, implying 28% total return from the current price of $118, or 6% annualized.

The revenue trajectory established in Q1, with 11% growth, a 12% cRPO advance, and new product bookings representing 25% of the mix, is exactly the setup that supports TIKR’s assumption of a gradual re-acceleration as the AI agent layer monetizes through fiscal 2028 and beyond.

Okta stock’s undervalued position relative to TIKR’s $151 target depends on the identity platform expanding its customer wallet share at a rate faster than the Street’s current 9%–10% growth consensus — a condition that the 40% ACV uplift on AI agent deals already supports in early data.

Should You Invest in Okta, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Okta, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Okta, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze OKTA stock on TIKR for Free →

How significant is Okta’s agentic AI opportunity relative to current revenue?

The pipeline for Okta for AI Agents is the largest ever seen for a new product, but management flagged it as not yet material in Q1, positioning it as a fiscal 2028 revenue driver beyond the 9%–10% full-year guidance.

Why is Okta buying back stock while the share price is near recent highs?

Okta deployed $241 million in Q1 buybacks with $680 million remaining under a $1 billion authorization, and CFO Brett Tighe stated on the earnings call that management views the current share price as undervalued.