Key Stats for VRT Stock

- 52-Week Range: $110.06 – $379.94

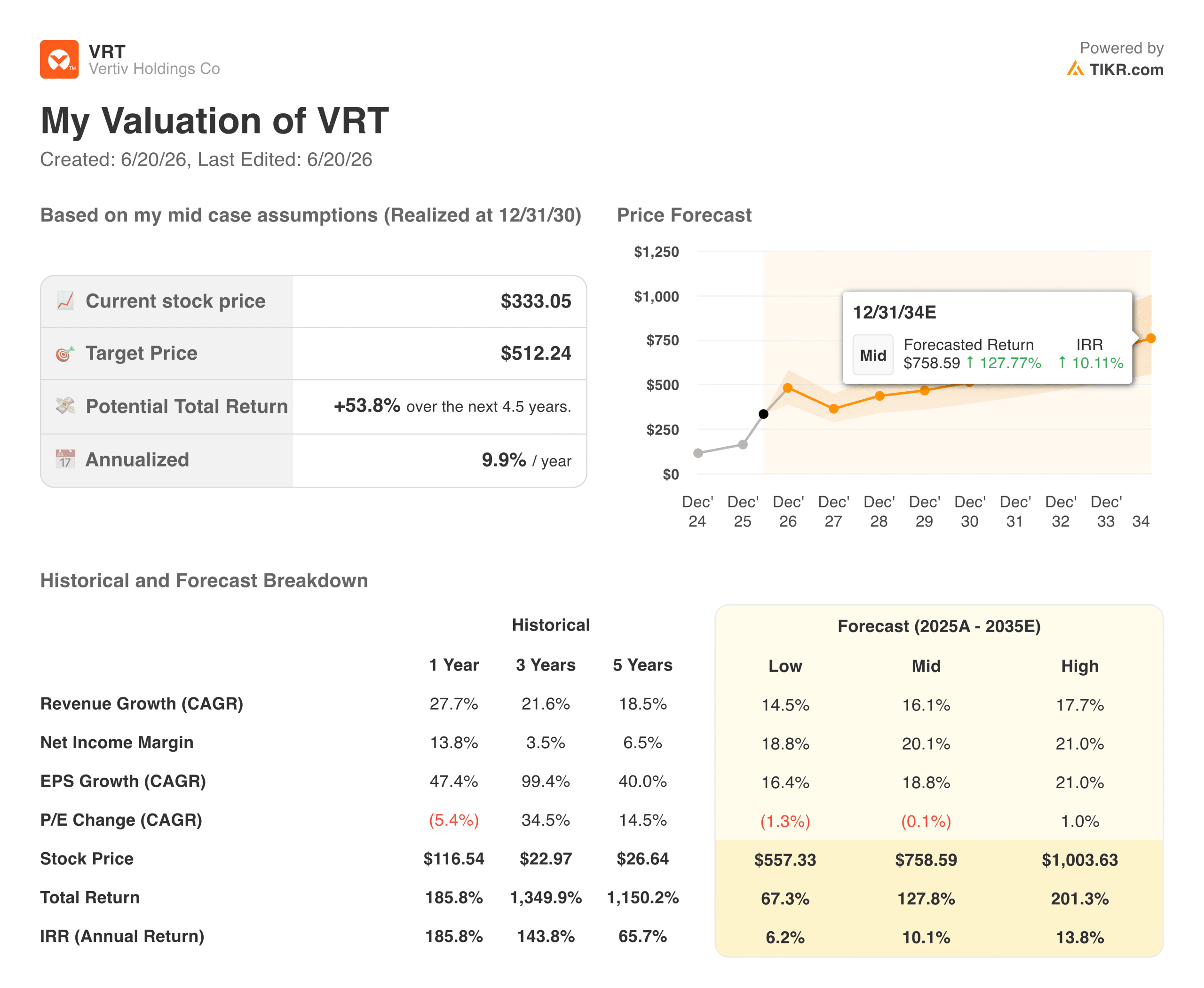

- Current Price: $333.05

- Street Mean Target: ~$378

- TIKR Model Target: ~$512 at ~10% annualized IRR

- Q1 2026 Revenue: $2.65B (+30% YoY)

- Q1 2026 Adjusted Operating Margin: 20.8%

- Q1 2026 Adjusted Diluted EPS: $1.17 (+83% YoY)

- Full-Year 2026 Adjusted EPS Guidance: $6.30 – $6.40

Analyze your favorite stocks like Vertiv Holdings Co with TIKR (It’s free) >>>

A 25% Drop That the Business Did Not Earn

Vertiv (VRT) spent much of June in a sharp pullback that had little connection to what was actually happening inside the company. The stock hit a 25% drawdown on June 10, unwinding a significant portion of the gains that followed a strong Q1 earnings report in late April.

The selloff was macro-driven, tied to broader AI infrastructure sentiment and sector rotation rather than any company-specific deterioration.

The underlying business in that same window was running at 30% revenue growth, 83% adjusted EPS growth, and a $15 billion backlog with a book-to-bill ratio near 2.9x. Investors who understand the difference between price and business performance had a meaningful opportunity sitting in plain sight.

See analysts’ full growth forecasts and estimates for VRT stock (It’s free) >>>

How a Power and Cooling Business Became an AI Infrastructure Play

Vertiv makes the physical infrastructure that keeps data centers running: power systems, cooling units, racks, and the monitoring software that ties it all together. That description undersells what has happened to the business over the past three years.

As AI workloads have driven data center density to dramatically higher levels, the power and cooling requirements per rack have grown at a pace the industry was not designed to handle, and Vertiv has been one of the primary beneficiaries of that shift.

Revenue has grown from roughly $5 billion in 2021 to over $10 billion in 2025, while operating margins expanded from 4% to nearly 19% over the same period.

That margin trajectory is particularly important. Vertiv is not just growing revenue by adding volume. It is converting that volume into meaningfully higher operating profit as the business scales, pricing improves, and the product mix shifts toward higher-margin thermal management and services. The Americas region, which led Q1 with 44% organic growth, is the clearest expression of where hyperscaler AI capex is landing.

Estimate a company’s fair value instantly (Free with TIKR) >>>

The Backlog Tells the Forward Story

First-quarter results gave investors several reasons to look past the near-term noise. Net sales of $2.65 billion came in ahead of expectations, adjusted operating profit grew 64%, and management raised full-year revenue guidance to $13.5 to $14 billion, implying around 30% organic growth for the year.

The adjusted diluted EPS guidance of $6.30 to $6.40 represents roughly 51% growth at the midpoint versus 2025.

The backlog number is where the forward visibility becomes tangible. A $15 billion backlog and a book-to-bill ratio near 2.9x mean Vertiv has nearly $3 in new orders for every $1 it ships. That kind of coverage gives management confidence in the guidance and provides investors with a reasonable degree of protection against near-term softness in demand.

See analysts’ growth forecasts and price targets for Vertiv stock (It’s free!) >>>

What the Valuation Model Says

TIKR’s model targets around $512 per share in the mid case, realized at the end of 2030, implying roughly 54% total return over about 4.5 years at around 10% annualized. The scenario range skews to the upside: the low case lands around $557 at roughly 6% annualized, while the high case approaches $1,004 at around 14% per year.

The mid-case return is driven almost entirely by earnings growth rather than multiple expansion, with the P/E modeled to compress slightly over the forecast period. That is the honest framing for a stock trading at nearly 49x forward earnings: the bull case is not multiple expansion, it is that earnings grow fast enough to grow into the current valuation and beyond.

The model assumes around 16% revenue growth, compounded through 2035, with net income margins expanding toward 20%, both of which are consistent with management’s own long-term targets.

The risks are a slowdown in hyperscaler AI capex, competitive pressure from cooling specialists like Eaton and Schneider Electric, or execution slippage in the capacity expansion Vertiv is running to meet current demand.

Build your own Valuation Model to value any stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!