Key Stats for Vertiv Holdings Stock

- 52-Week Range: $106 to $380

- Current Price: $316

- Street Mean Target: $377

- Street High Target: $500

- Analyst Consensus: 18 Buys / 4 Outperforms / 3 Holds

- TIKR Model Target (Dec. 2030): $419

Vertiv Stock Soars 200% but the May Investor Day Just Changed the Thesis

Vertiv Holdings Co (VRT), the global provider of power management and thermal management systems for data centers, delivered a quarter of operational inflection in April and then used its May investor conference in Greenville, South Carolina to extend that momentum into a formal multi-year framework, raising its 5-year revenue CAGR guidance to 20% to 22% and setting an adjusted operating margin ambition of 27% by 2030 from the 23.3% it currently guides for full-year 2026.

The Q1 2026 results that preceded the investor day were themselves a statement of execution velocity.

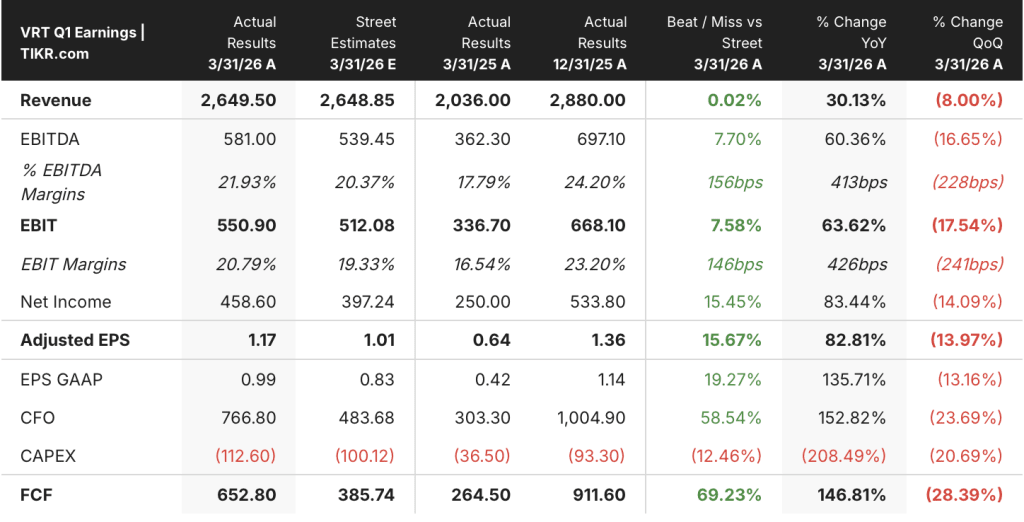

Net sales of $2.65 billion came in 30% above the year-ago period, with organic growth of 23% and Americas organic growth of 44% reflecting the concentrated intensity of hyperscaler and colocation deployment in that region.

Adjusted diluted EPS of $1.17 landed $0.19 above guidance, a 83% increase over Q1 2025 that management attributed to operating leverage, favorable price-cost dynamics, and the scale benefits of a business that produced $653 million in adjusted free cash flow in a single quarter, up 147% year-over-year.

“The urgency has increased,” said Executive Chairman Dave Cote on the Q1 2026 earnings call. “The scale of deployments is larger and the technical complexity is creating opportunities for companies that can solve system-level problems, which is exactly where we excel.”

The investor day then reframed what those system-level capabilities are actually worth, positioning Vertiv not as a component vendor but as the end-to-end infrastructure layer for AI factories from grid connection through chip-level thermal management.

CEO Giordano Albertazzi introduced a $75 billion total addressable market figure for Vertiv’s expanded portfolio, up from the $62 billion legacy served market, with the data center subset estimated at roughly $50 billion growing at 18% to 20% annually.

The pipeline is the signal the market is tracking most closely.

Vertiv disclosed at the investor day that total data center power capacity additions are expected to ramp from around 20 gigawatts annually today toward roughly 35 gigawatts by the end of the 5-year planning horizon, a trajectory Albertazzi described as driven by the persistent gap between demand for AI compute capacity and the physical infrastructure that enables it.

Six acquisitions in under twelve months, including the thermal specialist ThermoKey, structural fabricator BMarko Structures, and liquid-cooling engineering firm Strategic Thermal Labs, have expanded Vertiv’s addressable content per megawatt while vertically integrating capabilities that previously sat outside the company’s manufacturing footprint.

Vertiv Holdings also announced four new or expanded Americas facilities in March, with South Carolina capacity for infrastructure solutions targeting a roughly 7x regional increase when fully ramped, and committed around $50 million to expand its Ironton, Ohio facility specifically for liquid cooling and chilled water systems, targeting a roughly 45% capacity increase there by Q2 2027.

Full-year 2026 guidance was raised at Q1 to net sales of $13.5 billion to $14 billion at the midpoint of $13.75 billion, representing 34% growth over 2025, with adjusted EPS guided to a midpoint of $6.35, up 51% year-over-year.

The investor day then layered a longer arc on top of that near-term guide, projecting adjusted free cash flow conversion of 95% to 100% through 2030, a CapEx framework of 3% to 4% of revenue annually, and a targeted leverage range of 1x to 2x that leaves what CFO Craig Chamberlin described as roughly $24 billion of available deployment capital over the period after dividends and share repurchases.

Vertiv stock has responded accordingly, trading near $316 as of May 29 after spending much of the year building from its 52-week low near $106.

Twenty-Two Analysts Are Bullish on Vertiv Stock, and the EBITDA Slope Explains Why

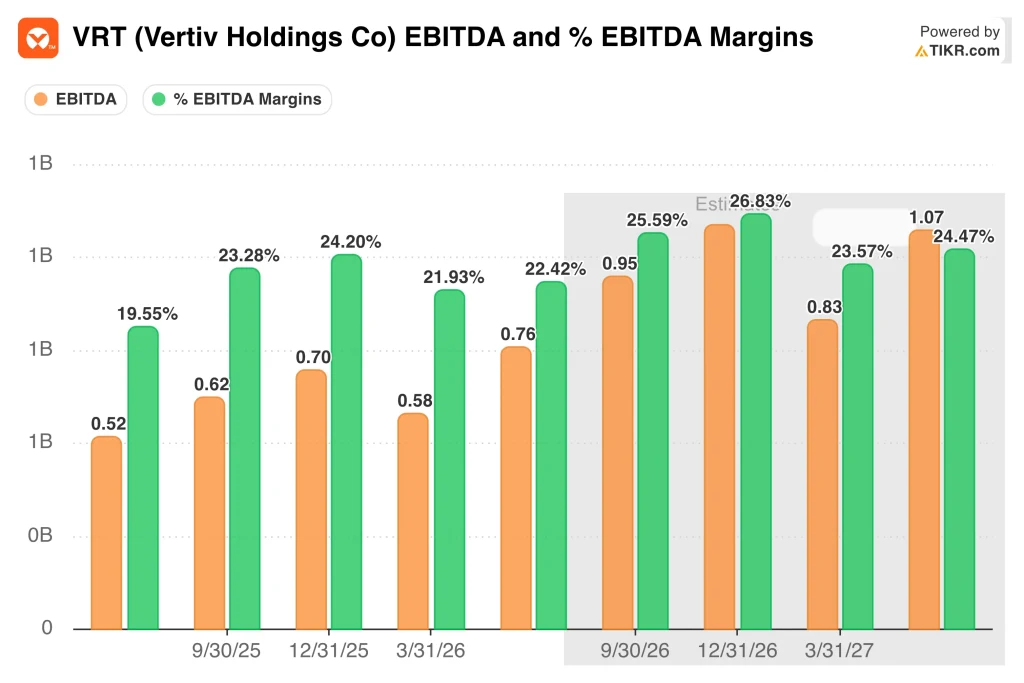

The investor day framework Vertiv laid out in May matters to analysts because it puts a quantitative roadmap behind what was previously a directional claim about operating leverage, with the street now underwriting EBITDA growth of roughly 47% year-over-year in Q2 2026 on the way to roughly 56% growth in Q4 2026.

Q1 2026 EBITDA came in at $0.58 billion, up 60.4% from the $0.37 billion posted in Q1 2025, and the margin line at 21.9% confirmed that Vertiv is converting accelerating revenue into operating profit at a rate the estimates table now extends through 2027.

The consensus sees full-year 2026 EBITDA building from that Q1 base through Q2 at around $760 million, Q3 at around $950 million, and Q4 at around $1.09 billion, a quarterly ramp that reflects the capacity additions Vertiv flagged as back-half weighted in both Americas and the recovering EMEA region.

Into 2027, the estimates carry the trajectory further, with Q1 2027 EBITDA seen at around $830 million and Q2 2027 at around $1.07 billion, growth rates of roughly 43% and roughly 42% year-over-year respectively, a deceleration in rate but an acceleration in absolute dollar terms.

The rating distribution as of May 29 shows 18 Buys, 4 Outperforms, 3 Holds, and 1 Underperform across 26 analysts, a skew that reflects broad conviction in the capacity buildout thesis with a small minority skeptical of execution at the pace management has guided.

The mean price target stands at $377, implying approximately 19% upside from the current price of $316, while the street high target of $500 reflects the bull case in which both the TAM expansion and the 27% margin ambition Vertiv set at its investor day materialize on schedule.

With the EBITDA line running at roughly 60% year-over-year growth on actuals and the consensus underwriting continued expansion through 2027 on the back of named capacity investments and recovering EMEA demand, Vertiv stock is undervalued relative to where this margin profile has historically been rewarded by the market.

The variable the street has not fully resolved is whether EMEA, which posted a 29% organic revenue decline in Q1 2026, can return to growth in the second half at the pace management embedded in the full-year guidance, because the entire 34% top-line growth target for 2026 depends on that regional recovery arriving on schedule.

Revenue Up 30% and Gross Profit Up 46%: What the Cost Build Is Actually Telling Investors

Vertiv generated $2.65 billion in revenue in Q1 2026, a 30% increase over the $2.04 billion posted in the comparable prior-year quarter, extending a top-line acceleration that has now run for five consecutive reporting periods.

Gross profit of $1.00 billion in Q1 2026 grew near 46% year-over-year from $0.69 billion, a rate of expansion that outpaced revenue growth by more than 15 percentage points and confirms that pricing power and volume leverage are compounding simultaneously at the top of the income statement.

Gross margin of around 38% in Q1 2026 represents a full recovery from the ~34% trough posted in Q1 2025, a 400 basis point improvement over four quarters that traces directly to the favorable price-cost execution management cited as the primary driver of Q1’s outperformance versus guidance.

SG&A of $0.46 billion in Q1 2026 expanded from $0.35 billion in Q1 2025, a ~31% increase that nearly matched the revenue growth rate, and total operating expenses of $0.57 billion rose from $0.39 billion in Q1 2025, absorbing the gross profit gains before they could fully flow through to the operating line.

Operating income of $0.43 billion in Q1 2026 grew around 47% year-over-year from $0.29 billion, a strong absolute increase, though the ~16% operating margin came in below the ~20% peak posted in Q4 2024, reflecting the deliberate cost investment in manufacturing capacity and services headcount that Vertiv has explicitly tied to second-half revenue acceleration.

Is Vertiv Stock Undervalued in 2026? TIKR’s $419 Target Holds If the Margin Roadmap Delivers

TIKR’s base case values Vertiv at approximately $419 by December 2030, implying around 33% total return from the current price of $316, or roughly 6% annualized over the next 4.6 years.

Should the 20% to 22% revenue CAGR Vertiv outlined at its May investor day hold through the 2030 planning horizon, supported by the capacity expansion program already underway across Americas and a recovering EMEA, the TIKR model points to a stock price of around $388 by December 2030, or roughly 2% annualized from current levels.

If the 27% adjusted operating margin ambition management set at the investor day materializes on schedule, driven by the operating leverage and productivity gains CFO Craig Chamberlin detailed, the mid-case trajectory implies a stock price of around $512 at December 2034, representing roughly 62% total return or approximately 6% annualized.

In the high case, where EPS compounds at roughly 16% annually and the P/E multiple modestly re-rates rather than compresses, the TIKR model implies a stock price of around $658 by December 2034, or approximately 9% annualized, a scenario that requires both the demand environment Vertiv described and continued share gains in the liquid cooling and converged infrastructure categories seeded throughout the buildout.

If EMEA fails to return to growth in the second half of 2026 as management has guided, or if hyperscaler spending visibility remains low and order volatility weighs on the margin trajectory, the downside case produces a stock price near $388 by December 2030, an annualized return of roughly 2% that prices Vertiv as a single-geography story rather than the global platform the investor day framed.

Is Vertiv stock a good buy in 2026?

Vertiv stock enters the second half of 2026 with a Q1 earnings beat of $0.19 above guidance, a full-year revenue guide of $13.75 billion at the midpoint representing 34% growth, and a May investor day that set a formal 5-year framework targeting 20% to 22% organic revenue CAGR and adjusted operating margins of 27% by 2030.

The investment case rests on whether the capacity investments now underway across Americas and a recovering EMEA translate into the back-half acceleration Vertiv has embedded in its guidance.

Twenty-two of 26 analysts currently rate the stock a Buy or Outperform, with a mean price target of $377 implying approximately 19% upside from the current price of $316.

Why is Vertiv stock up so much in 2026?

Vertiv stock has gained substantially in 2026 on the back of three overlapping developments: Q1 organic revenue growth of 23% with Americas up 44%, an EPS beat of $0.19 above guidance driven by operating leverage and favorable price-cost execution, and a May investor day at which management raised its 5-year revenue CAGR guidance and set a 27% adjusted operating margin ambition, prompting multiple analyst price target increases.

The S&P 500 inclusion effective March 23 added a structural demand component, and Hut 8’s $9.8 billion, 15-year data center lease in Texas, with Vertiv named as infrastructure partner, reinforced the scale of deployments the company is now embedded in.

Should You Invest in Vertiv Holdings Co?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Vertiv Holdings Co stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Vertiv Holdings Co alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze VRT stock on TIKR for Free →