Key Stats for Futu Holdings Stock

- Current Price: ~$104 (May 29, 2026)

- Q1 2026 Total Revenue: HKD 5.9B, +25% YoY

- Q1 2026 Net New Funded Accounts: 225,000; total funding accounts 3.59M, +34% YoY

- Q1 2026 Total Trading Volume: HKD 4.15T, +29% YoY (record)

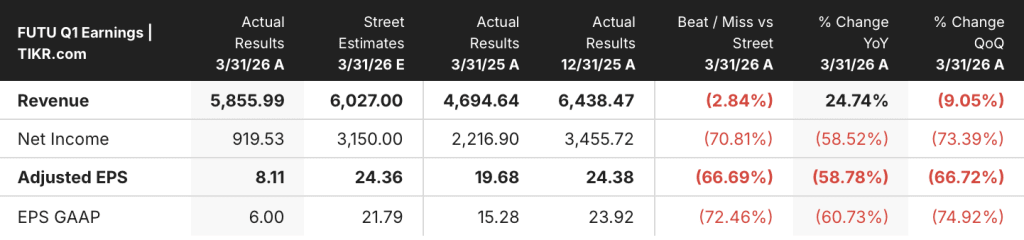

- Q1 2026 Adjusted EPS: HKD 8.11, -59% YoY (impacted by RMB 1.85B regulatory penalty)

- TIKR Model Price Target: ~$150

- Implied Upside: ~43%

Futu Holdings Stock Navigates Record Trading Volume and a Regulatory Penalty in Q1

Futu Holdings (FUTU) delivered record total trading volume of HKD 4.15 trillion in Q1 2026, up 29% year-over-year, even as a one-time RMB 1.85 billion regulatory penalty from China’s CSRC collapsed reported net income by 61% year-over-year.

The underlying operating picture was sharply different from the headline: prior to the CSRC administrative penalty, net income would have risen 36% year-over-year to HKD 2.9 billion, with a net income margin of 49.9%.

Client assets grew 47% year-over-year, and the company added 225,000 net new funded accounts in the quarter, bringing the total to 3.59 million funded accounts, up 34% year-over-year and 7% sequentially.

Arthur Chen, CFO, stated on the Q1 2026 earnings call that “prior to giving effect to this adjustment, our net income would have increased by 36% year-over-year and down 13% Q-over-Q to HKD 2.9 billion, with net income margin at 49.9%,” framing the penalty as a non-recurring event that does not alter the company’s operational trajectory.

Mainland Chinese funded accounts represented approximately 13% of total funded accounts at quarter end, with related client assets at roughly 17% of total and approximately 20% of total revenue; updated CSRC and SFC regulatory guidance issued in late May restricts deposit and buying activity for clients physically located in Mainland China but does not require account closure and carries no impact on the company’s full-year guidance of 800,000 net new funded accounts.

Beyond the penalty, two strategic developments extended the long-term growth surface: PantherTrade, the group’s crypto exchange, received full operational approval under the Hong Kong SFC VATP second-phase license in March, and Moomoo received NFA approval to operate a prediction market brokerage business in the United States, with event contracts including sports products expected to launch imminently.

Malaysia led all markets in client addition for the second consecutive quarter, profitability in the market continued to improve, and management expects Malaysia to reach breakeven within six to twelve months, while client assets in Singapore have compounded at a CAGR of over 50% over the past three years.

FUTU Stock Draws Overwhelming Buy Conviction as Analysts Look Through the Penalty

The thesis for Futu Holdings stock is a geographic diversification and wealth management penetration story: as the company’s revenue base shifts progressively toward Singapore, Malaysia, Japan, Australia, and the United States, dependence on the mainland-exposed revenue pool shrinks and the sustainable earnings multiple should expand.

Adjusted EPS for Q1 2026 came in at HKD 8.11, against a Street estimate of HKD 24.36, a miss of roughly 67%: the entire gap traces to the RMB 1.85 billion CSRC penalty, which was fully reflected as an adjusted subsequent event under U.S. GAAP and is not expected to recur.

Revenue of HKD 5.9 billion missed the HKD 6.03 billion Street estimate by approximately 3%, growing 25% year-over-year against a quarter of elevated market volatility that held down idle cash balances and compressed security lending yields.

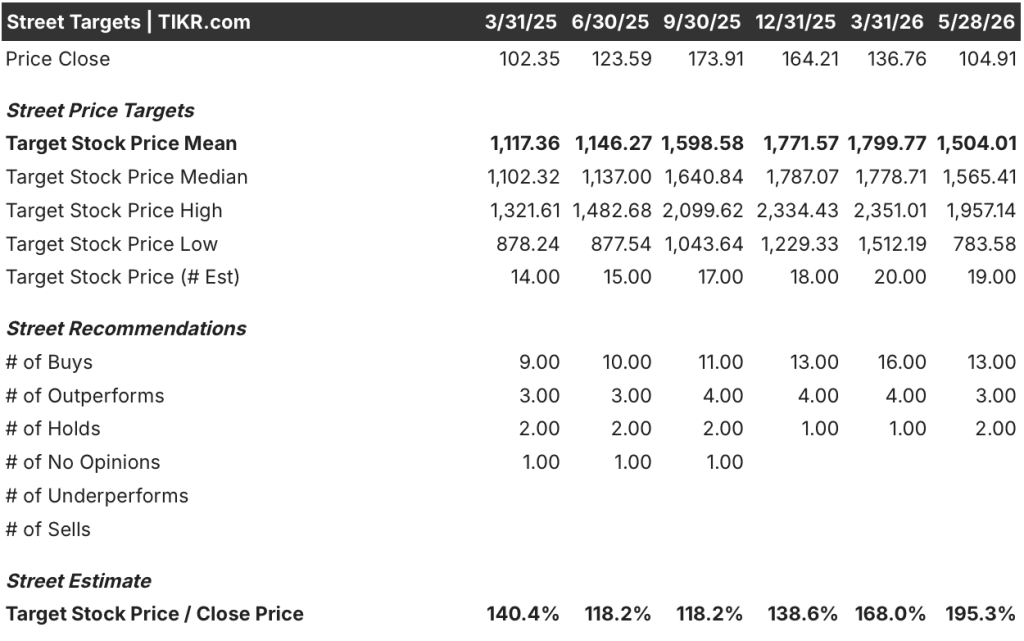

The most recent consensus table shows 13 Buy ratings, 3 Outperforms, 2 Holds, and zero Sells among 18 analysts, with a mean price target of HKD 1,504 per share: at the May 28 close of $104.91, that consensus implies roughly 95% upside, and the skew of 16 Buy or better ratings to 2 Holds reflects analyst conviction that the penalty was isolated, not structural.

Management confirmed that credit facilities remain intact following direct discussions with banking partners and S&P, and that an annual credit rating from S&P is expected imminently, with management expressing confidence in a favorable outcome.

The single metric to watch is the trajectory of overseas adjusted EPS contribution: if Moomoo’s five countries that doubled revenue year-over-year in Q1 sustain that pace and Malaysia reaches breakeven, the 20% mainland revenue share will shrink as an overhang and the earnings multiple should re-rate toward the platform’s international peers.

Is Futu Holdings Stock Undervalued in 2026? The TIKR Model’s Verdict

TIKR’s base case values Futu Holdings stock at approximately $150 by December 2030, implying around 43% total return from the current price of approximately $105, or roughly 8% annualized over 4 and a half years.

If Futu sustains mid-case revenue growth of roughly 12% annually and net income margins around 50%, the model projects a stock price of approximately $199 by December 2034, representing around 89% total return or roughly 8% annualized.

If international expansion stalls and revenue growth tracks the low-case scenario near 10%, the model yields approximately $144, a total return of roughly 38% or around 4% annualized.

If Moomoo’s geographic acceleration holds and margins reach the high-case level near 52%, the stock could reach approximately $267, implying around 154% total return or roughly 12% annualized.

How Did Futu Holdings Perform in Q1 2026 Earnings?

The headline adjusted EPS of HKD 8.11 missed the Street estimate of HKD 24.36 by approximately 67%, but the entire miss reflected a one-time RMB 1.85 billion CSRC administrative penalty fully expensed in the quarter.

Excluding the penalty, adjusted net income would have grown 36% year-over-year to HKD 2.9 billion, with a net income margin of 49.9%.

Total trading volume hit a record HKD 4.15 trillion, up 29% year-over-year, and funded accounts reached 3.59 million, up 34% year-over-year.

Management maintained the full-year guidance of 800,000 net new funded accounts, signaling no operational disruption from the regulatory action.

Is Futu Holdings Stock a Buy?

TIKR’s base case values Futu Holdings stock at approximately $150 by December 2030, implying around 43% total return from the current price near $105, or roughly 8% annualized.

The operating foundation supports that case: funded accounts grew 34% year-over-year to 3.59 million, total client assets rose 47% year-over-year, and pre-penalty net income margin was approximately 50%.

The central condition is regulatory normalization: if the CSRC penalty proves non-recurring and mainland revenue exposure continues to shrink as overseas markets scale, the base case return profile is well-supported.

Should You Invest in Futu Holdings Limited?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Futu Holdings Limited stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Futu Holdings Limited alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FUTU stock on TIKR for Free →