Key Stats for Agilent Technologies Stock

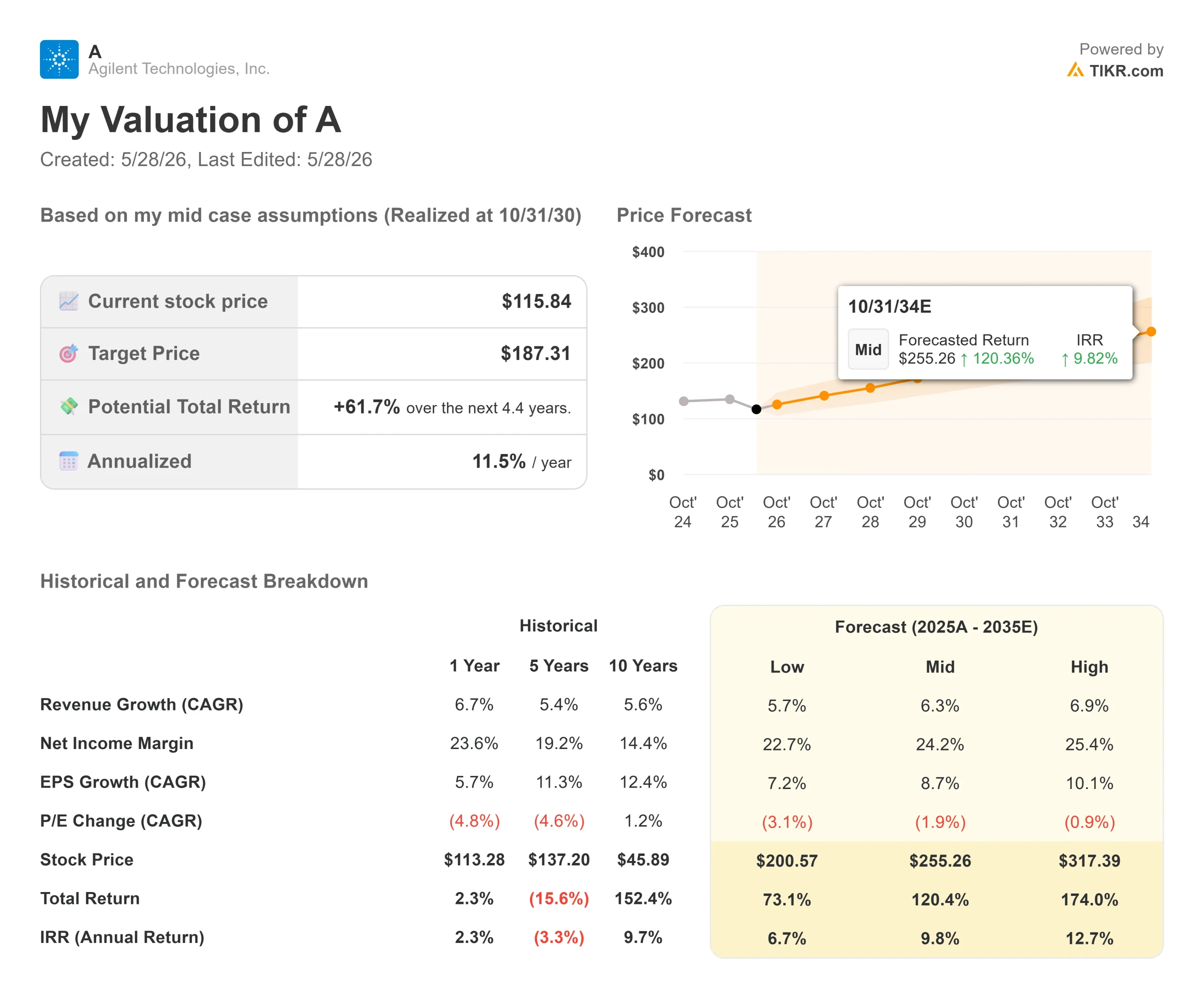

- Current Price: $115.84

- Target Price (Mid): ~$187

- Street Target: ~$161

- Potential Total Return: ~62%

- Annualized IRR: ~12% / year

- Earnings Reaction: +0.66% (May 27, 2026)

- Max Drawdown: 29.87% on 3/27/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Agilent Technologies (A) delivered one of the cleanest earnings beats in its sector this week, and the stock barely moved. That disconnect is worth interrogating.

On May 27, the Santa Clara-based maker of analytical laboratory instruments reported $1.83 billion in Q2 revenue, growing 6.3% on a core organic basis and exceeding the high end of its own guidance by 80 basis points. Non-GAAP EPS of $1.49 beat the Street consensus of $1.41 by $0.08, representing 14% year-over-year growth. Management raised both revenue and EPS guidance for full-year FY2026. The stock closed up 0.66%.

The muted reaction tells you what the market still believes: the improvement is real but fragile, China remains a drag, and the stock, about 28% below its 52-week high of $160.27, is coming off a multi-year correction that one quarter cannot fully reprice. That skepticism is not irrational. But the results make a structural case that the stock price has not yet acknowledged.

What Drove the Beat

The strength was broad across end markets. Pharma grew 6% for the fifth consecutive quarter. Chemicals and Advanced Materials grew 8%, ahead of a mid-single-digit guide, driven by semiconductor capital spending and chemical investment in the Americas. Diagnostics and Clinical grew 11%, led by the Omnis platform, an automated immunohistochemistry (IHC) system used to detect disease markers in tissue samples. Environmental and Forensics came in at 13% against a low single-digit guide.

Part of the forensics outperformance came from a specific contract win. Agilent recognized $5 million from a $9 million TSA award to deploy its bulk alarm resolution technology at FIFA World Cup 2026 security checkpoints across the U.S. CEO Padraig McDonnell noted on the earnings call that the successful rollout positions Agilent “to continue to secure larger aviation security tenders” going forward.

On instruments, liquid chromatography (LC) and LC/MS a technique that separates and identifies chemical compounds by mass both grew at a low double-digit rate, as did gas chromatography (GC). Book-to-bill stayed above 1 for the ninth consecutive quarter, meaning orders continue to exceed revenue. McDonnell called the market share gains “the best I’ve seen,” pointing to aging instrument fleets and improving capital spending conditions in the U.S. and Europe.

The margin story was equally strong. Operating margin expanded 130 basis points year-over-year to 26.4% and 180 basis points sequentially. Strategic pricing contributed approximately 200 basis points in Q2, already double the full-year target of 100 basis points. CFO Adam Elinoff credited the Ignite operating system, Agilent’s internal framework for driving pricing discipline, procurement savings, and manufacturing efficiency. Manufacturing overhead fell more than 50 basis points versus the prior year.

See historical and forward estimates for Agilent Technologies stock (It’s free!) >>>

The Biocare Acquisition

Layered into this recovery is Agilent’s pending $950 million all-cash acquisition of Biocare Medical, announced March 9, 2026. Biocare is a clinical pathology company with more than 300 specialized antibodies and a portfolio covering immunohistochemistry (IHC), in situ hybridization (ISH), and FISH fluorescence in situ hybridization, a technique used to detect chromosomal abnormalities in cancer diagnostics. The company generated over $90 million in revenue in 2025, with double-digit revenue and profit growth every year since 2021.

The deal is expected to close by Q4 FY2026 and to be accretive to EPS approximately 12 months after closing. Biocare’s antibody menu directly complements the Omnis platform that already grew low double digits this quarter, adding a recurring reagent revenue stream to a segment that is already Agilent’s fastest-growing.

The balance sheet can absorb it. Net leverage stood at 0.7 turns of EBITDA at quarter-end, and management guided operating cash flow of $1.6 billion to $1.7 billion for the full year. A $950 million all-cash transaction at those leverage levels carries manageable balance sheet risk.

What the Bears Still Have Right

Three concerns have been weighing on the stock, and Q2 did not fully resolve them.

China declined 9% in Q2. Management guided the full-year China segment to be roughly flat, with anticipated government stimulus now expected to benefit FY2027 rather than FY2026. Agilent is over-indexed to Applied Markets in China, a more cyclical segment, which limits how much it benefits from biotech strength there.

Academic and government spending fell 5%, in line with expectations. The U.S. portion represents roughly 3% to 4% of total company sales, and while America’s instrument comparables are stabilizing, multiyear grant uncertainty has not cleared.

Food declined 3% against a mid-single-digit guide, due to delayed government funding in China and India, and Middle East conflict pressures on food shipments and testing in Asia. Management lowered the full-year food outlook to a low single-digit decline.

H2 comparables get tougher from here. The guidance raise was measured 30 basis points at the core revenue midpoint, $0.08 at the EPS midpoint, which reflects both genuine momentum and an acknowledgment that the back half needs to be earned. Investors tracking earnings revisions will want Q3 execution before pushing the multiple higher.

See how Agilent Technologies performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $115.84

- Target Price (Mid): ~$187

- Potential Total Return: ~62%

- Annualized IRR: ~12% / year

See analysts’ growth forecasts and price targets for Agilent Technologies stock (It’s free!) >>>

Using the mid case, the TIKR Valuation Model assumes a revenue CAGR of around 6% and a net income margin of around 24%, arriving at a target of approximately $187 by October 31, 2030. That implies around 62% total return and an annualized IRR of approximately 12% from today’s price of $115.84.

The two revenue drivers the model depends on are pharma end-market expansion and the instrument replacement cycle. Pharma has delivered five consecutive quarters in the mid-to-low double-digit range, with GLP-1 manufacturing demand tracking approximately 20% growth year-to-date through Q2. The LC and GC replacement cycle adds a multi-year tailwind that does not require new customer wins it just requires aging fleets to be replaced, which the funnel data and nine consecutive book-to-bill readings above 1 support.

The margin driver is Ignite. Agilent guided 85 basis points of full-year operating margin expansion at the FY2026 midpoint. The primary risk to the model is China and Middle East-driven cost inflation. If either worsens materially, free cash flow could miss the $1.6 billion to $1.7 billion guidance range, pulling the 2030 scenario price toward the low case.

On valuation multiples, Agilent trades at 15.66x NTM EV/EBITDA, a discount to Waters Corporation at 16.93x and Sartorius at 17.09x, and a modest premium to Revvity at 14.62x. All three are comparable life sciences tool businesses. The Street’s mean price target of around $161, reflecting 10 Buys, 5 Outperforms, and 3 Holds already implies roughly 39% upside. The TIKR mid-case extends that to approximately $187 by October 2030, contingent on Ignite delivering compounding margin gains and pharma demand sustaining through the decade.

Conclusion

The most important near-term catalyst is the Biocare close, guided by Q4 FY2026. If it arrives on schedule, the FY2027 EPS accretion story enters guidance language in Q3, which could trigger the re-rating that Q2 alone did not deliver. A delay leaves the stock dependent on H2 execution against tougher comparables.

Watch Q3 2026 earnings, expected around August 26, 2026. Beat again with Biocare on track, and the case for approximately $187 by October 2030 becomes significantly harder to dismiss.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Agilent Technologies?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Agilent Technologies, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Agilent Technologies alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Agilent Technologies on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!