Key Stats for Marvell Technology Stock

- Current Price: $198.70

- TIKR Mid-Case Target: ~$556

- Potential Total Return: ~180%

- Annualized IRR: ~25% / year

- Most Recent Earnings Reaction: +18.35% (reported 3/5/2026)

- Max Drawdown: 26.42% on 2/4/2026

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Marvell Technology (MRVL) designs the custom silicon and high-speed optical interconnects that power the world’s largest AI data centers. After hours on May 27, the stock rose roughly 3.5% following a Q1 fiscal 2027 earnings report that beat on both revenue and earnings per share. The headline beat was modest. The guidance raised was not.

CEO Matt Murphy raised fiscal 2028 revenue guidance to approximately $16.5 billion, around $1.5 billion above the figure management issued just one quarter prior. That makes four consecutive multi-billion-dollar upward revisions to Marvell’s medium-term outlook in under twelve months. The question investors are sitting with now is not whether Marvell is growing. It is whether the market is pricing the right number.

A Record Quarter, Then the Real Story

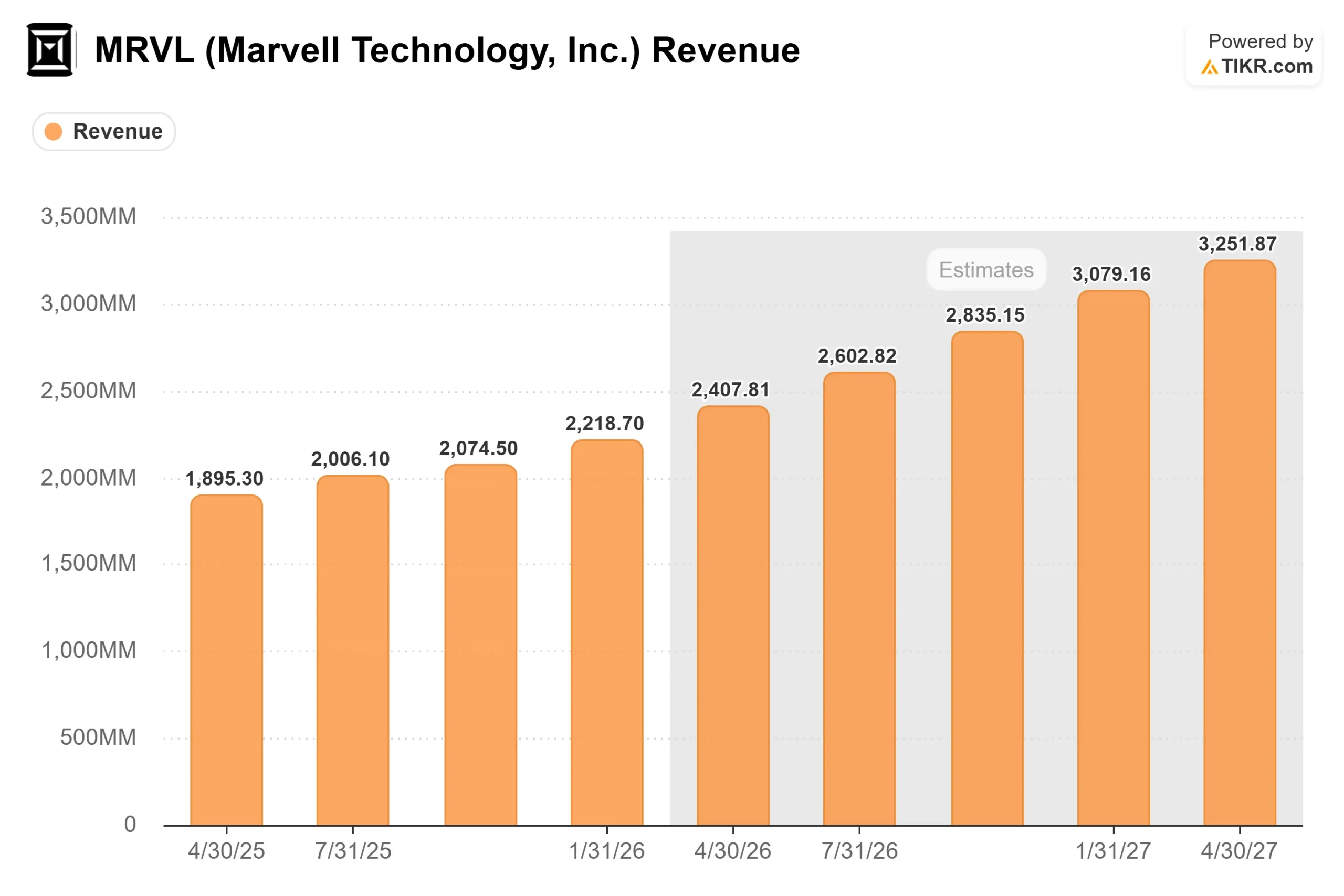

Marvell reported Q1 fiscal 2027 net revenue of $2.418 billion, a new company record, up 28% year-over-year and 9% sequentially. Revenue came in $18 million above the midpoint of guidance. Non-GAAP EPS was $0.80, one cent above the guidance midpoint. Data center revenue reached $1.83 billion, up 11% sequentially and 27% year-over-year, making up 76% of total company revenue. Operating cash flow hit a record $639 million in the quarter, per the earnings call.

The guidance is what matters more. Murphy called for Q2 fiscal 2027 revenue of approximately $2.7 billion, around 35% year-over-year growth. He added that Q3 and Q4 would each grow at least 10% sequentially, pulling the $3 billion quarterly revenue milestone one full quarter ahead of schedule. Full fiscal 2027 revenue is now expected at approximately $11.5 billion, up around 40% year-over-year. Fiscal 2028 is now guided to approximately $16.5 billion, up around 45% year-over-year. Both figures are management guidance from the May 27 earnings call and reflect the most recent outlook, ahead of street consensus estimates.

Three Growth Engines

Murphy broke the data center business into three categories. Each one is accelerating.

Interconnect is the largest and fastest-growing segment. Marvell now expects interconnect revenue to grow more than 70% year-over-year in fiscal 2027, raised from a prior expectation of 50%. The driver is surging demand for 1.6-terabit-per-second (1.6T) solutions, the next generation of high-speed optical data links inside AI clusters. Murphy also pointed to the data center interconnect (DCI) market, where Marvell ships to all five major U.S. hyperscalers and pioneered the pluggable DCI module category. He said the DCI business is on track for a $1 billion annualized revenue run rate in fiscal 2028, roughly double the approximately $500 million it generated in fiscal 2026. A newer opportunity called “scale across,” where AI workloads must span multiple data centers simultaneously, is expected to push DCI growth further, with aggregate bandwidth requirements Murphy described as more than 10 times higher than current front-end DCI networks.

Custom silicon is where the multi-year stakes are highest. Murphy confirmed that Marvell’s custom business, which designs application-specific chips called XPUs (accelerated processing units) directly for hyperscaler customers, is expected to more than double year-over-year in fiscal 2028. He said growth will come from three roughly equal sources: a continued ramp of existing XPU programs, over ten XPU-attached products reaching higher production volumes, and a new Tier 1 XPU program entering volume production in fiscal 2028 with firm customer requirements already locked in. Murphy also reaffirmed Marvell’s target of delivering over $10 billion in custom revenue in fiscal 2029.

Switching is the smallest piece today, with the most open-ended upside. Scale-out switch revenue is expected to exceed $600 million in fiscal 2027, doubling from fiscal 2026, with a path to more than $1 billion annualized by fiscal 2028. The scale-up switching opportunity, covering next-generation protocols including UALink, ESUN, and NVLink, currently contributes little to projections. Murphy described each engagement as a multibillion-dollar lifetime revenue opportunity. None of that upside is baked into the $16.5 billion fiscal 2028 figure.

See historical and forward estimates for Marvell Technology stock (It’s free!) >>>

The NVIDIA Partnership

On March 31, 2026, NVIDIA announced a $2 billion investment in Marvell alongside a partnership built around NVLink Fusion, a platform that lets hyperscalers build semi-custom AI infrastructure fully compatible with NVIDIA’s software ecosystem. The partnership covers silicon photonics collaboration, direct chip-level integration between Marvell’s custom silicon and NVIDIA infrastructure, and AI-RAN (AI-enabled radio access network) technology for 5G/6G networks. Murphy said the two companies are “off to the races” following the announcement. The structural effect is that Marvell’s custom silicon path is now formally connected to the NVIDIA ecosystem rather than positioned apart from it, reducing the friction for hyperscalers choosing between the two.

What the Valuation Reflects

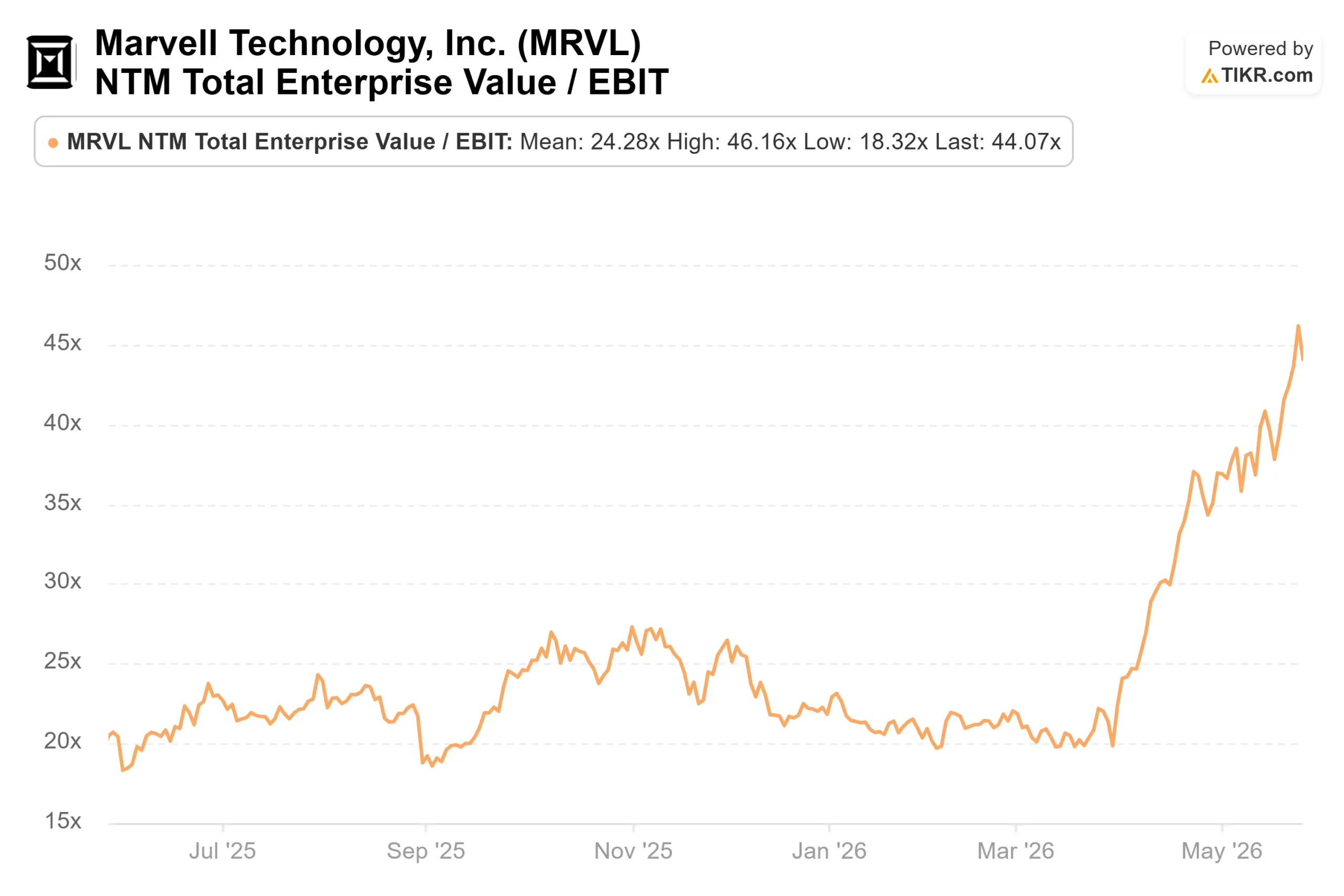

At $198.70, Marvell trades at 16.06x NTM EV/Revenue and 51.61x NTM P/E per TIKR. Both are premium figures. Broadcom, the closest peer, trades at 17.15x NTM EV/Revenue and 31.53x NTM P/E. NVIDIA trades at 11.74x NTM EV/Revenue and 21.32x NTM P/E. The peer-group median NTM EV/Revenue across 36 semiconductor peers sits at 6.75x per TIKR’s competitors’ data.

Marvell’s premium over the median is large. The argument for it is that revenue growth is accelerating off a large base: fiscal 2026 revenue of $8.19 billion grew 42.1% year-over-year per TIKR, and management is guiding for growth to reach around 50% in fiscal 2027 and around 55% in fiscal 2028 for the data center segment alone. Non-GAAP operating margin was 35% in Q1, with CFO Willem Meintjes guiding toward the upper end of a 38-40% target range in fiscal 2028. If margins reach that level, the earnings multiple compresses meaningfully from today.

The main risk is customer concentration. The top U.S. hyperscalers account for the majority of data center revenue, and a CapEx deceleration or a single program delay would put material pressure on the $16.5 billion target. Murphy acknowledged cloud CapEx growth is expected to moderate into the 30%-plus range in fiscal 2028. His argument is that Marvell’s content gains in interconnect and custom silicon will outpace that moderation. That argument has been right for four consecutive quarters.

See how Marvell Technology performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $198.70

- TIKR Mid-Case Target: ~$556

- Potential Total Return: ~180%

- Annualized IRR: ~25% / year

See analysts’ growth forecasts and price targets for Marvell Technology stock (It’s free!) >>>

TIKR’s mid-case model projects approximately 25% annualized revenue growth through January 31, 2031, with net income margins expanding toward approximately 30%. The two revenue growth drivers are optical interconnect compounding as 1.6T ramps extend the product cycle past fiscal 2028, and custom silicon breadth as Marvell builds XPU-attached revenue across multiple hyperscaler relationships rather than depending on a single program. The margin driver is operating leverage: management has guided non-GAAP opex to grow in the mid-to-high teens percentage range in fiscal 2028 while revenue grows approximately 45%, meaning significantly more revenue flows through to earnings.

The high case, at approximately 27% revenue CAGR, puts the stock near $1,324 by January 31, 2031. The downside risk is a hyperscaler CapEx correction, which would deflate the premium valuation multiples quickly, given how much of today’s price reflects future cash flows.

Conclusion

Murphy has guided for Q2 fiscal 2027 revenue of approximately $2.7 billion. The Q2 earnings report, expected in late August 2026, is the next confirmation point. The threshold is straightforward: revenue at or above $2.7 billion, data center growing into the mid-40% range year-over-year, and interconnect tracking above 70% annual growth. A clean beat confirms the $16.5 billion fiscal 2028 path. Any cut to the interconnect growth rate would be the first crack in a guidance track record that has been raised, not lowered, four consecutive times.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Marvell Technology?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Marvell Technology, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Marvell Technology alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Marvell Technology on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!