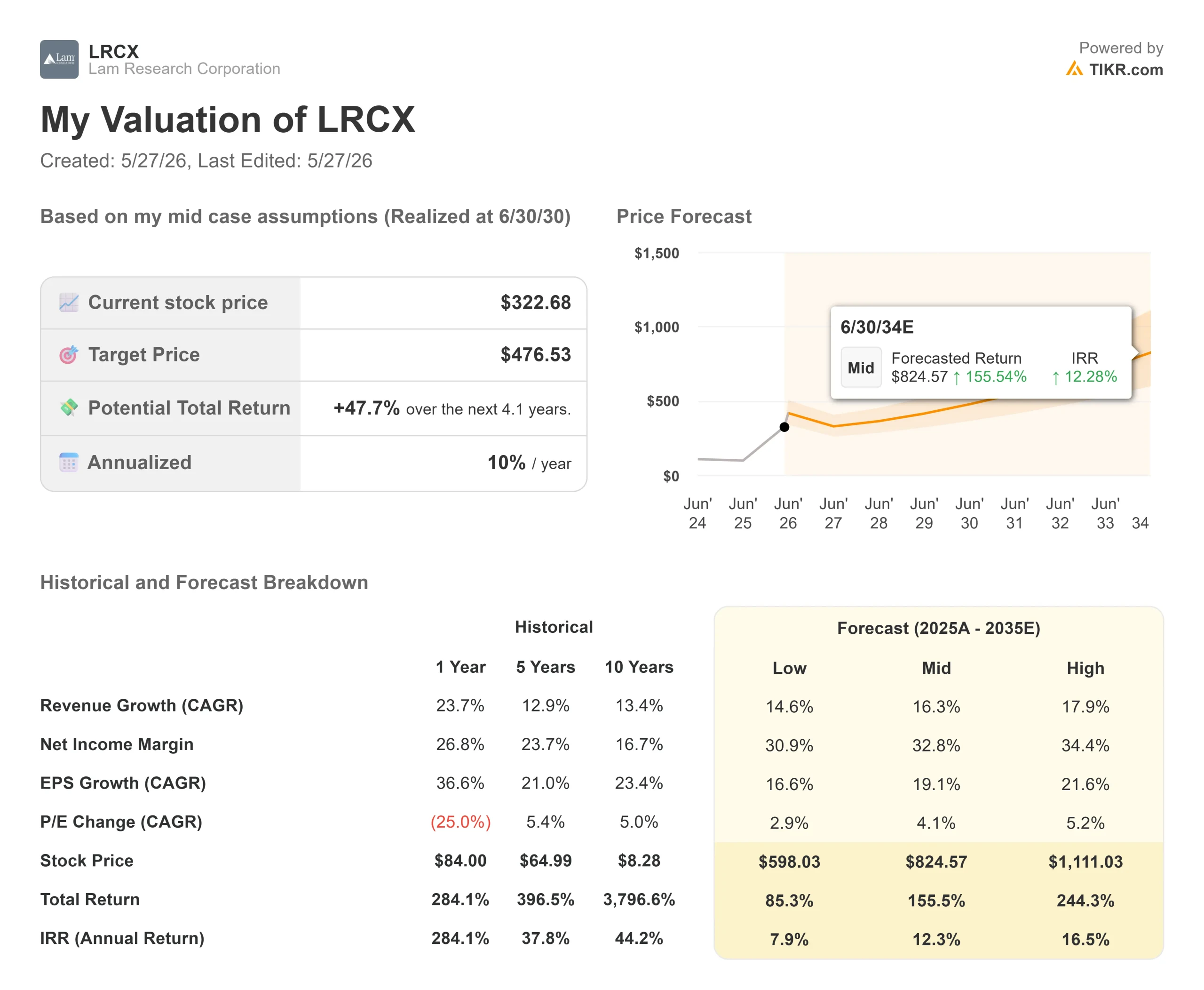

Key Stats for Lam Research Stock

- Current Price: $322.68

- TIKR Target Price (Mid-Case): ~$477

- Street Mean Target: ~$312

- Potential Total Return: ~48%

- Annualized IRR: ~10% / year

- Earnings Reaction: -2.63% (April 22, 2026)

- Max Drawdown: -20.10% (March 6, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Lam Research Corporation (LRCX) just received a pointed vote of confidence from one of Wall Street’s most-watched semiconductor analysts, and the reasoning goes well beyond last quarter’s results.

On May 18, Morgan Stanley upgraded LRCX to Overweight from Equal-weight, raising its price target to $331 from $293. The same call cut Applied Materials (AMAT) to Equal-weight. That simultaneous rotation is the signal: Morgan Stanley now believes NAND flash memory storage is about to become the fastest-growing segment in the global wafer fabrication equipment market in 2027, and that Lam captures more of that spending than any peer.

Sanford C. Bernstein followed days later, raising its price target to $340 and maintaining Outperform. LRCX now trades near its 52-week high of $323.98. The market has already priced in strong execution. The question is whether the 2027 NAND setup is fully priced in yet.

Why Morgan Stanley Made the Switch

Morgan Stanley’s upgrade is built around one central projection: 59% NAND systems growth in calendar year 2027, which would push NAND WFE spending above its 2021 peak. The logic runs directly through what CEO Tim Archer told investors on the Q3 2026 earnings call in April.

Lam had already raised its 2026 wafer fabrication equipment (WFE) market outlook from $135 billion to $140 billion, with an upward bias. Archer went further: the $40 billion in NAND conversion spending the company had previously flagged as spread over several years would now largely land before the end of 2027. “We now anticipate that this conversion will be pulled forward,” Archer said, “with the majority of spending occurring before the end of calendar year 2027.”

The driver is AI data centers shifting toward higher-layer count QLC-based NAND devices for SSDs. QLC, or quad-level cell, stores four bits per memory cell instead of the three bits used in standard TLC NAND, enabling more storage per wafer at lower cost. Archer noted that data center NAND bit demand is on track to exceed both PC and mobile combined in 2026. Reaching the 256-layer-and-above devices that AI data centers require means adding etch and deposition steps at every layer, exactly where Lam generates revenue.

The Applied Materials rotation reinforces the logic from the other direction. DRAM was the fastest-growing WFE end market in 2026. Morgan Stanley expects it to be the slowest in 2027. AMAT carries heavier DRAM exposure. Lam has NAND.

See historical and forward estimates for Lam Research stock (It’s free!) >>>

A Record Quarter the Market Took in Stride

On April 22, Lam reported Q3 2026 revenue of $5.84 billion, up 24% year-over-year and 9% sequentially its third consecutive record quarter. Adjusted EPS of $1.47 beat the top end of the company’s own guided range. The stock fell 2.63% that day, reflecting a market more focused on the 2027 trajectory than the quarter just printed.

CFO Doug Bettinger guided June quarter revenue to $6.6 billion (plus or minus $400 million), gross margin to 50.5%, operating margin to 36.5%, and EPS to $1.65, all records at their midpoints. He added that gross margins would “level out at where it’s at” through the remainder of the year, crediting factory efficiency gains from Lam’s manufacturing buildout in Malaysia.

The Customer Support Business Group (CSBG), which covers spares, upgrades, and services for Lam’s installed base, crossed $2.11 billion in quarterly revenue for the first time, up 25% year-over-year. CSBG compounds, regardless of where new equipment orders sit in the cycle, with Lam’s installed base exceeding 100,000 chambers and industry utilization running near its ceiling, this business provides a meaningful earnings floor.

Within memory systems, DRAM reached a record 27% of systems revenue in Q3, driven by high-bandwidth memory investment and the transition to 1c-generation nodes. Lam’s Striker ALD solution for bitline spacer applications is the tool of record at all leading memory makers for 1c node transitions, with the company expecting its total dielectric deposition served available market in DRAM to grow more than 20% as those nodes scale.

The Packaging Bet Investors Are Underweighting

On May 20, Lam announced a Panel-Level Packaging Center of Excellence in Salzburg, Austria, built on the foundation of Semsysco GmbH, a wet-process equipment firm it acquired in 2022. As reported by Reuters, the facility is Lam’s first wet-processing lab dedicated to panel-level packaging, a technology that replaces circular silicon wafers with square panels, eliminating material waste at the curved edges and producing more chips per surface at lower cost per unit.

This matters because Archer confirmed on the Q3 call that advanced packaging revenue is expected to grow more than 50% in calendar year 2026. The Salzburg lab positions Lam directly in the path of AI chipmakers pushing toward denser architectures that conventional round wafers cannot efficiently support.

The Dextro cobot program adds another dimension. Dextro is Lam’s collaborative robot for automated tool maintenance inside fabs. Lam expanded Dextro coverage to eight tool types in Q3, up from six, and shipped its first unit for a deposition product. Customers running Dextro report improved fab output and in some cases better yield from existing capacity a metric that matters enormously when clean room space is the binding constraint across the industry.

On peer valuation, Applied Materials trades at around 9x NTM EV/Revenues and around 31x NTM EV/EBITDA, per TIKR data. Lam trades at around 14x NTM EV/Revenues and around 37x NTM EV/EBITDA. The premium is real. Whether it holds depends on whether Lam’s NAND-weighted mix and CSBG compounding produce structurally better earnings growth over a full cycle than peers can deliver. Morgan Stanley’s upgrade says yes.

See how Lam Research performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $322.68

- Target Price (Mid-Case): ~$477

- Potential Total Return: ~48%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Lam Research stock (It’s free!) >>>

The TIKR mid-case model prices LRCX at around $477 by June 2030, a roughly 48% total return from today and an annualized IRR of around 10% per year. Two drivers anchor the revenue CAGR of around 16%: the NAND conversion and greenfield cycle accelerating into 2026 and 2027, and CSBG compounding on an installed base exceeding 100,000 chambers. The margin driver is operating leverage on a manufacturing base already scaled in Malaysia, with gross margins at the model’s long-term target level ahead of schedule.

The 48% mid-case return over four years reflects a stock already trading at a premium on every forward multiple. The Street’s mean target of $312.13 from 37 analysts, 25 Buys, 4 Outperforms, 6 Holds, 1 Underperform, 1 No Opinion, actually sits below the current price, suggesting the market has already priced in significant execution. Lam’s ROIC of 51.9% and return on equity of 66.8% reflect a business with genuine pricing power and customer switching costs that support the floor, but the upside case is a NAND execution story.

The primary risk: if clean room additions don’t open up on schedule in 2027, NAND greenfield orders slip into 2028, and the around 43x forward P/E compresses before earnings can grow into it.

Conclusion

The thesis resolves at Lam’s Q4 2026 earnings call, expected around late July 2026. The key number to watch is NAND as a percentage of systems revenue, which sat at 12% in Q3. A visible move higher confirms the acceleration Morgan Stanley is betting on. If NAND stalls while DRAM softens, the premium is harder to defend.

Bettinger flagged on the April call that Lam will update its long-term financial targets later in 2026. That update, whenever it arrives, is the second catalyst worth watching. It will clarify how far operating margins can expand beyond the 36.5% guided for June, and whether the TIKR model’s 33% net income margin assumption is conservative or already baked in. July is the first checkpoint.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Lam Research?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Lam Research, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lam Research alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Lam Research on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!