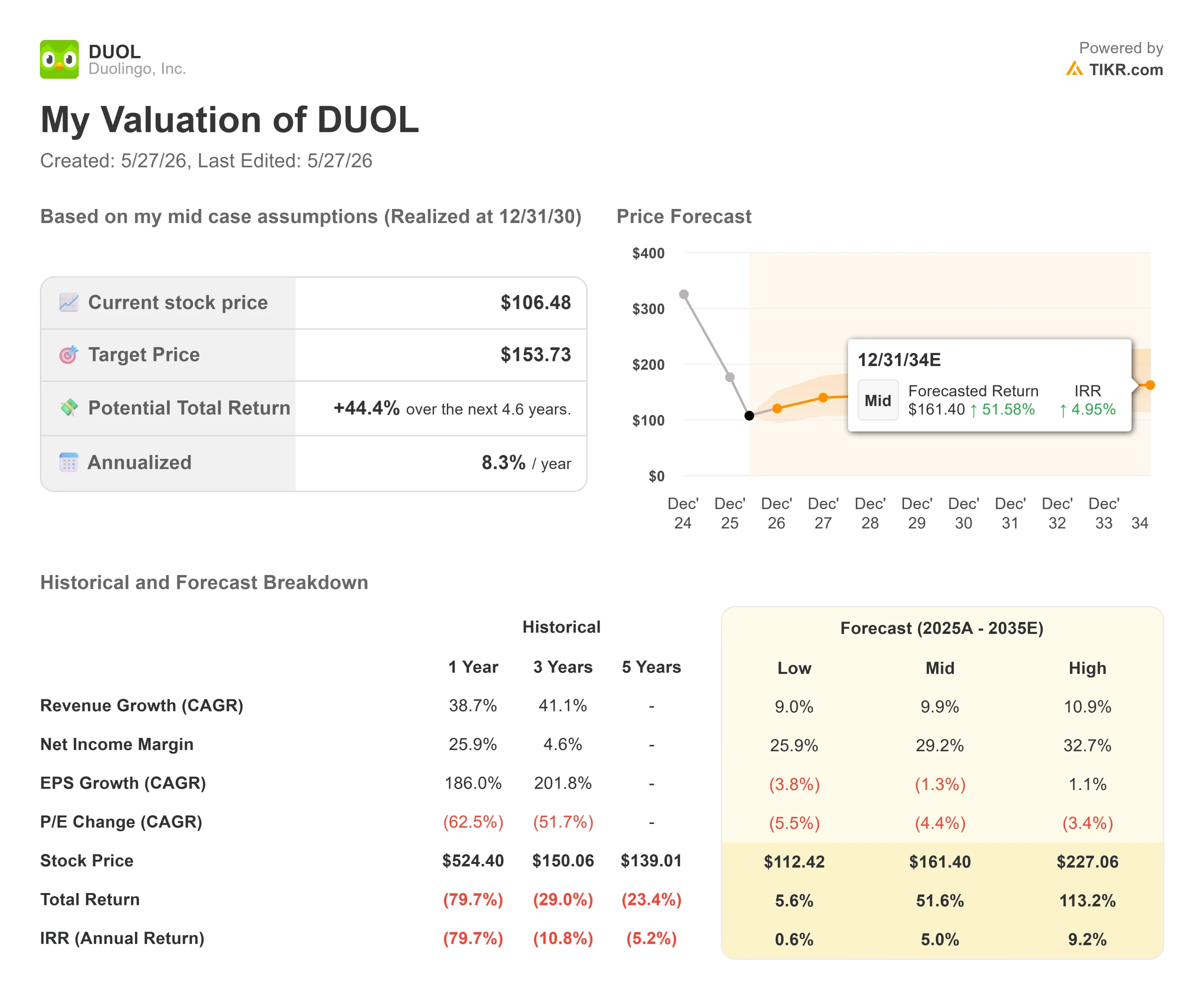

Key Stats for Duolingo Stock

- Current Price: $106.48

- Target Price (Mid): ~$160

- Street Mean Target: ~$105

- Potential Total Return (Mid): ~52%

- Annualized IRR: ~5% / year

- Max Drawdown: 82.91% on April 10, 2026

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Duolingo, Inc. (DUOL) beat every number Wall Street set for Q1 2026. Revenue of $291.97 million topped estimates by 1.18%. GAAP EPS of $0.89 cleared the $0.71 consensus by 25%. Adjusted EBITDA of $83.43 million beat by nearly 14%. The stock still dropped nearly 14% in after-hours trading on May 4.

The selloff was driven by Q2 bookings guidance of around 6% growth and a full-year bookings target below analyst models. That concern is legitimate. But whether DUOL at $106 is a buy or a value trap depends less on that number and more on something CEO Luis von Ahn said on the May 4 earnings call that most coverage missed.

“We are at the same time undermonetized and overmonetized,” von Ahn told analysts. “It is a weird thing.”

That paradox and what Duolingo is doing to resolve it is the real investment thesis right now.

The Paradox Behind the Pivot

Only about 12% of Duolingo’s monthly active users are paying subscribers. Von Ahn noted on the call that Spotify’s ratio sits “close to 50%,” suggesting the platform has far more conversion runway than its current paying base implies. That’s the undermonetized side.

The overmonetized side: certain friction-based tactics were pushing some users to subscribe while pushing others off the platform entirely. In von Ahn’s words, many of those tactics were “at odds with DAU growth.” The 2026 pivot is a direct response to finding monetization methods that don’t require sacrificing user growth to generate revenue.

The clearest example is free trial length. Duolingo has historically offered a 7-day free trial for its Super subscription. The company is now testing 1-month trials, with 3-month trials in the pipeline. Von Ahn explained the tradeoff directly: a 3-month trial delays booking recognition by a full quarter, which is precisely why management gave itself a full investment year with wide guidance ranges. The early results on the 1-month experiment, per von Ahn, are boosting both revenue and user satisfaction simultaneously.

See historical and forward estimates for Duolingo stock (It’s free!) >>>

What AI Has Actually Changed

In Q1 2026, Duolingo published 20,500 course units, more than 10 times what it was producing per quarter two years ago, and roughly equal to its entire prior year’s output. Von Ahn was direct: “AI has fundamentally changed what’s possible for us.”

This matters for growth because Duolingo now offers courses to B2 proficiency level, the professional standard on the Common European Framework of Reference for Languages (CEFR), across its nine most-learned languages. Learners who previously had nowhere to go after intermediate content now have a reason to stay.

On costs, CFO Gillian Munson explained that Q1 gross margin came in at 73.0%, better than expected, despite heavy AI deployment because per-unit AI costs have compressed through optimization. Margin is still guided to decline to around 69% by Q4 as more AI features roll out, but Munson described this as a deliberate product investment, not a cost blowout.

The video call feature illustrates both sides. The average words spoken per user in video calls have more than doubled over the past year. The company is now testing bringing this feature, previously exclusive to the premium Duolingo Max tier, down into the standard Super subscription. Early data shows users are willing to pay more for Super with video calls. How much more is still being tested, and the answer could meaningfully shift average revenue per user (ARPU).

Where Duolingo Stands Versus Peers

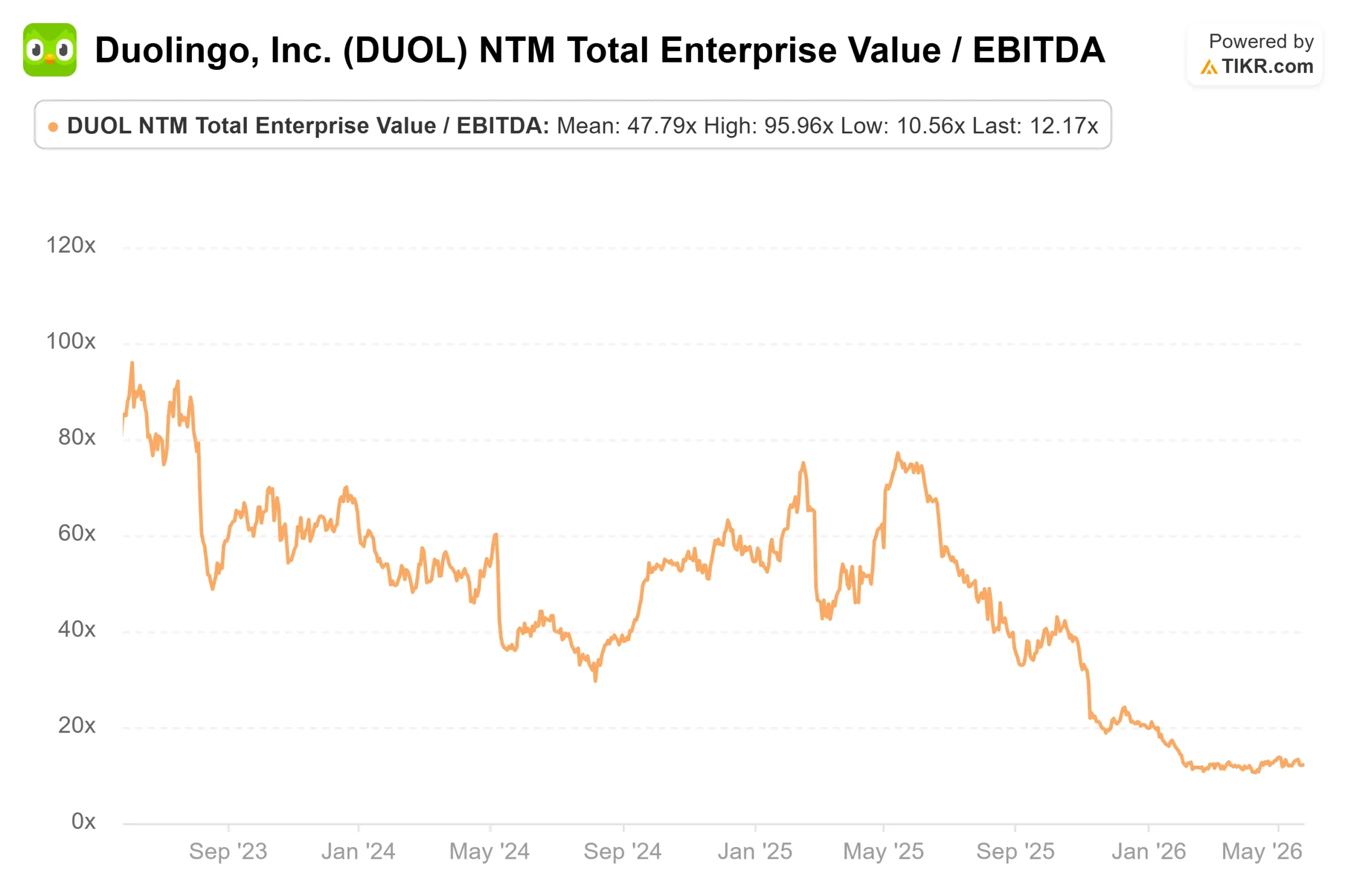

Duolingo trades at a meaningful premium to its edtech peers, but the gap reflects genuine differences in scale and engagement. According to TIKR’s Competitors page, Pearson (PSON) trades at 2.13x NTM EV/Revenue and 9.21x NTM EV/EBITDA. Stride (LRN) sits at 1.33x and 5.52x. Coursera (COUR) trades at 0.89x and 9.34x. Duolingo is at 3.07x and 12.17x.

The premium is supported by a free cash flow profile none of those peers can match: LTM levered FCF of $312.47 million, and Q1 2026 FCF of $147.79 million against an estimate of $68 million. The business is generating substantial cash while absorbing deliberate investment. Whether the valuation premium is justified at current levels depends entirely on what the free trial and ARPU experiments deliver in the second half of 2026.

See how Duolingo performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $106.48

- Target Price (Mid): ~$160

- Potential Total Return: ~52%

- Annualized IRR: ~5% / year

See analysts’ growth forecasts and price targets for Duolingo stock (It’s free!) >>>

The mid-case model assumes a revenue CAGR of around 10% and net income margins expanding to around 29%. The two revenue growth drivers are subscriptions, the dominant segment at $873.44 million in FY2025, and advertising, which grew from $54.91 million in 2024 to $79.73 million in 2025, the fastest-growing segment by percentage. The margin driver is operating leverage as per-unit AI costs continue to compress. The primary risk is timing: the model assumes deferred bookings from free trial experiments start converting in 2027. If they don’t, the multiple stays are compressed.

The Street’s mean target sits at approximately $105, essentially at the current price, reflecting consensus that DUOL is fairly valued with no near-term catalyst. The TIKR model diverges significantly. The high case puts the stock at around $227 by 12/31/30, implying over 100% total return, assuming revenue CAGR near 11% and net income margins near 33%.

The current analyst distribution 2 Buys, 2 Outperforms, 18 Holds, 1 Sell reflects a Street that has seen consistently strong operating earnings surprises but continues to wait for bookings guidance to confirm the pivot is working.

Conclusion

The single number to watch is Q3 2026 bookings. CFO Munson guided approximately 3 percentage points of acceleration in Q3 relative to Q2’s guided 6% growth, before rising further in Q4. If Q3 comes in materially below that, it signals the free trial experiments are deferring more revenue than modeled. If it meets or beats, it confirms the Q2 weakness was exactly the one-quarter comp anomaly management described, driven by last year’s pricing increase and the Energy feature rollout, and the pivot thesis holds.

The Q3 2026 earnings call, expected in early November, is the first real verdict.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Duolingo?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Duolingo, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Duolingo alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Duolingo on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!