Key Stats for Champion Homes Stock

- Current Price: $72 (May 26, 2026)

- Q4 FY2026 Revenue: $621.3M, +4.6% YoY

- Q4 FY2026 Adjusted EPS: $0.68, +4.6% YoY

- Q4 FY2026 Adjusted EBITDA: $55.9M, +6.3% YoY

- Q1 FY2027 Revenue Guidance: Approximately flat YoY

- Q1 FY2027 Adjusted Gross Margin Guidance: 24.5%–25.5%

- TIKR Model Price Target: $102

- Implied Upside: ~42%

Champion Homes Sells a Record Number of Houses While Input Costs Start to Eat the Margin

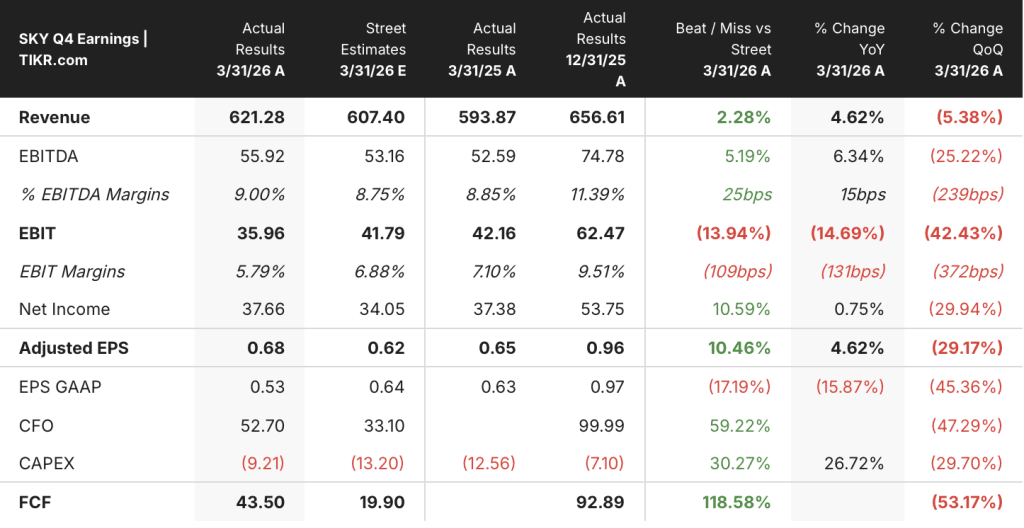

Champion Homes, Inc. (SKY) reported Q4 FY2026 net sales of $621.3M on May 26, a 4.6% increase year-over-year that came in ahead of management’s own low-single-digit growth expectation.

The quarter was driven by a meaningful shift in average selling price rather than volume growth. The average selling price per U.S. home increased 4.6% to $98,600, pulled higher by a mix shift toward multi-section homes and stronger pricing through company-owned retail.

U.S. homes sold in Q4 decreased 0.6% to 5,908, while Canadian volume grew from 230 to 243 units, with Canadian revenue benefiting from both higher volume and favorable foreign exchange rates.

Adjusted gross profit increased 4.6% to $159.4M, with adjusted gross margin at 25.7%, essentially unchanged from the prior year quarter. Adjusted EBITDA rose 6.3% to $55.9M, with EBITDA margin ticking up slightly to 9% from 8.9%.

Adjusted net income attributable to Champion Homes increased 1% to $37.7M or $0.68 per diluted share, above Street estimates of $0.62. The effective tax rate of 20.3% was higher than the 17.1% rate in the year-ago period.

For the full fiscal year, Champion Homes sold 26,622 homes, a record since the company went public in 2018. Timothy Larson, President and CEO, stated on the Q4 earnings call that “across Champion, we earned the business of 26,622 customers in fiscal 2026, the record number of homes sold since the company went public in 2018.”

Operating cash flow for the full fiscal year reached $303.9M, up 26.2% from $240.9M in fiscal 2025. Champion repurchased $200M of common stock during the year and refreshed its buyback authorization to $150M in early May.

The company announced the acquisition of Homes Direct, a manufactured housing retailer with 11 locations across Arizona, California, Colorado, New Mexico, and Oregon. Homes Direct carries approximately $70M in annualized revenue and brings Champion’s company-owned retail store count to 95. The deal is expected to close in Q2 FY2027 and is not included in Q1 guidance.

Looking into Q1 FY2027, management guided for revenue approximately flat versus the prior year. Adjusted gross margin is expected to come in at 24.5% to 25.5%, below Q4’s 25.7%, as input cost inflation across forest products, steel, and petroleum continues to outpace the company’s efficiency and pricing offsets. David McKinstray, EVP and CFO, stated on the Q4 earnings call that “the actions we’re taking to offset [inflation], whether it be through efficiency or value or mix, are lagging the rate of inflation that we’re seeing.”

Manufacturing backlog ended Q4 at $316M, up $50M or approximately 19% sequentially, with average lead time at 8 weeks. Manufacturing orders increased 7% year-over-year in Q4.

TIKR’s $102 Target on SKY Stock Requires Inflation to Behave and Retail Integration to Deliver

TIKR’s valuation model prices Champion Homes stock at a mid-case target of $102, against a current price of $72, implying a total return of 42.2% over the next 6 years at an annualized rate of 7.5% per year.

If Champion Homes works through its near-term margin compression and the business returns to normalized profitability, TIKR’s mid-case scenario points to a stock price of $117.29 by March 2035, with a total return of 63.4% and an IRR of 5.7%. That outcome requires inflation in forest products, steel, and petroleum to moderate, and the operational efficiency initiatives management referenced to close the lag on input cost pressures.

If the macro environment stays difficult and volume growth stalls, the low-case scenario produces a stock price of $94.03, a total return of 31%, and an IRR of 3.1%. In that world, Champion Homes stock still trades higher than today, but the annualized return is thin compensation for the operating risk of sustained margin pressure on a housing-sensitive business managing through cost inflation and a cautious consumer.

If inflation moderates faster than expected and the Homes Direct integration replicates the Iseman playbook, the high case produces a stock price of $142.28, a total return of 98.2%, and an IRR of 8%.

The catalyst there is not just volume: it is captive retail mix continuing to rise from 37% of consolidated sales toward a higher share, combined with the West Coast plant network feeding more production into Homes Direct locations as other brands are phased out.

Should You Invest in Champion Homes, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Champion Homes, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Champion Homes, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SKY stock on TIKR for Free →