Key Takeaways:

- MEDP stock has fallen around 25% year to date and sits roughly 32% below its 52-week high of $629, trading near $428.

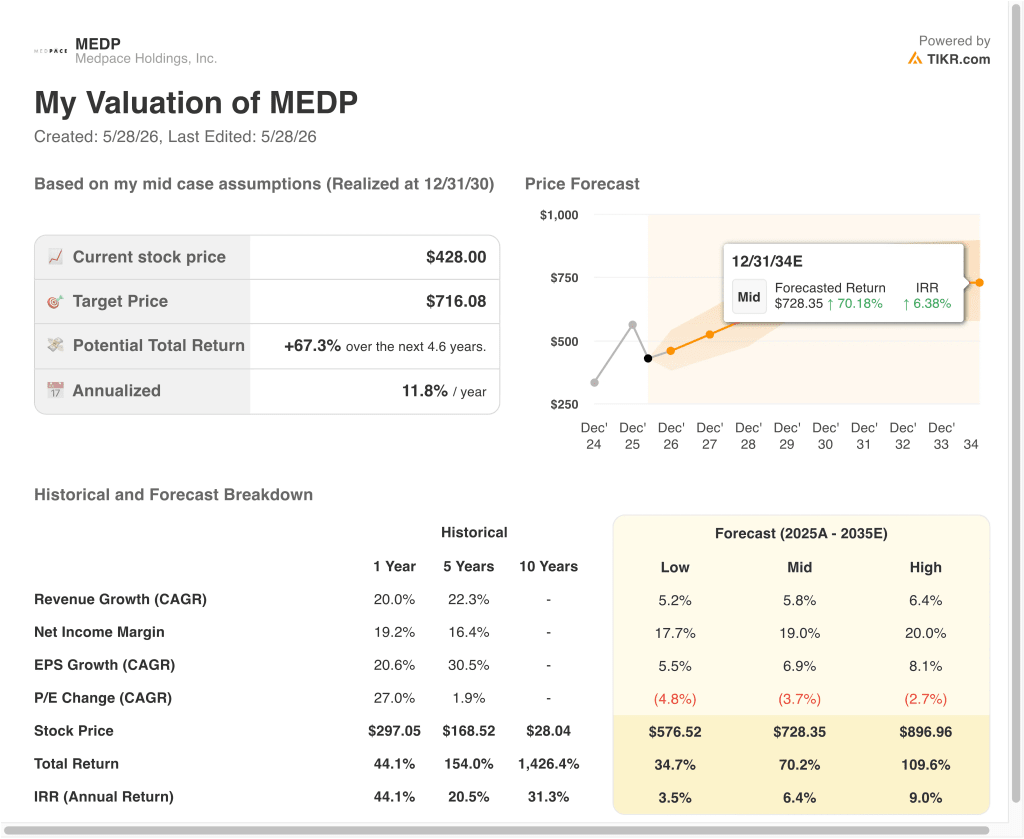

- Our model projects Medpace stock could reach around $557 per share by late 2028, a 30% total return and roughly 11% annualized.

- Medpace beat Q1 2026 revenue estimates and raised full-year 2026 revenue guidance to $2.755 billion to $2.855 billion, implying growth of around 9% to 13%.

What Happened?

Medpace Holdings, Inc. (MEDP) has faced significant selling pressure in 2026. The stock fell from a 52-week high of $629 to near $428 today, a decline of around 32%. Much of this pressure came from investor concern that artificial intelligence could disrupt the contract research organization (CRO) industry. CROs like Medpace manage and execute clinical drug trials on behalf of pharmaceutical and biotech companies that outsource this work rather than building the capability in-house.

Reuters reported in March 2026 that the AI-driven CRO selloff may overstate the disruption risk to these businesses. Medpace’s recent results supported that view. Q1 2026 revenue came in at $706.6 million, beating the analyst consensus estimate of $697.7 million. GAAP net income also rose 8.1% to $123.9 million, reflecting solid operational execution.

Management set 2026 full-year revenue guidance of $2.755 billion to $2.855 billion, implying year-over-year growth of around 8.9% to 12.8%. This range suggests the core business remains healthy and that demand from pharma and biotech clients has not slowed materially. Q4 2025 revenue of $708.45 million also beat the $689.4 million consensus estimate, continuing a pattern of strong results.

On governance, Medpace shareholders removed supermajority voting requirements at the May 2026 annual meeting to improve governance. Medpace’s integrated model, covering regulatory strategy, bioanalytical labs, and data management, gives it a differentiated CRO position.

Here’s why Medpace stock could offer solid capital returns through 2028 as its core business drivers support shareholder value.

What the Model Says for MEDP Stock

We analyzed the upside potential for Medpace stock based on its integrated full-service CRO model, consistent pattern of quarterly revenue beats, and a profitable operating structure that benefits from therapeutic focus and strong client retention.

Based on estimates of 8% annual revenue growth, 21% operating margins, and a normalized P/E multiple of 25x, the model projects Medpace stock could rise from $428 to $557 per share.

That would be a 30% total return, or an 11% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for MEDP stock:

1. Revenue Growth: 8.2%

Medpace has delivered a one-year revenue CAGR of 20.0% and a five-year CAGR of 22.3%, reflecting years of consistent contract wins and strong client retention within its therapeutically focused CRO model. The company’s 2026 full-year guidance implies growth of roughly 9% to 13%, which is a step down from recent historical rates but still represents healthy momentum for a business of this scale. Near-term growth may face some pressure as overall CRO demand adjusts to changing biotech funding dynamics.

Medpace’s differentiated, therapeutically specialized approach has helped it win contracts that more generalist CROs may struggle to secure. The company focuses on complex therapeutic areas like oncology, rare disease, and metabolic disorders, where deep scientific expertise matters. The forward two-year revenue CAGR consensus estimate stands at around 7.1%, reflecting modest deceleration from the high-growth period.

Based on analysts’ consensus estimates, we used an 8.2% revenue growth assumption for MEDP. This reflects the 2026 guidance midpoint and accounts for both the healthy pipeline of clinical trials and near-term uncertainty around biotech funding conditions and the evolving role of AI tools in clinical research operations.

2. Operating Margins: 21.4%

Medpace’s last-twelve-month EBIT margin stands at 21.0%, and its gross margin is 71.9%. These margins are strong for a CRO and reflect the benefits of the integrated model, where a single organization manages the entire clinical trial process from start to finish. Integration reduces handoff costs and improves execution quality, which in turn supports pricing power with clients.

Medpace’s return on invested capital (ROIC) stands at 75.2%, indicating exceptional capital efficiency that is unusual even among high-quality CRO peers. The company’s consistent profitability and strong cash generation have allowed it to return capital through share repurchases. Continued margin discipline as the company scales operations will be key to sustaining this performance.

Based on analysts’ consensus estimates, we used a 21.4% operating margin assumption for MEDP. This is consistent with the company’s recent historical margin level and reflects the ongoing benefits of scale and operational efficiency within Medpace’s integrated clinical research model.

3. Exit P/E Multiple: 24.5x

MEDP currently trades at a forward NTM P/E of around 24.5x. This multiple reflects Medpace’s above-average growth profile and differentiated positioning within the CRO industry, but it has compressed from higher levels seen before the AI-driven sector selloff began. The stock does not pay a dividend, so investors depend entirely on price appreciation for total return.

CRO companies with strong recurring revenue characteristics and consistent earnings growth can justify elevated P/E multiples relative to more cyclical healthcare businesses. However, if investor sentiment toward CROs continues to be weighed down by AI disruption fears, multiple compressions could persist. A reversal of that sentiment, combined with continued strong results, could support a meaningful re-rating.

Based on analysts’ consensus estimates, we used a 24.5x exit P/E multiple for MEDP. This reflects the current forward P/E and assumes a stable valuation for a high-quality CRO that consistently delivers above-industry revenue growth and strong margin performance within its integrated model.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for MEDP stock through 2030 show varied outcomes based on clinical trial demand and the resolution of AI disruption concerns for the CRO industry (these are estimates, not guaranteed returns):

- Low Case: Biotech funding slows, and AI tools reduce contract research volumes → 3.5% annual returns

- Mid Case: Steady clinical trial demand sustains revenue growth and margins hold → 6.4% annual returns

- High Case: AI integration enhances CRO efficiency, and Medpace accelerates market share gains → 9.0% annual returns

Going forward, Medpace’s near-term guided model implies an 11% annualized return potential that places the stock in a range many investors find attractive, though the longer-term scenario analysis points to more moderate outcomes.

The stock’s 32% pullback from its 52-week high has reset valuation to more reasonable levels relative to the company’s growth history. Investors should weigh the strength of Medpace’s differentiated CRO model against ongoing uncertainty around AI disruption narratives and biotech funding trends.

See what analysts think about MEDP stock right now (Free with TIKR) >>>

Should You Invest in Medpace?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MEDP, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track MEDP alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!