Key Takeaways:

- BDX stock has declined around 30% from its 52-week high of $213, trading near $147 today.

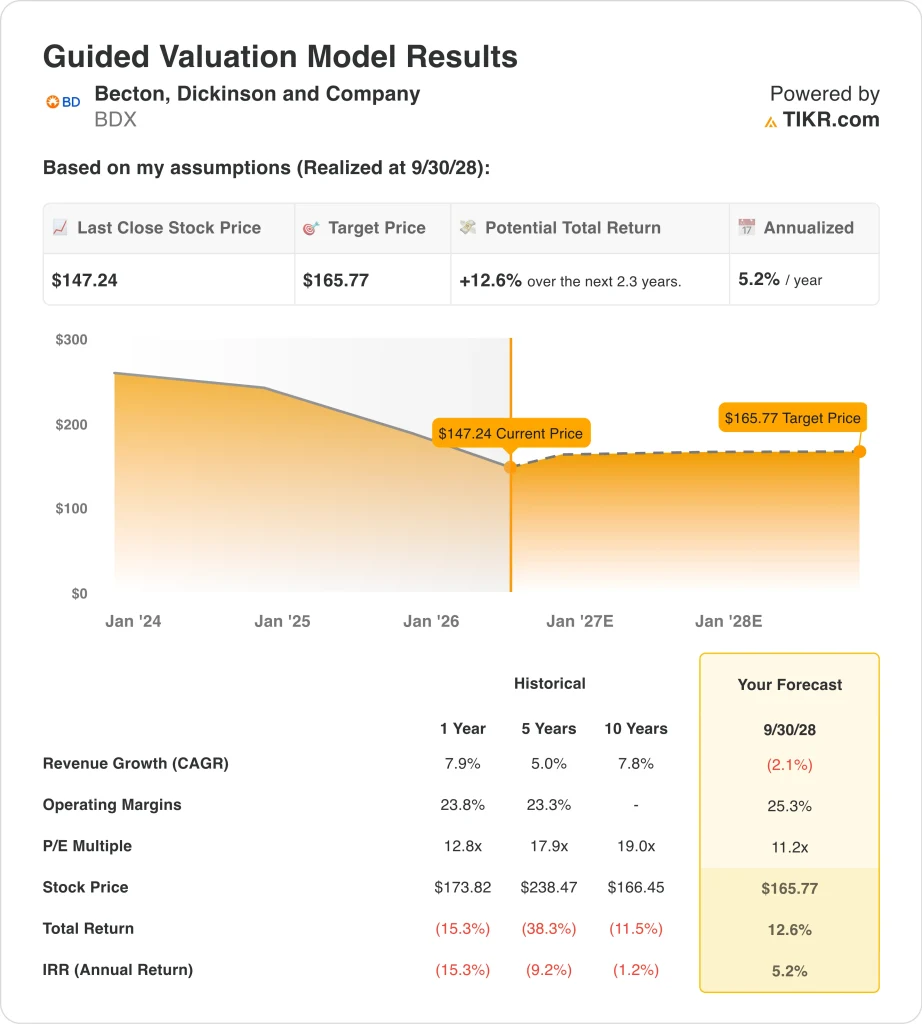

- Our model projects Becton Dickinson stock could reach around $166 per share by late 2028, a 13% total return and roughly 5% annualized.

- Q2 fiscal 2026 adjusted EPS of $2.90 beat the $2.77 consensus estimate, and BD raised its full-year 2026 profit forecast on strong drug delivery device demand.

What Happened?

Becton, Dickinson and Company (BDX) has experienced a sharp pullback from its 52-week high. The stock fell from around $213 to near $147 today, a decline of roughly 30% over the past several months. Investors have been cautious about near-term revenue trends as the company completes a major portfolio restructuring. But recent earnings results suggest the underlying business may be stabilizing.

Q2 fiscal 2026 results beat expectations on both earnings and revenue. BD reported adjusted EPS of $2.90, ahead of the $2.77 consensus estimate. Revenue climbed 5.2% to $4.71 billion, driven by strong demand for drug delivery devices. BD also raised its full-year 2026 profit forecast on the strength of that demand, which lifted investor sentiment.

The company has been actively reshaping its portfolio. Waters Corporation completed its combination with BD’s Biosciences and Diagnostic Solutions businesses in February 2026, allowing BD to focus on its core medical device and drug delivery segments. BD confirmed Vitor Roque as its permanent CFO and named Peter Menziuso as EVP and President of BD Interventional. These leadership moves signal a commitment to executing the refocused strategy.

On the capital markets side, BD’s finance subsidiary priced EUR 600 million in 3.855% notes due 2033 in May 2026. This debt issuance helps fund BD’s ongoing operational needs as it integrates its new structure. Here’s why Becton Dickinson stock could offer solid capital returns through 2028 as its core business drivers support shareholder value.

What the Model Says for BDX Stock

We analyzed the upside potential for Becton Dickinson stock based on its refocused drug delivery and interventional device platform, improving profitability post-divestiture, and a consistent dividend that adds to total shareholder return.

Based on estimates of around (2%) annual revenue growth reflecting the Biosciences divestiture impact, 25% operating margins, and a normalized P/E multiple of 11x, the model projects Becton Dickinson stock could rise from $147 to $166 per share.

That would be a 13% total return, or a 5% annualized return over the next 2.3 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for BDX stock:

1. Revenue Growth: -2.1%

The Waters and BD Biosciences combination closed in February 2026, removing a meaningful revenue segment from BD’s reported top line. This divestiture is the primary reason near-term reported revenue growth is projected to be negative. However, BD’s remaining core portfolio, focused on drug delivery devices and interventional products, is growing.

BD’s core drug delivery business delivered 5.2% revenue growth in fiscal Q2, according to Reuters. The near-term revenue headwind from the divestiture should ease as the new business structure matures and the remaining segments grow. The forward two-year revenue CAGR consensus estimate stands at around (5%), reflecting the full accounting impact of the portfolio change.

Based on analysts’ consensus estimates, we used a (2.1%) revenue growth assumption for BDX. This reflects the near-term impact of the divestiture on reported revenues, balanced against underlying growth in BD’s retained drug delivery and device businesses.

2. Operating Margins: 25.3%

BD’s last-twelve-month EBIT margin stands at 16.6%, and its gross margin is 47.1%. These margins are somewhat below many healthcare peers because BD’s product mix includes lower-margin device categories alongside its pharmaceutical delivery systems. However, the portfolio simplification from the Biosciences divestiture is expected to improve margin quality over time.

Management raised its full-year 2026 profit forecast after Q2 results, signaling that margin recovery is already underway. Higher drug delivery device volumes are also providing positive operating leverage. The removal of lower-margin businesses from the portfolio should benefit the company’s overall profitability going forward.

Based on analysts’ consensus estimates, we used a 25.3% operating margin assumption for BDX. This reflects the expected margin improvement as BD concentrates its portfolio on higher-value segments and benefits from scale in its core drug delivery and interventional device businesses.

3. Exit P/E Multiple: 11.2x

BDX currently trades at a forward NTM P/E of around 11x, which is low compared to many medical device peers. The significant decline from the 52-week high of $213 to near $147 has compressed the valuation multiple toward historic lows. A 2.6% dividend yield adds a meaningful income component to total return, which matters for investors evaluating the stock’s overall attractiveness.

Medical device companies with diverse portfolios and stable recurring revenue typically trade at forward P/E multiples of 12x to 22x. BD’s current low multiple reflects the uncertainty around the divestiture’s revenue impact and the near-term earnings transition. However, the raised profit guidance suggests that an earnings recovery may already be underway.

Based on analysts’ consensus estimates, we used an 11.2x exit P/E multiple for BDX. This is consistent with the current depressed valuation and accounts for the modest recovery expected as the refocused portfolio drives improved earnings quality over the coming years.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for BDX stock through 2030 show varied outcomes based on drug delivery device demand and operating margin recovery pace (these are estimates, not guaranteed returns):

- Low Case: Revenue remains pressured, and margins recover more slowly than expected → 3.5% annual returns

- Mid Case: Drug delivery demand sustains, and margins improve as planned → 5.6% annual returns

- High Case: Portfolio refocus accelerates profitability and device revenue rebounds → 7.4% annual returns

Going forward, BDX’s return profile is modest across all three scenarios, reflecting the near-term revenue headwinds from the Biosciences divestiture and a muted forward growth outlook. The stock’s sharp pullback from $213 to near $147 has created some valuation support, and the raised profit forecast suggests fundamentals are improving.

But investors should weigh the limited upside implied by the model against the company’s stable dividend, strong drug delivery device franchise, and long-term healthcare exposure.

See what analysts think about BDX stock right now (Free with TIKR) >>>

Should You Invest in Becton Dickinson?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up BDX, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track BDX alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!