Key Takeaways:

- Marathon Petroleum’s Q1 2026 adjusted EPS of $1.65 more than doubled the IBES estimate of $0.75, driven by wider refining margins tied to Middle East geopolitical tensions.

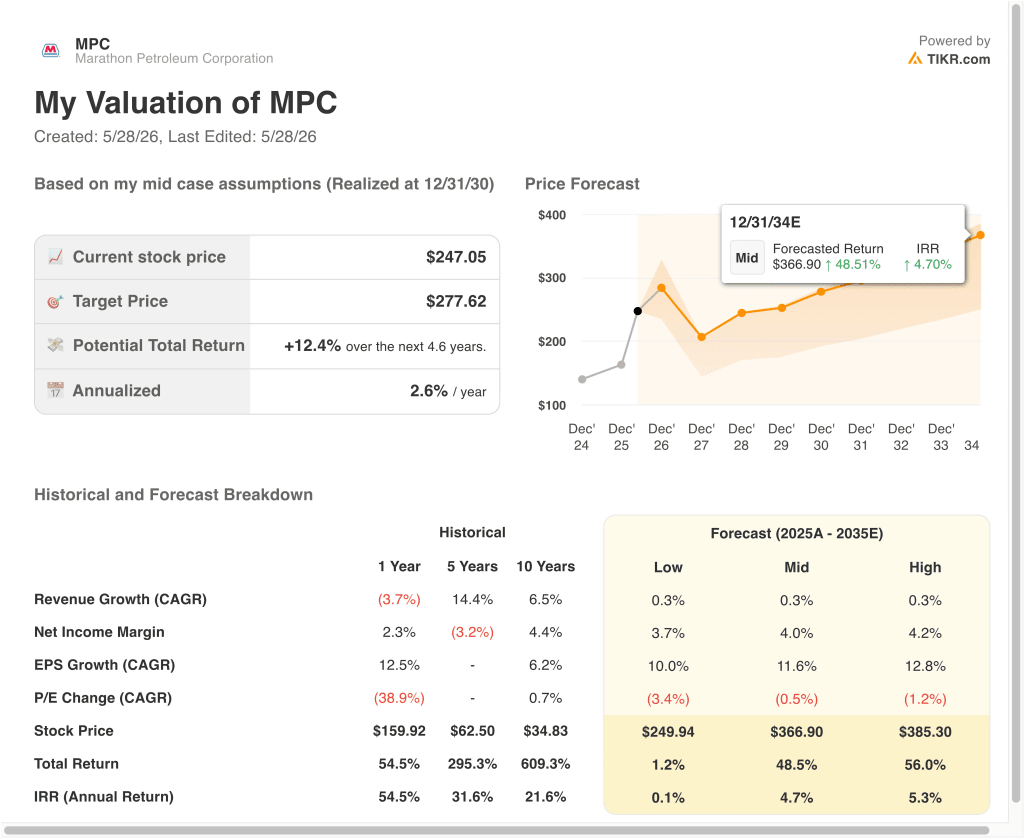

- MPC stock could rise from $247 to around $272 per share by December 2028, based on our valuation assumptions.

- That implies a total return of around 10% and an annualized return of around 4% over the next 2.6 years.

What Happened?

Marathon Petroleum Corporation (MPC) delivered a standout first quarter in fiscal 2026. Adjusted EPS of $1.65 more than doubled the Street estimate of $0.75. Net income reached $511 million, returning the company to solid profitability. Investors reacted positively and pushed shares higher after the results.

The key driver behind the beat was a sharp rise in refining margins. Conflict in Iran boosted crude oil prices and widened crack spreads, which represent the gap between crude input costs and refined product prices. Marathon operates one of the largest refining networks in the United States, so this environment directly benefited the business. Scale gave the company a strong advantage during the disruption.

Looking ahead, oil price movements tied to Iran negotiations remain the central variable. Marathon entered a new $5 billion revolving credit facility in April 2026, boosting financial flexibility. The company also filed a mixed shelf offering in May 2026, signaling potential capital market activity. These moves give management room to navigate a volatile energy environment.

Analysts hold a consensus target of around $262. The 52-week range runs from $156 to $264, reflecting the cyclical nature of refining. The stock has gained around 51% year to date. Here’s why Marathon Petroleum stock could offer solid capital returns through 2028 as its core business drivers support shareholder value.

What the Model Says for MPC Stock

We analyzed the upside potential for Marathon Petroleum stock based on its near-term refining margin recovery, steady throughput across its U.S. refinery network, and disciplined capital allocation through buybacks and dividends.

Based on estimates of 2% annual revenue growth, 7.7% operating margins, and a normalized P/E multiple of 10.0x, the model projects Marathon Petroleum stock could rise from $247 to around $272 per share.

That would be a 9.9% total return, or a 3.7% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for MPC stock:

1. Revenue Growth: 2%

Marathon Petroleum is one of the largest independent refining and marketing companies in the United States. Revenue is highly sensitive to crude oil prices, crack spreads, and refinery throughput rates. The one-year revenue declined 3.7%, but the five-year CAGR of 14.4% reflects the extraordinary margin environment of recent years.

Refining revenue tracks commodity cycles closely, so growth assumptions are more modest than growth-oriented sectors. The forward two-year consensus revenue CAGR of just 0.7% reflects an expectation that the Iran-driven margin spike is temporary.

Based on analysts’ consensus estimates, we used 2% annual revenue growth. This reflects steady throughput capacity, partially offset by normalizing refining margins as geopolitical uncertainty gradually eases.

2. Operating Margins: 7.7%

Marathon’s LTM EBIT margin stands at 5.1%, reflecting the inherently thin margin structure of refining. However, Q1 2026 demonstrated the operating leverage this business carries when conditions align. Margins can swing sharply based on regional supply and demand dynamics.

The company also benefits from its MPLX midstream affiliate, which provides stable, fee-based cash flows. These midstream earnings help cushion volatility in the core refining segment.

Based on analysts’ consensus estimates, we used 7.7% operating margins. This reflects a normalization toward mid-cycle levels while including a steady contribution from MPLX’s fee-based operations.

3. Exit P/E Multiple: 10x

Marathon Petroleum trades at an NTM P/E of around 8.5x and an LTM P/E of around 16x. The forward multiple compression reflects expected earnings normalization as refining margins moderate. Refining stocks historically trade at lower multiples because of their cyclical earnings profile.

A 10.0x exit P/E reflects the cyclical nature of the business and accounts for some earnings recovery above the current environment. This is consistent with the historical trading range for large independent refiners.

Based on analysts’ consensus estimates, we used a 10.0x exit multiple. This accounts for potential margin normalization, ongoing capital returns through buybacks, the 1.7% dividend yield, and the stabilizing contribution from MPLX.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for MPC stock through 2030 show varied outcomes based on refining margin trends and midstream distribution growth (these are estimates, not guaranteed returns):

- Low Case: Refining margins normalize sharply and revenue growth stalls near zero → 0.1% annual returns

- Mid Case: Margins stabilize at mid-cycle levels with steady MPLX distributions supporting earnings → 4.7% annual returns

- High Case: Prolonged geopolitical disruption sustains elevated crack spreads above consensus → 5.3% annual returns

consensus → 5.3% annual returns

Going forward, Marathon Petroleum’s returns are tightly linked to crude oil prices and the trajectory of Middle East tensions. The company’s refinery scale and midstream exposure provide a floor, but the upside depends on variables outside management’s control. Investors weighing a position should monitor Iran-related oil supply developments as a primary leading indicator.

See what analysts think about MPC stock right now (Free with TIKR) >>>

Should You Invest in Marathon Petroleum Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MPC, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track MPC alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!