Key Stats for Bank of Nova Scotia Stock

- Current Price: ~CA$112 (May 27, 2026)

- Q2 FY26 Revenue: CA$9.84B, +8.3% YoY

- Q2 FY26 Adjusted EPS: CA$2.02, +32.9% YoY

- Q2 FY26 Net Income: CA$2.49B, +31.1% YoY

- Q2 FY26 EBIT Margin: 47.5% (vs. 44.4% prior year)

- CET1 Ratio: 13.3%

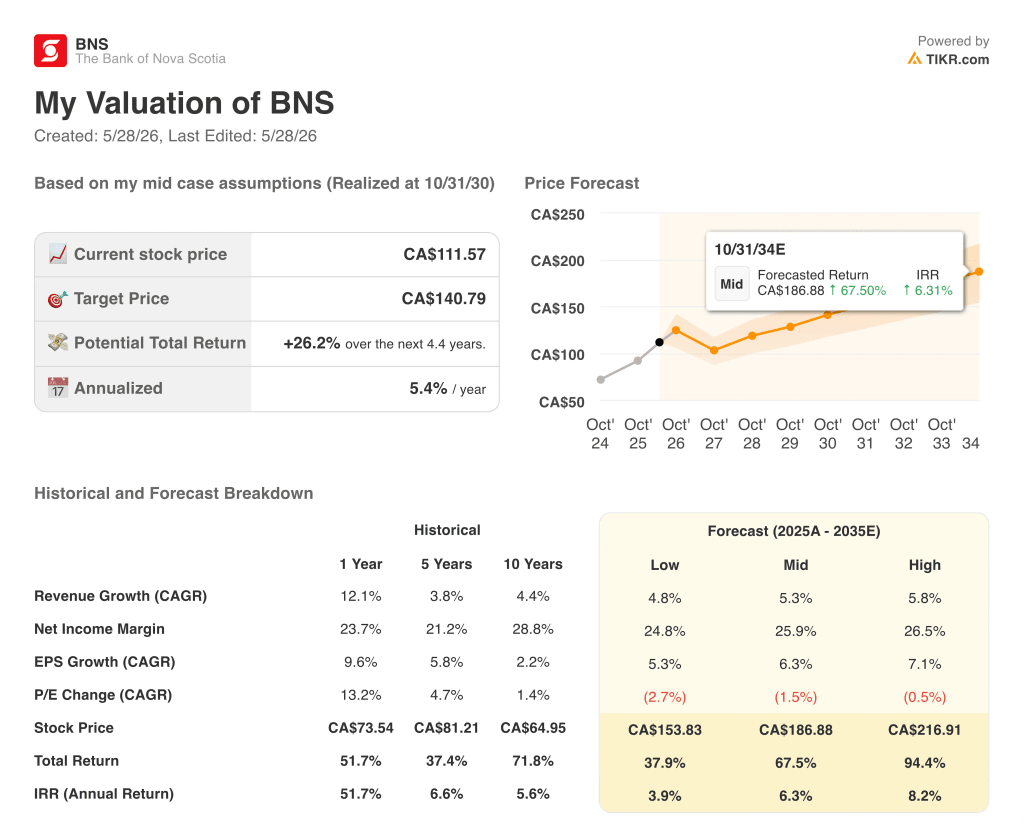

- TIKR Model Price Target: CA$141

- Implied Upside: ~26%

BNS Stock Posts a Clean Q2 Beat as Capital Returns and Margin Expansion Redefine the Thesis

The Bank of Nova Scotia (BNS) delivered adjusted EPS of CA$2.02 in Q2 2026, beating the CA$1.94 Street estimate by around 4% as pretax pre-provision earnings grew 16% year-over-year across a business that is quietly re-rating.

Revenue reached CA$9.84 billion, topping the CA$9.73 billion consensus estimate by just over 1% and accelerating 8% from CA$9.08 billion in the same quarter last year.

Canadian Banking was the most important engine this quarter, posting pretax pre-provision earnings growth of 13% year-over-year as four consecutive quarters of net interest margin expansion and record mutual fund sales drove the operating leverage story.

CEO Scott Thomson stated on the Q2 2026 earnings call that “pretax pre-provision earnings were up 16% year-over-year as we continue to drive revenue growth and manage our expenses effectively,” anchoring guidance for a return on equity above 14% in fiscal 2027, one year ahead of the original Investor Day target.

Global Wealth Management delivered earnings of CA$474 million, up 19% year-over-year, with net sales of CA$4.7 billion representing 4x the figure from Q2 2025 and marking the seventh consecutive quarter of positive net flows.

International Banking produced pretax pre-provision earnings growth of 12% year-over-year at constant currency, with Mexico leading the segment at 8% revenue growth and 25% earnings growth.

The bank repurchased 6.4 million shares in the quarter under its 2026 program and announced a CA$0.04 quarterly dividend increase, bringing total capital returned to shareholders over the past 12 months to CA$7.5 billion through buybacks and dividends.

Credit quality remains the primary risk: total provisions for credit losses were CA$1.2 billion or 66 basis points, with a single corporate account in Brazil’s International Banking segment accounting for approximately 7 basis points of the bank-wide impaired PCL ratio.

Management now guides for impaired PCLs to settle in the mid-50 basis points range for the remainder of 2026, a more gradual decline than previously anticipated, reflecting persistent inflationary pressures on Canadian retail borrowers and lingering macro uncertainty across Latin America.

Is BNS Stock Undervalued in 2026? TIKR’s CA$141 Target Points to Around 26% Upside

TIKR’s base case values BNS stock at approximately CA$141 by October 2030, implying around 26% total return from the current price of CA$112, or roughly 5% annualized over around 4 years.

If BNS sustains around 5% revenue growth and around 26% net income margins — consistent with the trajectory the Q2 result supports — the mid-case holds and the stock reaches near CA$141 on an annualized return of roughly 5%.

Should PCL pressures persist beyond 2026 and the ROE improvement toward 14% stall, the low case produces a stock price near CA$154 by October 2034 at around 4% annualized — still positive, but meaningfully below the base.

If Canada’s macro outlook improves faster than expected and wealth management and International Banking accelerate beyond current consensus, the high case puts BNS near CA$217 at around 8% annualized, a 94% total return over the full period.

How did Bank of Nova Scotia perform in Q2 2026 earnings?

BNS delivered adjusted EPS of CA$2.02 in Q2 2026, beating the CA$1.94 Street estimate by around 4%. Revenue reached CA$9.84 billion, 8% above the CA$9.08 billion reported in Q2 2025, while pretax pre-provision earnings grew 16% year-over-year.

Canadian Banking earnings surged 53% year-over-year on NIM expansion and lower provisions, with the overall PCL ratio coming in at 66 basis points.

The bank also raised its quarterly dividend by CA$0.04, signaling management confidence in the earnings trajectory.

Should You Invest in The Bank of Nova Scotia?

You can build a free watchlist to track The Bank of Nova Scotia alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up The Bank of Nova Scotia stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

Access Professional Tools to Analyze BNS stock on TIKR for Free →