Key Takeaways:

- Zillow Group reported Q1 2026 revenue of $708 million, up 18% year over year, with net income rising to $46 million on AI integration gains.

- ZG stock could potentially reach around $43 per share by December 2028, based on our near-term valuation assumptions.

- This implies a total return of around 17% from today’s price of $36, with an annualized return of 6.3% over the next 2.6 years.

What Happened?

Zillow Group (ZG) reported Q1 2026 revenue of $708 million, up 18% year over year, with net income reaching $46 million. AI integration was highlighted as a key driver of engagement and conversion improvements across the platform.

The company reaffirmed its full-year revenue outlook and mid-cycle financial targets at a special investor call in March 2026. Investors were broadly encouraged by the Q1 beat, but the stock has faced significant pressure throughout the year.

A major data disruption emerged in May 2026 when the Midwest Real Estate Data (MRED) cooperative suspended its listing feeds to Zillow and Trulia. This cut off access to Chicago-area property listings, one of the largest housing markets in the US.

A federal judge ordered MRED to restore Zillow’s access just days later, on May 23, 2026. The episode exposed ongoing tensions between Zillow and regional listing cooperatives, but resolved quickly.

Zillow and Redfin failed to dismiss an FTC lawsuit in May 2026, with the agency claiming they suppressed rental market competition. Higher mortgage rates continued to slow the US home sales rebound through April and May 2026.

Rental concessions hit a record spring high in May, with 39.8% of listings offering incentives to attract tenants. Investors are broadly rethinking the ZG setup, balancing strong revenue growth against regulatory risks and housing affordability headwinds.

Here’s why Zillow stock could offer solid capital returns through 2028 as its core business drivers support shareholder value.

What the Model Says for ZG Stock

We analyzed the upside potential for Zillow stock using valuation assumptions based on its dominant real estate marketplace position, expanding AI capabilities across search and mortgage, and growing rental and agent tools businesses.

Based on estimates of 15.5% annual revenue growth, 11.8% operating margins, and a normalized P/E multiple of 14.7x, the model projects Zillow stock could rise from $36 to around $43 per share.

That would be a 17.3% total return, or a 6.3% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ZG stock:

1. Revenue Growth: 15.5%

Zillow Group operates the leading online real estate marketplace in the United States through its Zillow and Trulia platforms. Revenue comes from residential advertising, rental listings, mortgage origination, and software-as-a-service (SaaS) tools for real estate agents and professionals. The company has been investing heavily in AI to improve search quality, lead matching, and transaction completion rates.

Q1 2026 revenue of $708 million grew 18% year over year, driven by improved agent engagement and AI-powered product upgrades. Zillow also extended its Preview listings collaboration with Realtor.com in May 2026, which could draw additional listing inventory and consumer traffic. These initiatives support continued revenue momentum even in a rate-challenged housing environment.

Based on analysts’ consensus estimates, we used a 15.5% revenue growth rate for Zillow stock. This reflects the company’s expanding product suite, AI-driven engagement improvements, and a gradual housing market recovery. The forward two-year revenue CAGR consensus of around 14% provides support for this estimate.

2. Operating Margins: 11.8%

Zillow reported an LTM EBIT margin of 0.5%, which is near breakeven, but the LTM gross margin of 73.3% confirms that the underlying business model is highly scalable. Operating expenses in technology, marketing, and product development have kept EBIT minimal while the company reinvests for growth. High gross margins indicate that additional revenue can flow efficiently to operating income as scale increases.

Q1 2026 net income of $46 million shows that profitability is building as revenue grows. AI investments are intended to drive operating leverage by reducing manual processes and improving conversion rates without proportional cost increases. This dynamic supports the view that margins can expand materially from near-breakeven levels as the platform matures.

Based on analysts’ consensus estimates, we used an 11.8% operating margin assumption for Zillow stock. This implies significant improvement from today’s near-zero EBIT level as revenue scales faster than costs. The high gross margin structure provides confidence that this level is achievable if the growth thesis holds.

3. Exit P/E Multiple: 14.7x

Zillow stock trades at an NTM P/E of around 14.7x, which is modest relative to the company’s expected revenue growth rate of around 15%. The LTM P/E of around 150x is distorted by minimal reported earnings at the current stage of the business, making the forward multiple more meaningful for valuation purposes. A 14.7x exit multiple implies investors are paying for earnings normalization but not a premium growth multiple.

The street consensus target price sits at around $65 per share, implying roughly 79% upside from the current price of $36. This significant gap reflects analysts’ view that the stock is materially undervalued if the growth thesis plays out over several years. Near-term regulatory risks and the MRED listing dispute have likely kept the multiple depressed below where it might otherwise trade.

Based on analysts’ consensus estimates, we used a 14.7x exit P/E multiple for Zillow stock. This reflects a normalized earnings multiple consistent with a marketplace business that is transitioning toward sustained profitability. Upside to the multiple is possible if AI capabilities drive faster-than-expected margin expansion.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

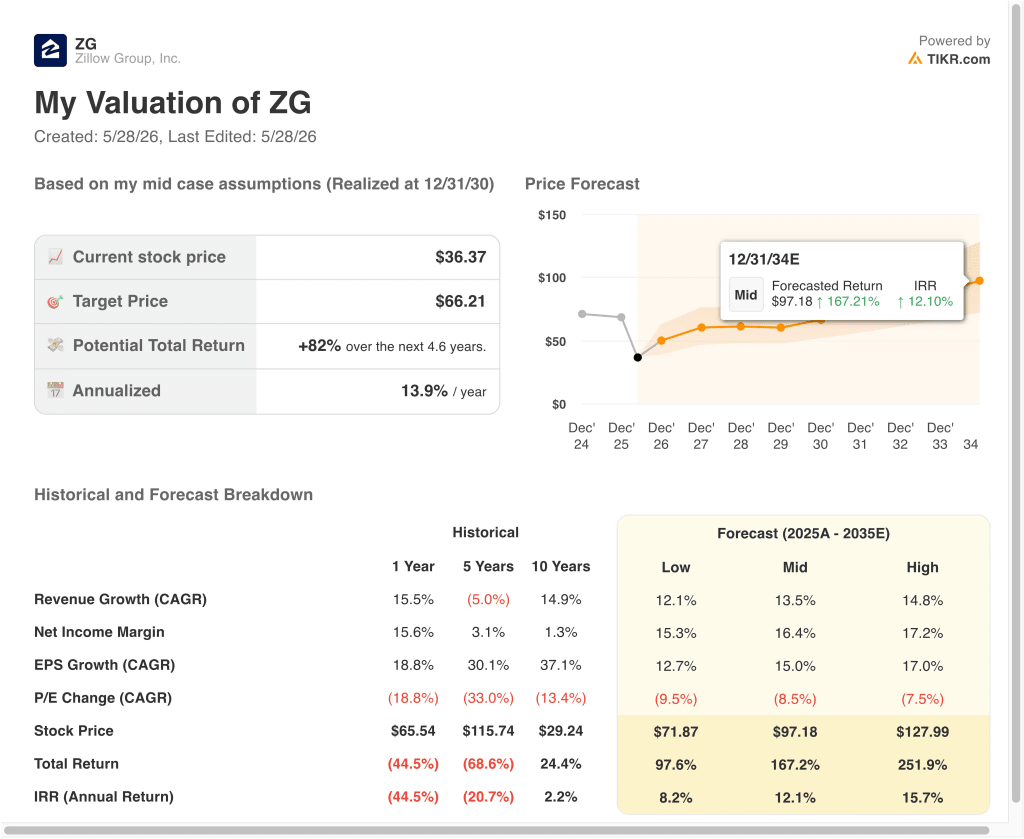

Different scenarios for ZG stock through 2034 show varied outcomes based on housing market recovery, AI revenue monetization, and operating margin expansion (these are estimates, not guaranteed returns):

- Low Case: Housing market recovery stalls and AI tools fail to drive meaningful revenue acceleration → 8.2% annual returns

- Mid Case: AI integration drives strong revenue growth, and margins expand toward 16% → 12.1% annual returns

- High Case: Full housing market recovery and rapid AI monetization across mortgage and agent tools → 15.7% annual returns

Going forward, the near-term 2028 model for Zillow projects 6.3% annualized returns, which falls below the 10% threshold many investors consider attractive for near-term positions. However, the longer-term 2034 mid-case projects around 12% annual returns, which crosses into territory many investors find compelling.

The stock’s ultimate trajectory will hinge on housing affordability trends, FTC lawsuit resolution, and Zillow’s success in converting AI investments into durable margin expansion.

See what analysts think about ZG stock right now (Free with TIKR) >>>

Should You Invest in Zillow Group?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ZG, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ZG alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!