Key Takeaways:

- CBRE Group reported Q1 2026 core EPS of $1.61, with revenue rising 19% to $10.5 billion, driven by data center demand.

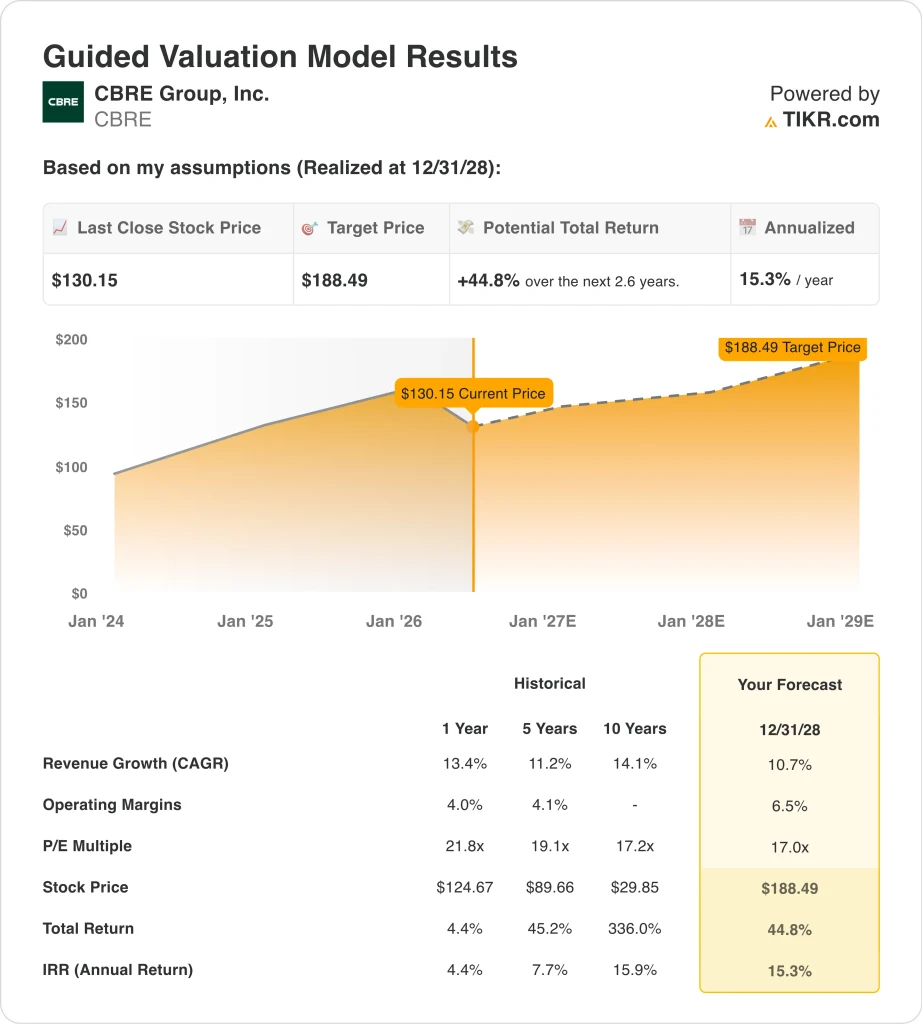

- CBRE stock could potentially reach around $188 per share by December 2028, based on our valuation assumptions.

- This implies a total return of around 45% from today’s price of $130, with an annualized return of 15.3% over the next 2.6 years.

What Happened?

CBRE Group (CBRE) posted Q1 2026 revenue of $10.5 billion, up 19% year over year, as data center demand fueled strong results across its services businesses. GAAP net income more than doubled in the quarter, while core EPS came in at $1.61. This result beat analyst expectations and marked one of the strongest revenue quarters in recent history. Investors responded positively, viewing data center exposure as a structural growth driver for CBRE’s platform.

CBRE Investment Management-backed Accelerate closed a $630 million primary capital raise in May 2026. Abu Dhabi sovereign wealth fund Mubadala also joined the Accelerate Infrastructure Opportunities platform alongside CBRE. These moves reflect growing institutional appetite for infrastructure-linked real estate assets. CBRE also issued $750 million in 5.25% senior notes due 2036, extending its debt maturity profile and funding future growth initiatives.

The company recast its financial reporting in March 2026, creating a Critical Infrastructure Services (CIS) segment that generated $1.7 billion in 2025 revenue. This new segment covers data centers, life sciences facilities, and advanced manufacturing work. J.P. Morgan cut its price target in April 2026, citing near-term caution around growth timing. Yet most investors appear excited about CBRE’s growing infrastructure exposure and the long-term data center buildout tailwind.

Here’s why CBRE stock could offer solid capital returns through 2028 as its core business drivers support shareholder value.

What the Model Says for CBRE Stock

We analyzed the upside potential for CBRE stock using valuation assumptions based on its leadership in commercial real estate services, expanding data center and infrastructure exposure, and growing assets under management across global markets.

Based on estimates of 10.7% annual revenue growth, 6.5% operating margins, and a normalized P/E multiple of 17.0x, the model projects CBRE stock could rise from $130 to around $188 per share.

That would be a 44.8% total return, or a 15.3% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CBRE stock:

1. Revenue Growth: 10.7%

CBRE Group is the world’s largest commercial real estate services and investment firm. Revenue comes from leasing advisory, property and facilities management, investment management, and the growing Critical Infrastructure Services segment. The company operates globally, making it a highly diversified real estate services platform with multiple income streams.

Q1 2026 revenue of $10.5 billion grew 19% year over year, driven by data center leasing and construction activity. The CIS segment alone generated $1.7 billion in 2025 and is positioned to grow rapidly as AI-driven data center investment accelerates. This segment formalizes what was already a major and fast-growing part of CBRE’s business mix.

Based on analysts’ consensus estimates, we used a 10.7% revenue growth rate for CBRE stock. This reflects strong secular demand from data center construction and leasing, combined with a recovery in broader commercial real estate transaction volumes. The forward two-year revenue CAGR consensus of around 12% supports this level.

2. Operating Margins: 6.5%

CBRE reported an LTM EBIT margin of 2.9% and an LTM gross margin of 18.5%. The EBIT margin appears modest because lower-margin facility management and property management contracts dilute the overall margin picture. Higher-margin advisory, investment management, and project management businesses are where most operating leverage is concentrated.

GAAP net income more than doubled in Q1 2026, driven by strong operating leverage and a favorable business mix from data center and infrastructure projects. The CIS segment carries better margins than traditional property management. This mix shift toward infrastructure is a key driver of projected margin improvement over the coming years.

Based on analysts’ consensus estimates, we used a 6.5% operating margin assumption for CBRE stock. This implies meaningful improvement from current reported levels as data center and advisory revenues grow faster than lower-margin service lines. The assumption reflects CBRE’s stated long-term margin expansion ambitions.

3. Exit P/E Multiple: 17x

CBRE stock currently trades at an NTM P/E of around 17x, which reflects both its earnings growth potential and the cyclical nature of commercial real estate. The LTM P/E of 29.7x is elevated because base earnings were compressed during the commercial real estate slowdown. A 17x exit multiple implies more normalized earnings power priced at a market-rate multiple for a real estate services leader.

The company’s LTM ROE of 15.6% and ROIC of 6.1% are supported by a large and growing investment management platform. ROE is expected to improve as higher-margin businesses scale and assets under management grow. A 17x multiple reflects reasonable confidence in CBRE’s long-term earnings trajectory without requiring an aggressive premium.

Based on analysts’ consensus estimates, we used a 17.0x exit P/E multiple for CBRE stock. This is consistent with the company’s NTM trading level and reflects the expectation of sustained earnings growth from infrastructure services. Some contraction from historical peak multiples is assumed, reflecting a more normalized commercial real estate environment.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

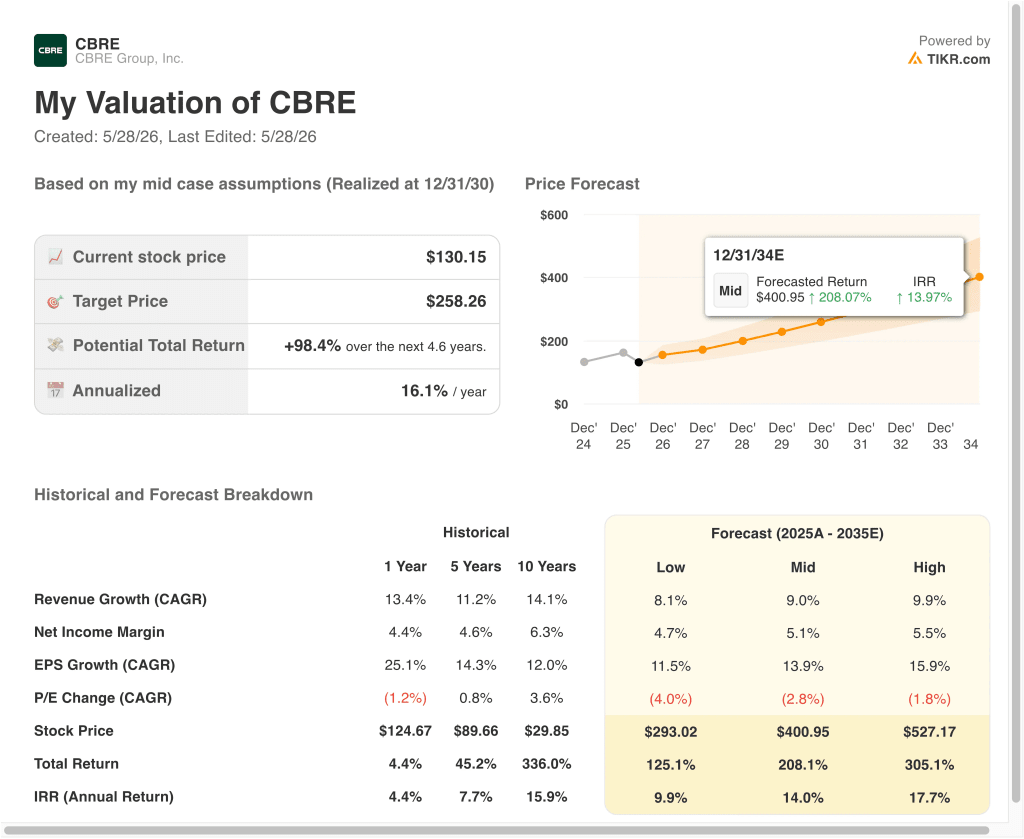

Different scenarios for CBRE stock through 2034 show varied outcomes based on data center leasing volumes, commercial real estate market recovery, and operating margin expansion (these are estimates, not guaranteed returns):

- Low Case: Data center growth moderates and commercial real estate recovery stalls → 9.9% annual returns

- Mid Case: Infrastructure services scale strongly, and advisory volumes continue recovering → 14.0% annual returns

- High Case: Rapid data center expansion and a full commercial real estate market recovery drive strong earnings → 17.7% annual returns

Going forward, CBRE stands out with mid-case long-term returns above 14% and even the low case clearing the 9.9% mark. The near-term 2028 model projects 15.3% annualized returns, which is at the high end of what investors typically consider attractive.

Key risks include a deceleration in data center construction spending and a prolonged commercial office and retail transaction market downturn.

See what analysts think about CBRE stock right now (Free with TIKR) >>>

Should You Invest in CBRE Group?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CBRE, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CBRE alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!