Key Stats for Dycom Industries Stock

- Current Price: ~$529 (May 27, 2026)

- Q1 FY2027 Total Revenue: $1.96B, +56% YoY

- Q1 FY2027 Adjusted Diluted EPS: $4.42, +142% YoY

- Q1 FY2027 Adjusted EBITDA: $262.5M, +75% YoY; margin of 13.4%

- Q1 FY2027 Total Backlog: $11.9B, +25% sequentially

- FY2027 Revenue Guidance (raised): $7.38B–$7.65B, ~38% growth at midpoint

- TIKR Model Price Target: ~$621

- Implied Upside: ~17%

Dycom Industries Stock Surges 26% as Fiber and Data Center Demand Hits a New Gear

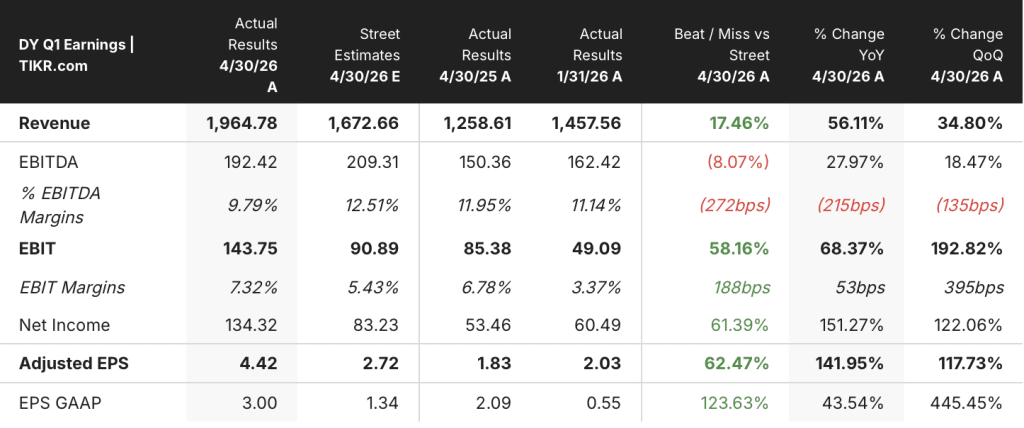

Dycom Industries (DY) delivered a historic Q1 FY2027 quarter on May 27, posting adjusted diluted EPS of $4.42 against a Street estimate of $2.72, a 62% beat, as total contract revenues of $1.96B surged 56% year-over-year.

The EPS beat traced directly to an acceleration in fiber-to-the-home volumes that outpaced even Dycom’s internal projections, with fiber-to-the-home revenue growing 33% in a single quarter.

The one number that makes the scale of the shift undeniable is the adjusted EBITDA margin: 13.4%, up 141 basis points year-over-year, on revenues that grew 56% — proof that Dycom is expanding faster than it is spending.

Daniel Peyovich, President and CEO, stated on the Q1 FY2027 earnings call that “fiber-to-the-home is starting to take place, just as we set up our strategy, and we believe that’s going to continue,” tying the organic acceleration to multiyear build programs ramping simultaneously across multiple customers and geographies.

Record total backlog of $11.9 billion, growing 25% sequentially with a book-to-bill of 2.2x, gives Dycom contracted revenue visibility that extends well past fiscal 2027, with management noting customers are extending contract durations to lock in skilled workforce capacity through the end of the decade.

Dycom also announced a definitive agreement to acquire National Technology Integrators (NTI), a Maryland-based low-voltage engineering and construction firm specializing in structured cabling and data center inside-plant work, for $275 million on a cash-free, debt-free basis, with an initial annual revenue run rate of approximately $175 million and adjusted EBITDA margins historically in the mid- to high-teens.

The NTI acquisition completes a vertically integrated digital infrastructure offering: Dycom’s Communications segment builds the long-haul and middle-mile fiber, Power Solutions handles inside-plant electrical work, and NTI connects the structured cabling at the rack level, enabling Dycom to serve a customer’s full fiber footprint from data center to home.

BEAD remains excluded from current guidance and represents incremental upside, with management expecting the first BEAD revenue in Q2 FY2027 and meaningful contribution beginning in calendar 2027, as state-level and subgrantee pipelines continue to advance.

Is Dycom Industries Stock Undervalued at $529? TIKR’s $621 Target and the Backlog That Argues Yes

TIKR’s base case values Dycom Industries stock at approximately $621 by January 2031, implying around 17% total return from the current price of $529, or roughly 3% to 4% annualized over approximately 5 years.

If Dycom sustains its organic revenue CAGR in the mid-range of TIKR’s 10.3% assumption and expands net income margin toward 7.8%, the mid-case price of approximately $803 by January 2035 implies a total return of around 52% and an IRR of roughly 5%.

A scenario where revenue growth decelerates to TIKR’s low case of 9.3% produces a stock price of approximately $610 by January 2035, a total return of around 15% and an annualized rate of roughly 2%.

Full capture of the fiber-to-the-home cycle, BEAD ramp, and long-haul middle-mile volume that management expects to accelerate in calendar 2028 could support TIKR’s high case of approximately $1,027, implying total return of around 94% and an annualized rate of roughly 8%.

The single variable that determines which scenario materializes is whether Dycom’s organic Communications revenue CAGR holds at or above 10% as fiber-to-the-home builds plateau and the BEAD and middle-mile cycles take over as primary growth drivers.

How Did Dycom Industries Perform in Q1 FY2027 Earnings?

Dycom Industries delivered adjusted EPS of $4.42, beating the $2.72 Street estimate by 62%, the largest reported EPS beat relative to consensus in the company’s recent history.

Revenue reached $1.96B, up 56% year-over-year, driven by 25% organic Communications growth and $395M in Building Systems revenue as Power Solutions ramped ahead of internal projections.

Adjusted EBITDA of $262.5M came in at a 13.4% margin, up 141 basis points year-over-year, confirming that scale is expanding faster than costs. Management raised full-year FY2027 revenue guidance to $7.38B–$7.65B and guided Q2 EPS of $4.40–$4.82.

Is Dycom Industries Stock a Buy Right Now?

TIKR’s base case values Dycom Industries stock at approximately $621 by January 2031, implying around 17% total return from the current price of $529, or roughly 3% to 4% annualized.

The record $11.9B backlog, 141 basis point EBITDA margin expansion, and a book-to-bill of 2.2x provide near-term earnings visibility that underpins the base case.

The key variable is whether the organic Communications CAGR sustains at or above 10% as the fiber-to-the-home cycle matures and BEAD and middle-mile volume assume the growth role.

Should You Invest in Dycom Industries, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Dycom Industries stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Dycom Industries alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DY stock on TIKR for Free →