Key Stats for DICK’S Sporting Goods Stock

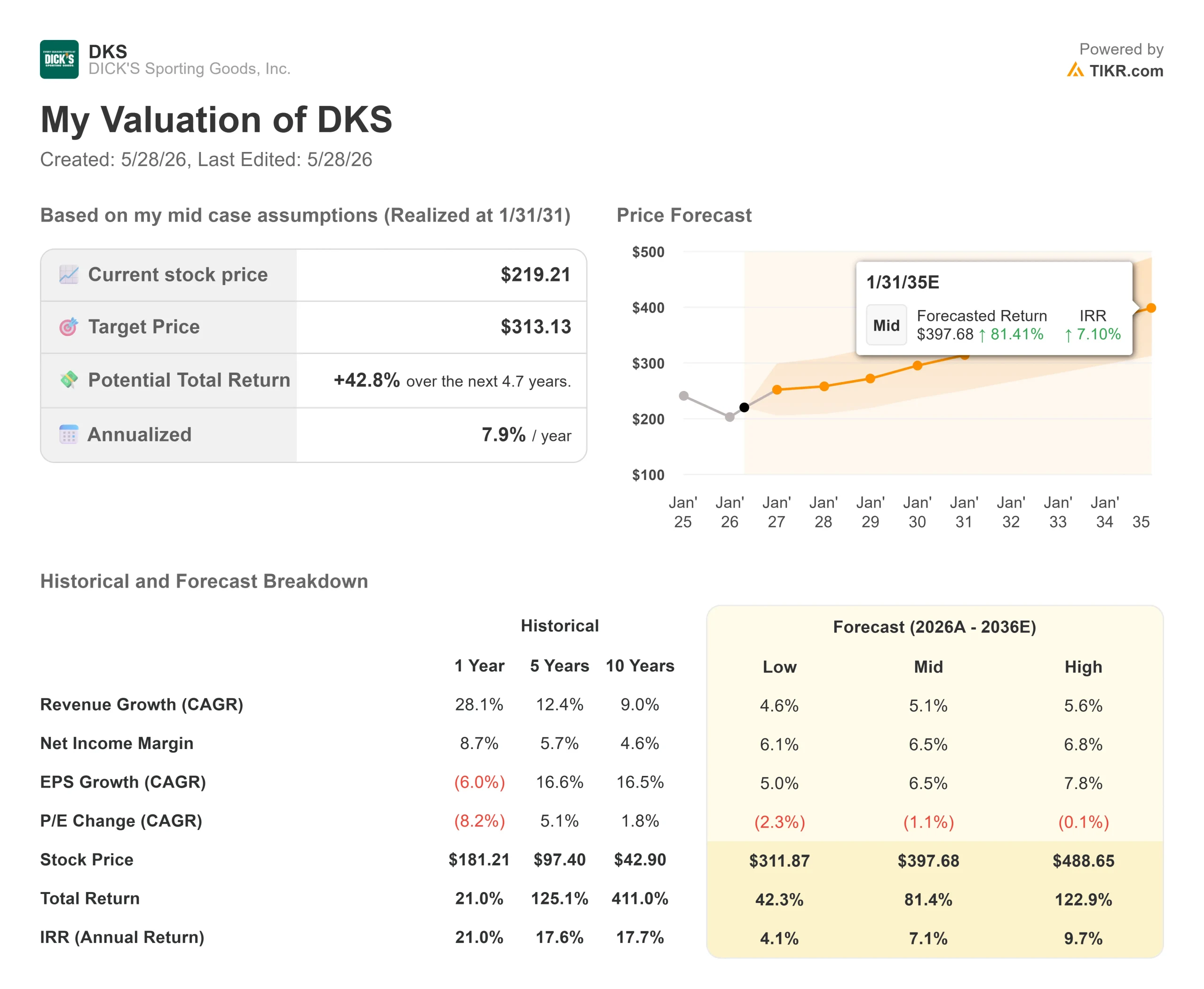

- Current Price: $219.21

- Target Price (Mid): ~$313

- Street Target: ~$240

- Potential Total Return: ~43%

- Annualized IRR: ~8% / year

- 1D Stock Reaction: -5.97% (May 27, 2026)

- Max Drawdown: -19.82% (3/16/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

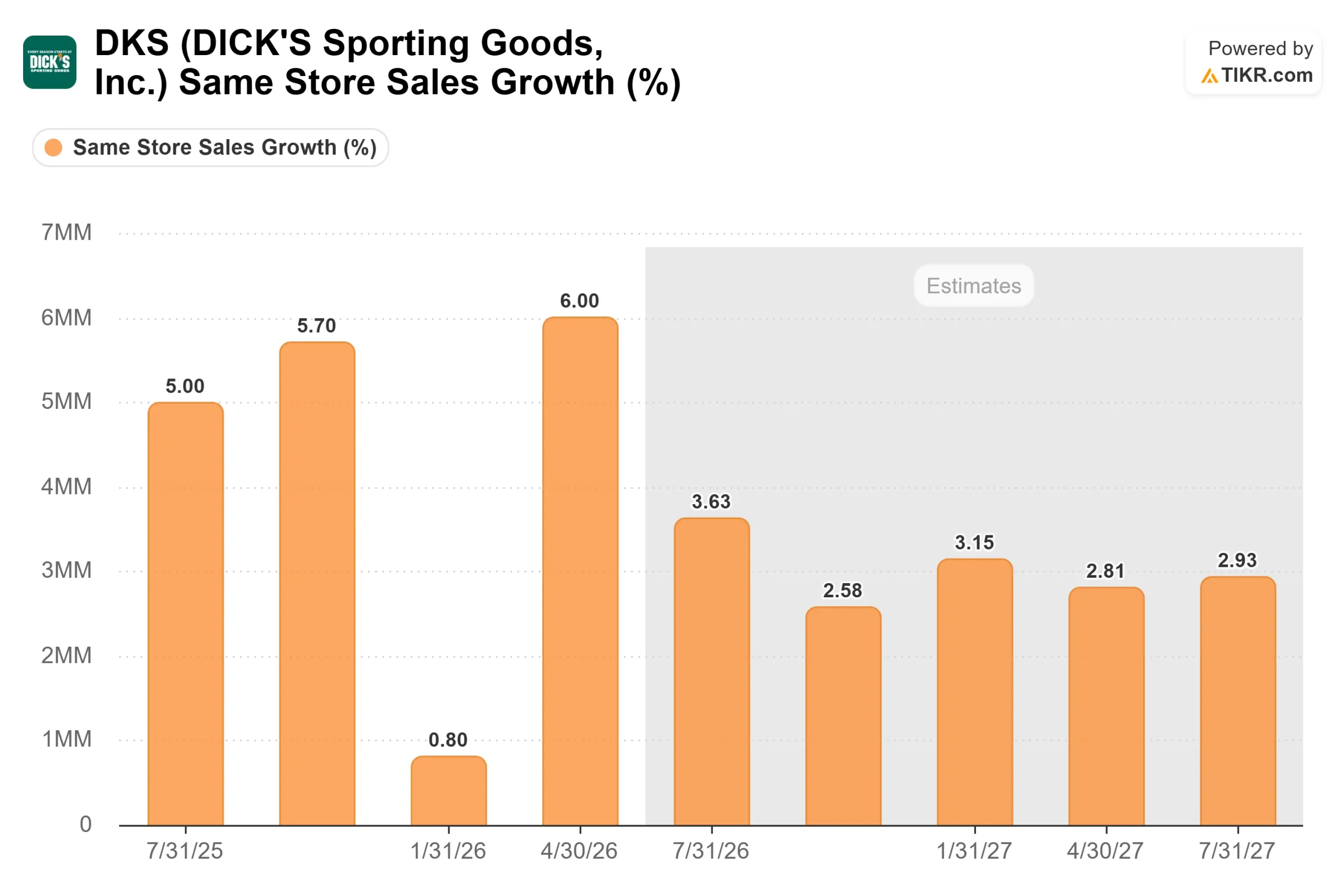

DICK’S Sporting Goods (DKS) delivered one of its strongest quarters on record this week. The core DICK’S business posted a 6% comparable sales increase, revenue beat consensus by nearly 2%, and EBITDA beat by more than 17%. Management raised guidance on both sales and margins.

The stock fell nearly 6%.

That gap between what the company delivered and how the market responded is the story. The selloff was not a verdict on the DICK’S business. It was a verdict on the Foot Locker acquisition and whether the market will ever fully separate the two.

A Business That Keeps Taking Share

Lauren Hobart, President and CEO, was unequivocal on the May 27 earnings call: “The 6% comp increase was not a result of a onetime factor. We saw broad-based strength across the entire portfolio.”

The numbers back it up. Average ticket rose 5.5%, and transactions rose 0.5%. Growth spanned footwear, apparel, and hardlines. The company added 1.5 million new athletes to its database in the quarter. DICK’S has now stacked comps of 6% in Q1 2026, 4.5% in Q1 2025, and 5.3% in Q1 2024, nearly 16% cumulative growth over three years. No signs of trade-down appeared across any income demographic. That is structural share gain, not a cyclical bump.

Ed Stack, Executive Chairman, framed the broader backdrop: “Sport is one of the hottest categories in the country today, and we’re in the middle of a real sports moment.” The 2026 FIFA World Cup is playing primarily on U.S. soil this summer, and management has already factored World Cup-driven demand into its first-half comp guidance. The 2028 Summer Olympics in Los Angeles sit further out, extending the runway. DICK’S also launched Coach by DICK’S on May 22, an agentic AI assistant built with Adobe Brand Concierge that delivers personalized sport and product guidance inside the DICK’S mobile app starting in June. It extends the brand’s in-store expertise into the digital channel, which matters for retention between purchase cycles.

See historical and forward estimates for DICK’s Sporting Goods stock (It’s free!) >>>

The Foot Locker Drag: Real, But Is It Permanent?

The market’s frustration has a logical basis. DICK’S acquired Foot Locker in September 2025, issuing 9.6 million new shares as part of the deal. That dilution persists until Foot Locker’s earnings catch up, and in Q1, they had not.

According to the Q1 2026 earnings release, the Foot Locker segment generated operating income of $17.5 million on $1.79 billion in revenue, a margin of 0.98%. The DICK’S segment operated at 10.69%. That margin gap is what pulled consolidated non-GAAP gross profit margin down 328 basis points year-over-year to 33.42%. CFO Navdeep Gupta confirmed the cause on the earnings call: “The year-over-year decline was primarily driven by mix impact from the Foot Locker business.” Adjusted EPS fell from $3.37 a year ago to $2.90, even as GAAP EPS rose from $3.24 to $3.54 due to a favorable litigation settlement.

Total pretax integration charges are expected to reach $500 million to $750 million, with roughly $200 million still to come through 2026 and beyond.

The early turnaround evidence is real, though. Pro forma Foot Locker comps turned positive for the first time since Q4 2024, rising 0.6% globally. The U.S. Foot Locker banner delivered a 6.4% comp, matching the DICK’S segment. The Fast Break initiative, a capital-light store remodel that cuts SKU count and reintroduces apparel, expanded from roughly 10 stores to approximately 100 in Q1. Those stores posted double-digit comps. Stack put it simply: “It’s retail 101. And when you execute it with discipline, it works.”

By back-to-school, DICK’S plans approximately 250 Fast Break stores globally. More importantly, that season marks the first time the DICK’S buying team will have had full control over Foot Locker’s assortment. Every prior quarter used inherited buys. Stack said the inflection point starts there, paired with a full Foot Locker brand relaunch.

Q2 will be the hardest quarter. World Cup marketing, concentrated House of Sport preopening costs, and continued integration charges all land at once. Gupta confirmed, “The most significant pressure is expected in Q2.” Investors who expected fast EPS normalization should expect another difficult quarter first.

See how DICK’s Sporting Goods performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $219.21

- Target Price (Mid): ~$313

- Potential Total Return: ~43%

- Annualized IRR: ~8% / year

See analysts’ growth forecasts and price targets for DICK’s Sporting Goods stock (It’s free!) >>>

The TIKR mid-case model targets approximately $313/share by January 2031, implying around 43% total return over roughly 4.7 years, or about 8% annually.

Two things drive the model. First, revenue is expected to compound at around 5% annually through the forecast period, supported by continued DICK’S share gains and a gradual Foot Locker recovery. Second, the mid-case net income margin assumption of around 6.5% represents a meaningful recovery from the 10-year historical average of 4.6%, as integration charges roll off. Gupta reaffirmed $100 million to $125 million in medium-term cost synergies, primarily from procurement and direct sourcing, with some arriving in 2026.

The primary risk is that Foot Locker’s structural challenges, including mall-based real estate and direct-to-consumer pressure from brand partners, prove harder to solve than the turnaround timeline assumes. If Foot Locker stalls, the margin recovery and EPS ramp both slow materially.

On relative valuation, DKS trades at 10.59x NTM EV/EBITDA, a discount to the specialty retail peer group mean of 13.68x. Its NTM P/E of 14.75x is roughly in line with the peer mean of 14.55x. The EBITDA discount is wider than it looks, because Foot Locker is temporarily compressing consolidated margins. As Foot Locker normalizes, those multiple gaps should narrow.

The Street is more conservative than the TIKR model. The mean analyst target sits at $240, implying about 10% upside. Post-earnings, Truist raised its target to $270 with a Buy, while Jefferies raised to $224 with a Hold. That spread captures the debate: bulls see a dominant sports retailer temporarily penalized for a well-timed acquisition; skeptics see dilution that takes years to earn back.

Conclusion

Back-to-school is the first real test. Watch the Q2 2026 results, due around August 25, for two specific data points: whether pro forma Foot Locker comps accelerate beyond the 1.5% to 3% full-year guidance range, and whether Foot Locker segment operating income shows meaningful improvement from Q1’s $17.5 million. If the first fully owned assortment and the Fast Break rollout deliver, the dilution thesis starts to close. If they disappoint despite the favorable setup, the timeline extends into 2027.

The DICK’S business has already answered the question investors had about it. At $219.21, the stock is a bet on whether Foot Locker earns its place in that story by year-end. August 25 is when investors find out.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in DICK’s Sporting Goods?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DICK’s Sporting Goods, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DICK’s Sporting Goods alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze DICK’s Sporting Goods on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!