Key Stats for Snowflake Stock

- Current Price: $175.26

- Target Price (Mid): ~$461

- Street Target: ~$229

- Potential Total Return: ~163%

- Annualized IRR: ~23% / year

- Earnings Reaction: +~36% after hours (May 27, 2026)

- Max Drawdown: 56.30% on April 10, 2026

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The Night Everything Changed for Snowflake

Snowflake Inc. (SNOW) spent most of 2026 looking like a business the market had given up on. The stock hit a max drawdown of 56.30% on April 10, even as the company beat estimates every quarter. Investors had priced in competitive collapse from Databricks, margin pressure from a consumption-based model, and GAAP losses with no clear end date.

That narrative collided with reality on May 27. Snowflake shares soared nearly 37% in after-hours trading after four things landed simultaneously: a record earnings beat, a full-year guidance raise, a $6 billion AWS infrastructure deal, and the announced acquisition of Natoma.

What the Numbers Actually Said

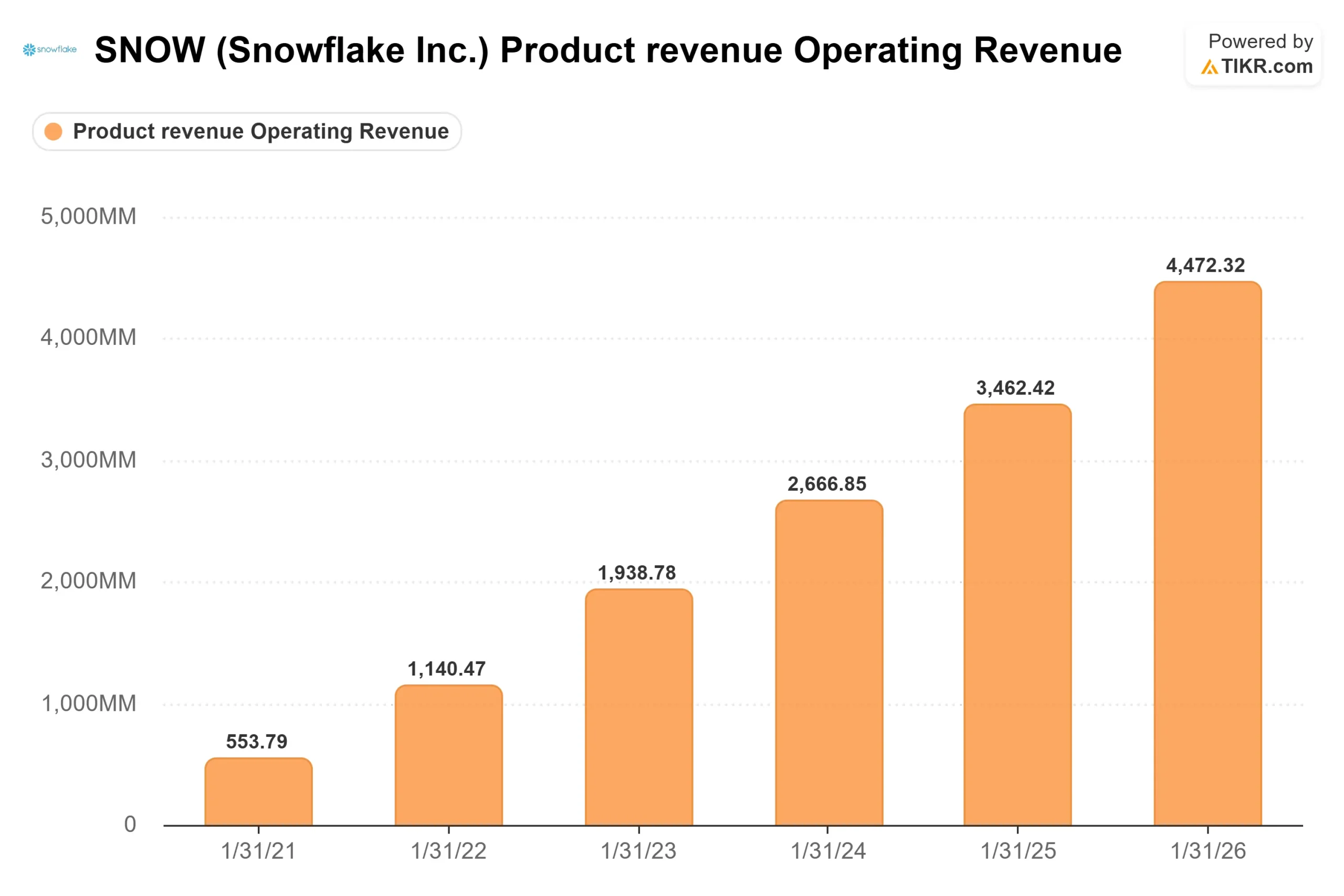

Snowflake reported product revenue of $1.33 billion in Q1 FY2027, up 34% year-over-year. Total revenue came in at $1.39 billion, up 33%. Net revenue retention, which measures how much existing customers are spending compared to a year ago, reached 126%. Remaining performance obligations grew 38% year-over-year to $9.21 billion.

Growth accelerated for the third straight quarter, from 26% a year ago to 30% last quarter to 34% now. CEO Sridhar Ramaswamy called it “the strongest sequential dollar growth in company history.” Two forces drove the acceleration. First, enterprises are migrating data to Snowflake faster because they need governed, structured data to run AI at scale. Second, Cortex Code (CoCo), Snowflake’s native coding agent that lets developers build applications in plain language, went into general availability on February 5 and contributed meaningfully in its first full quarter. CFO Brian Robins confirmed on the call: “CoCo had the largest driver to the increase in our forecast.”

Non-GAAP operating margin expanded over 300 basis points year-over-year to 12%, with organic headcount additions of just 17 people outside the Observe acquisition. Full-year product revenue guidance was raised to $5.84 billion, representing 31% growth, up from the prior guidance of $5.66 billion. Full-year non-GAAP operating margin guidance also increased, from 12.5% to 13.5%.

See historical and forward estimates for Snowflake stock (It’s free!) >>>

Three Catalysts in One Night

The $6 billion AWS deal. Amazon confirmed Snowflake committed to spending $6 billion on AWS over five years, including the purchase of its custom Arm-based Graviton chips and graphics processing units. The deal deepens a go-to-market partnership with the world’s largest cloud provider and is fully incorporated into Snowflake’s updated guidance.

The Natoma acquisition. Snowflake signed a definitive agreement to acquire Natoma, an enterprise MCP (Model Context Protocol) platform for AI agents. MCP is a standardized protocol that lets AI agents securely connect to external systems. The acquisition gives Snowflake a natively integrated governance and identity layer for AI agent access across SaaS applications, cloud environments, and on-premises infrastructure. As Ramaswamy put it in the press release: “AI agents don’t just need access to data. They need the right context, permissions and policy guardrails to operate safely inside the enterprise.”

Snowflake Summit. Snowflake hosts its annual Summit conference alongside an Investor Day on June 1 in San Francisco. Management has signaled new product showcases around CoCo and governance capabilities, making it a live near-term catalyst.

Why the Bears Still Have a Point

A 36% pop deserves scrutiny. At $175.26, Snowflake trades at around 10x NTM EV/Revenue and roughly 98x NTM P/E, per TIKR data. Those are not compressed valuation multiples. They price in sustained execution.

The consumption model cuts both ways. Revenue ties directly to how much customers actually use the platform, not to fixed subscriptions. If enterprise AI spending cools in the second half of 2026, revenue could miss guidance without any change in customer count or product quality. Robins reminded analysts that guidance philosophy has not changed: the CoCo uplift was layered in because observed behavior now existed, and a 3% beat is still considered a strong result.

Per TIKR consensus estimates, GAAP EPS does not turn positive until the fiscal year January 2031. The stock-based compensation burden is declining but still material. Combined with ongoing litigation tied to the 2023-2024 disclosure period, investors buying here are still accepting real execution risk.

See how Snowflake performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $175.26

- Target Price (Mid): ~$461

- Potential Total Return: ~163%

- Annualized IRR: ~23% / year

See analysts’ growth forecasts and price targets for Snowflake stock (It’s free!) >>>

The mid-case model’s two revenue drivers are AI-driven consumption growth within the existing 13,912-customer base and CoCo-accelerated migrations pulling new workloads onto Snowflake faster. Tonight’s 34% product revenue growth rate suggests the model’s 19% CAGR assumption may prove conservative. TIKR’s forward revenue consensus for FY2027 now sits at approximately $5.92 billion.

The margin driver is operating leverage. Net income margin in the mid-case expands toward approximately 14% by 2031 as revenue scales faster than costs and stock-based compensation continues declining as a percentage of revenue. The company is holding 75% non-GAAP product gross margin for the full year despite a lower-margin AI product mix, absorbing that headwind through reduced bandwidth costs under the new AWS contract.

Snowflake’s free cash flow profile supports the model. LTM levered free cash flow stands at approximately $1.76 billion per TIKR, and management reiterated a 23% adjusted free cash flow margin guide for FY2027. The primary risk the model does not fully capture is competitive displacement. If Databricks, Microsoft Fabric, or a hyperscaler-native platform meaningfully erodes Snowflake’s share of new AI workloads, the 19% CAGR assumption breaks.

Street consensus sits at a mean target of around $229, with 34 Buys, 10 Outperforms, 6 Holds, 1 No Opinion, and 1 Sell across 48 analysts per TIKR. That $229 target was set before tonight. Given the guidance raise and CoCo inflection, upward revisions across the Street are likely in the days ahead. Track those changes and earnings surprises in real time on TIKR.

Conclusion

The next real test is June 1 at Investor Day. The threshold is concrete: does management raise or hold FY2027 guidance a second time within a week, and do product announcements show a development cadence fast enough to keep Databricks and the hyperscalers from closing the gap? A second raise alongside Summit would confirm that Q1 was the start of a structural re-rating. A flat or cautious presentation would tell a different story, even after a 36% after-hours move.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Snowflake?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Snowflake, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Snowflake alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Snowflake on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!