Key Stats for HEICO Corporation Stock

- Current Price: ~$309(May 27, 2026)

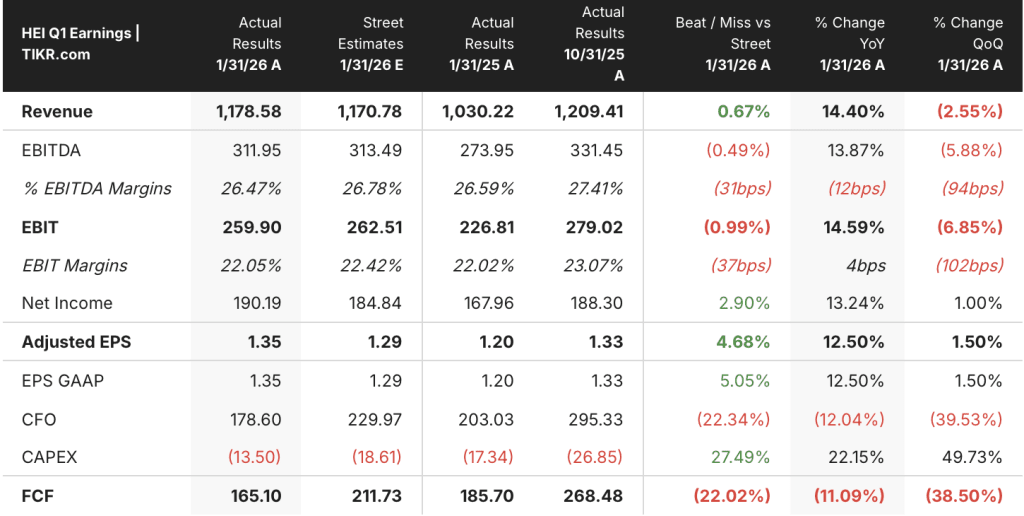

- Q1 FY2026 Revenue: $1.18B, +14% YoY

- Q1 FY2026 Adjusted EPS: $1.35, +13% YoY

- Q1 FY2026 FSG Operating Margin: 24.5% (up from 23.3%)

- Q1 FY2026 Consolidated EBITDA: $312M, +14% YoY

- Q1 FY2026 FSG Organic Revenue Growth: 12%

- TIKR Model Price Target: ~$505

- Implied Upside: ~63%

HEICO’s Flight Support Group Delivers a Margin Inflection That Changes the Earnings Story

HEICO Corporation (HEI) posted record consolidated net income of $190M in Q1 FY2026, a 13% year-over-year increase driven by an operating leverage inflection in the Flight Support Group that exceeded what the revenue headline alone implies.

The Flight Support Group was the decisive engine of the quarter, growing net sales 15% to $820M and operating income 21% to $201M, as SG&A expense efficiencies and a more favorable product mix in repair and overhaul amplified the revenue gains into disproportionate profit growth.

The single most undeniable figure from the print: FSG operating margin expanded to 24.5% from 23.3% in Q1 FY2025, while the FSG’s cash margin before acquisition-related intangibles amortization reached 27.1%, up 110 basis points year-over-year, making the margin story visible even after backing out M&A accounting noise.

Eric Mendelson, Co-Chairman and Co-CEO, stated on the Q1 FY2026 earnings call that HEICO “received consolidated margin expansion, record net income and strong increases in operating income and net sales,” anchoring a result that arrives on top of four consecutive years of high comparable periods in the FSG.

The 12% organic growth HEICO posted on those high comps establishes that the aftermarket demand cycle is not a post-COVID inventory correction but a structural repricing of the PMA and repair value proposition, and with roughly 20,000 parts in HEICO’s catalog and engine aftermarket parts running at a record level in Q1, the competitive moat compounds with each new OEM pricing escalation.

The Electronic Technologies Group introduced the only complication in the print: ETG net sales rose 12% to $371M with 6% organic growth, but operating margin contracted to 19.8% from 23.1% in Q1 FY2025, driven entirely by a product mix shift away from higher-margin defense and space products toward a greater proportion of lower-margin shipments in the quarter.

Victor Mendelson, Co-Chairman and Co-CEO, stated on the Q1 FY2026 earnings call that “based on our backlogs and our shipment plans, we expect the ETG margins to improve as the year progresses, particularly in the second half of the year,” pointing to record ETG backlogs and increasing order volumes as the mechanism for the expected recovery.

HEICO completed two acquisitions in the quarter and announced a third: Rockmart Fuel Containment (renamed from Axillon Aerospace’s fuel containment business, serving military fixed and rotary wing aircraft) closed in January, Ethos (industrial gas turbine and aeroderivative repair, with facilities in Connecticut, South Carolina, and Scotland) closed in February, and the FSG entered into an agreement to acquire 80% of a commercial aviation and defense component platform company, expected to close in Q2 FY2026.

The Ethos acquisition is a strategic pivot worth underscoring: it positions HEICO directly in the industrial gas turbine repair market at a moment when AI-driven power demand is accelerating the buildout of gas turbine-powered data center infrastructure, opening a revenue stream with no direct correlation to commercial airline cycles.

Is HEICO Stock Undervalued? What the TIKR Valuation Model Shows

TIKR’s base case values HEICO Corporation at approximately $505 by October 2030, implying around 63% total return from the current price of $309.40, or roughly 12% annualized over 4.4 years.

If FSG organic growth holds above 10% and ETG margins recover toward the 22% to 24% full-year guidance range, TIKR’s high case targets approximately $789, implying roughly 155% total return, or around 12% annualized.

If ETG mix pressure persists and organic growth decelerates to a low single-digit rate, the low case produces approximately $499, representing roughly 61% total return, or around 6% annualized.

The mid case at approximately $637 by October 2034 implies around 106% total return, or roughly 9% annualized, and requires sustained revenue growth in the 8% range alongside the margin profile management has guided.

How did HEICO perform in Q1 FY2026 earnings?

HEICO delivered adjusted EPS of $1.35 in Q1 FY2026, beating the $1.29 Street estimate by approximately 5%. Revenue reached $1.18B, up 14% year-over-year, while consolidated EBITDA grew 14% to $312M.

The FSG was the primary driver, posting 21% operating income growth on 12% organic sales growth as product mix and SG&A efficiencies expanded operating margin to 24.5%.

Management indicated continued sales momentum in both segments for the remainder of FY2026, supported by record ETG backlogs and increasing order volumes.

Is HEICO stock undervalued?

TIKR’s base case values HEICO stock at approximately $505 by October 2030, implying around 63% total return from the current price of $309.40, or roughly 12% annualized.

The FSG posted record-level engine aftermarket parts sales and 110 basis points of cash margin expansion in Q1, while HEICO’s net debt-to-EBITDA remained below 2x despite completing two acquisitions in the quarter.

The key variable is ETG operating margin: if it recovers to the 22% to 24% full-year guided range by Q3-Q4 FY2026, the base case is well supported.

Should You Invest in HEICO Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HEICO Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track HEICO Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HEICO stock on TIKR for Free →