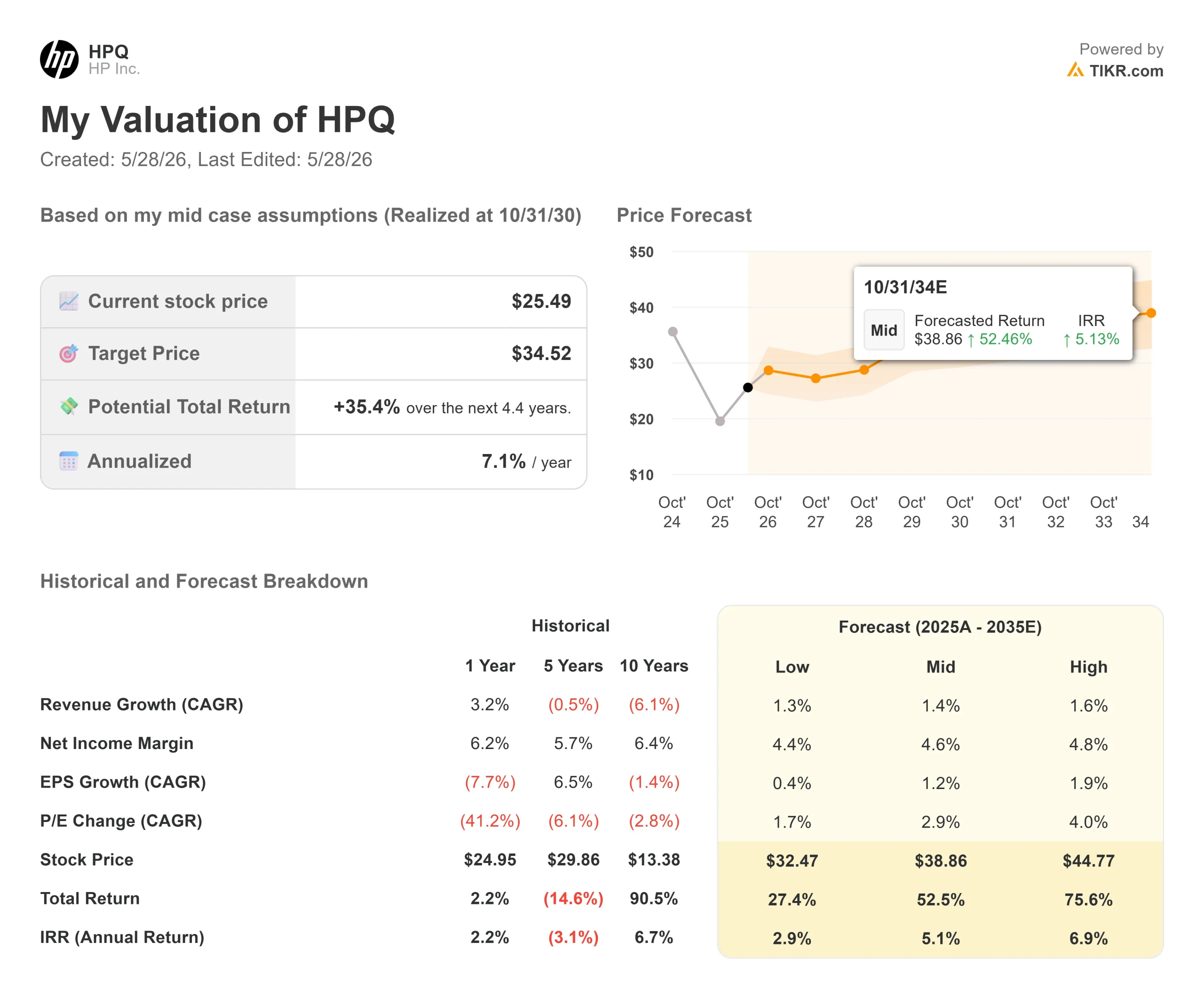

Key Stats for HP Inc. Stock

- Current Price: $25.49

- Target Price (Mid): ~$35

- Street Mean Target: ~$20

- Potential Total Return: ~35%

- Annualized IRR: ~7% / year

- Earnings Reaction: +4.34% (May 27, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

HP Inc. (HPQ) just silenced the bears, at least for one quarter. The company’s Q2 fiscal 2026 earnings release showed revenue of $14.4 billion, up 9% year-over-year, and non-GAAP EPS of $0.86, a 20% beat against the $0.71 consensus. The stock closed up 4.34% on May 27.

The setup heading into earnings was already charged. HPQ had surged 15% the prior week after rival Lenovo reported its fastest revenue growth in five years, with nearly 40% of sales coming from AI-related products per Lenovo’s own earnings disclosure. The market re-rated HP as a direct beneficiary before HP had even reported. The Q2 results confirmed the thesis. The question now is what the second half of fiscal 2026 actually looks like, because management was just as clear about that.

A Beat Built on Execution, Not Easy Conditions

Memory and storage costs rose sequentially through Q2, exactly as management had warned. HP beat anyway because CFO Karen Parkhill executed a three-part mitigation plan: accelerating product reconfiguration to qualify lower-cost components, using strategic low-cost inventory HP had pre-positioned, and implementing targeted repricing by customer, geography, and channel.

The result: Personal Systems operating profit grew 30% year-over-year, with operating margin at 5.2%, above guidance. AI PCs, devices with a dedicated neural processing unit built in to run AI workloads locally, jumped from 35% to 44% of HP’s shipment mix in a single quarter. Print revenue was flat year-over-year as expected, with an 18.3% operating margin. Industrial Graphics posted its 11th consecutive quarter of revenue growth.

HP raised full-year EPS guidance to $2.90–$3.10 and lifted its free cash flow outlook to solidly within the $2.8–$3.0 billion range.

The Back Half Is a Different Story

Parkhill was direct: Q3 will come in below seasonal norms for Personal Systems revenue because some commercial demand was pulled forward into Q2 ahead of rising commodity prices. HP estimates that pull-forward added roughly 2–3% of revenue in Q2. On top of that, the strategic low-cost inventory that protected Q2 margins will diminish through Q3 and Q4. As Parkhill said: “Based on what we’re seeing today, we would expect Q4 to be a low point, followed by sequential improvement into next fiscal year.”

That is not a reason to sell. It is a reason to know what the thesis requires: HP managing through a cost crunch while keeping its free cash flow intact. At a 4.8% NTM dividend yield with a 43.5% payout ratio, the dividend is not in danger even under pressure. LTM levered free cash flow stands at $3,275.88 million.The CEO search adds uncertainty. Former CEO Enrique Lores stepped down in February 2026, with board member Bruce Broussard serving as interim CEO. Broussard confirmed on the call that the board is actively evaluating candidates but offered no timeline.

See historical and forward estimates for HP Inc. stock (It’s free!) >>>

The AI Edge Thesis Is Bigger Than the Windows Refresh

What the earnings call transcript reveals beyond the near-term noise is a structural argument that most investors are not yet pricing. Ketan Patel, President of Personal Systems, described a genuine shift in enterprise computing: rising cloud costs associated with agentic AI, meaning AI systems that take autonomous actions across software and workflows, are pushing companies to bring AI processing to the device rather than routing everything through a data center. “There is a real shift happening towards the AI edge with workloads moving for reasons of latency, privacy, sovereign AI and the cost associated,” Patel said on the earnings call.

HP is positioning at the center of this shift through its AI PC platform, new Z workstations built for on-device inference, and HP IQ, an intelligence layer announced at HP’s annual HP Imagine showcase that coordinates integration across HP devices. The company has built an ecosystem of over 150 software partners developing AI workflows specifically for HP hardware.

Management guided AI PCs to reach 60–70% of HP’s shipment mix in fiscal 2027 and above 70% by fiscal 2028, up from 44% today. AI PCs carry higher average selling prices and attach more services, which structurally improves HP’s unit economics even in a flat PC unit market. Approximately 30% of the global installed base, per management, remains on Windows 10, adding a near-term refresh catalyst on top of the AI transition.

On valuation multiples, HP trades at 7.15x NTM EV/EBITDA and 9.36x NTM P/E. Per TIKR’s Competitors data, Lenovo trades at 6.73x NTM EV/EBITDA and 13.68x NTM P/E, while Canon trades at 6.32x NTM EV/EBITDA. HP’s premium to Lenovo on earnings multiple likely reflects its stronger Print margins and aggressive shareholder return program, though CEO uncertainty keeps the gap from closing fully.

The Street’s mean target of $19.68, held by 17 analysts split across 3 Buys, 1 Outperform, 8 Holds, 2 Underperforms, and 3 Sells, implies a 23% decline from current levels. That consensus was built when HP was trading near its 52-week low of $17.56. The Q2 beat and raised guidance have not yet moved it.

See how HP Inc. performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $25.49

- Target Price (Mid): ~$35

- Potential Total Return: ~35%

- Annualized IRR: ~7% / year

See analysts’ growth forecasts and price targets for HP Inc. stock (It’s free!) >>>

The TIKR mid-case uses a revenue CAGR of around 1.4% through fiscal 2030. The two drivers are AI PC mix upgrades lifting average selling prices in Personal Systems, and subscription and industrial print stabilizing the segment’s long-term decline. Net income margins are modeled at around 4.6%, recovering modestly from the near-term commodity-driven trough.

The floor for that recovery is HP’s restructuring program, which Parkhill confirmed is on track to generate approximately $1 billion in gross annualized run rate savings by the end of fiscal 2028.

The primary risk is commodity costs staying elevated longer than the mitigation playbook assumes, which would keep Personal Systems margins below 5% and slow the free cash flow generation that drives the buyback. On the upside, the high case targets around $45 by October 2030, if AI PC mix accelerates faster than the Street currently credits and triggers a faster P/E re-rating.

The mid-case is not pricing in a transformation. It prices in steady execution at around 7% annually.

Conclusion

The real test arrives around August 27, 2026, when HP reports Q3 fiscal 2026 results. Margins will compress. The question is how deep the trough goes and what management signals about the fiscal 2027 cost trajectory.

If Personal Systems margins hold above 3% and management signals memory cost headwinds are peaking, the stock has room to continue re-rating from a $19.68 Street consensus that has not caught up to where the business is. If margins fall further and cost guidance worsens, the recent rally will look like a head fake.

Watch the Personal Systems margin line. That number settles the debate.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in HP Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HP Inc., and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track HP Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze HP Inc. on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!