Key Takeaways:

- DaVita reported Q1 2026 diluted EPS of $2.87, up 43.5% year over year, with revenue rising to $3.42 billion and annual profit guidance raised.

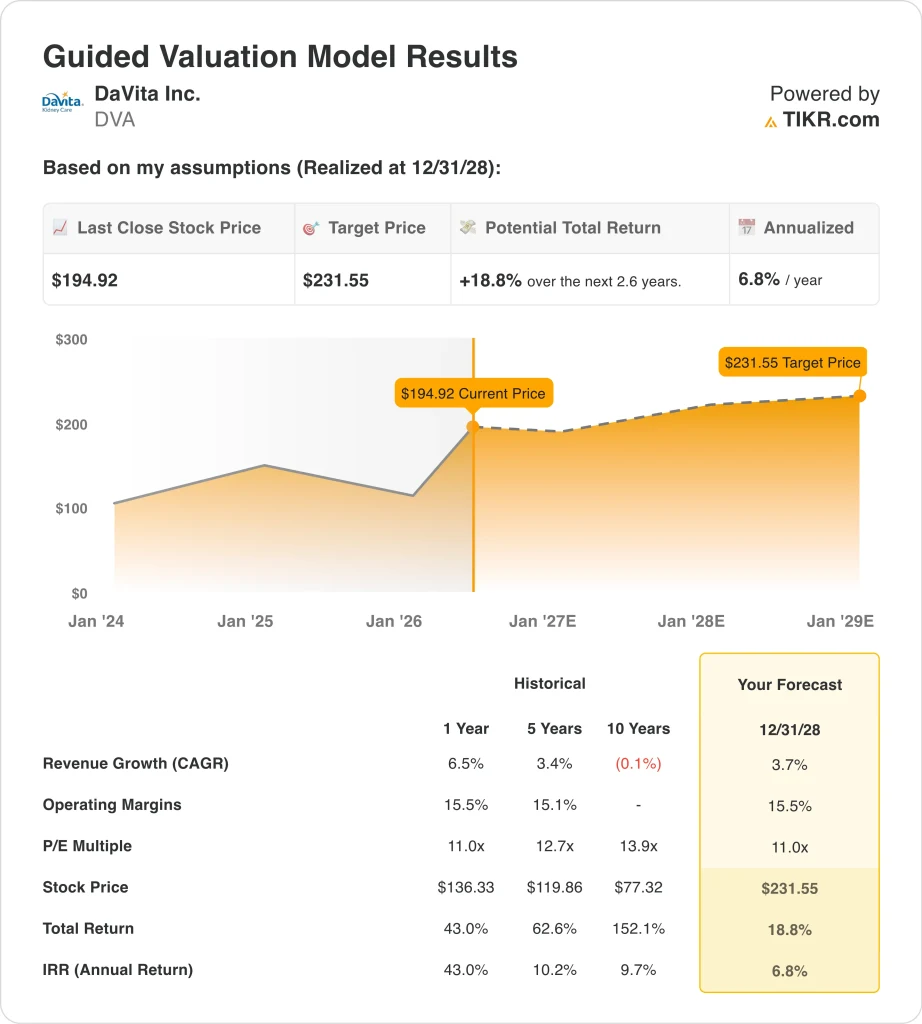

- DVA stock could potentially reach around $232 per share by December 2028, based on our valuation assumptions.

- This implies a total return of around 19% from today’s price of $195, with an annualized return of 6.8% over the next 2.6 years.

What Happened?

DaVita Inc. (DVA) reported Q1 2026 diluted EPS of $2.87, up 43.5% year over year, with revenue climbing to $3.42 billion. The company then raised its 2026 annual profit forecast, citing strong and sustained demand for outpatient dialysis services. DVA stock hit a record high on the news, as investors celebrated both the beat and the upgraded outlook. These results demonstrated that DaVita’s core dialysis business is on a solid growth trajectory.

Berkshire Hathaway sold 1.22 million DVA shares for approximately $183 million on May 6, 2026, at around $150 per share. This sale occurred even as the stock was rallying toward its record high, a development some investors viewed as notable from a historically supportive institutional holder.

A US appeals court also voided California’s law limiting dialysis providers’ profits in April 2026. That ruling removed a meaningful regulatory overhang for DaVita’s California operations.

DaVita set 2030 ESG goals in May 2026, including a target of 40,000 patient transplants. Management also presented at the Bank of America Global Healthcare Conference in May 2026, and the CFO discussed the raised profit guidance in a fireside chat.

Insider selling has been active, with the CFO and Chief Compliance Officer both disposing of shares worth millions in May 2026. Investors are broadly excited about the record-high stock price, but Berkshire’s exit and insider selling are prompting some to reassess the risk-reward setup.

Here’s why DaVita stock could offer solid capital returns through 2028 as its core business drivers support shareholder value.

What the Model Says for DVA Stock

We analyzed the upside potential for DaVita stock using valuation assumptions based on its dominant position in US outpatient dialysis, steady patient volume growth, and improving profitability per treatment driven by payer mix and cost control.

Based on estimates of 3.7% annual revenue growth, 15.5% operating margins, and a normalized P/E multiple of 11.0x, the model projects DaVita stock could rise from $195 to around $232 per share.

That would be an 18.8% total return, or a 6.8% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for DVA stock:

1. Revenue Growth: 3.7%

DaVita is the largest independent provider of outpatient dialysis services in the United States. Dialysis is an essential treatment for patients with end-stage renal disease (ESRD), who require multiple sessions per week because their kidneys can no longer filter blood adequately. Revenue is driven primarily by treatment volumes and per-treatment reimbursement rates from Medicare, Medicaid, and commercial insurers.

Q4 2025 revenue of $3.62 billion exceeded analyst estimates of $3.50 billion by around 3.5%. Results continued to build in Q1 2026, with revenue reaching $3.42 billion on solid treatment volumes. DaVita’s 2030 goal to achieve 40,000 patient transplants reflects a patient-first strategy, though transplants do reduce the long-term dialysis patient count.

Based on analysts’ consensus estimates, we used a 3.7% revenue growth rate for DaVita stock. This reflects steady growth in ESRD patient volume, modest increases in reimbursement rates, and gradual international expansion. The estimate aligns with the forward two-year revenue CAGR consensus of around 3.6%.

2. Operating Margins: 15.5%

DaVita reported an LTM EBIT margin of 15.0% and an LTM gross margin of 32.5%. Operating margins in dialysis are sensitive to staffing costs, supply chain, and payer mix, since commercial-pay patients generate significantly higher revenue per treatment than Medicare patients. Improving commercial payer mix is, therefore, a key profitability lever for DaVita.

Q1 2026 diluted EPS of $2.87 rose 43.5% year over year, reflecting both revenue growth and cost discipline. The California court ruling in April 2026 removes the risk of profit-capping legislation and improves the operating outlook in that key state. Higher reimbursement certainty is a direct positive for DaVita’s regional margin profile.

Based on analysts’ consensus estimates, we used a 15.5% operating margin assumption for DaVita stock. This is consistent with the company’s current LTM level and reflects sustained cost discipline and stable payer mix. Some upside to margins is possible if commercial contract growth accelerates in the coming quarters.

3. Exit P/E Multiple: 11x

DaVita stock trades at an NTM P/E of around 12.8x, modest for a healthcare services company. The street consensus target price of around $194 is roughly in line with the current share price of $195, suggesting the stock may be near analyst fair value estimates after its 70% YTD rally. A modest P/E multiple is typical for businesses where government reimbursement represents the primary revenue source.

DaVita’s LTM ROE of 81.0% is notably high, but partly reflects the company’s leveraged capital structure. LTM net debt stands at $12.6 billion, which adds meaningful financial risk in adverse operating environments. High leverage amplifies equity returns but also makes the company more sensitive to interest rate movements.

Based on analysts’ consensus estimates, we used an 11.0x exit P/E multiple for DaVita stock. This aligns with the company’s recent trading history and reflects the stable but slow-growth nature of dialysis reimbursement. It assumes no material re-rating of the multiple from current levels.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

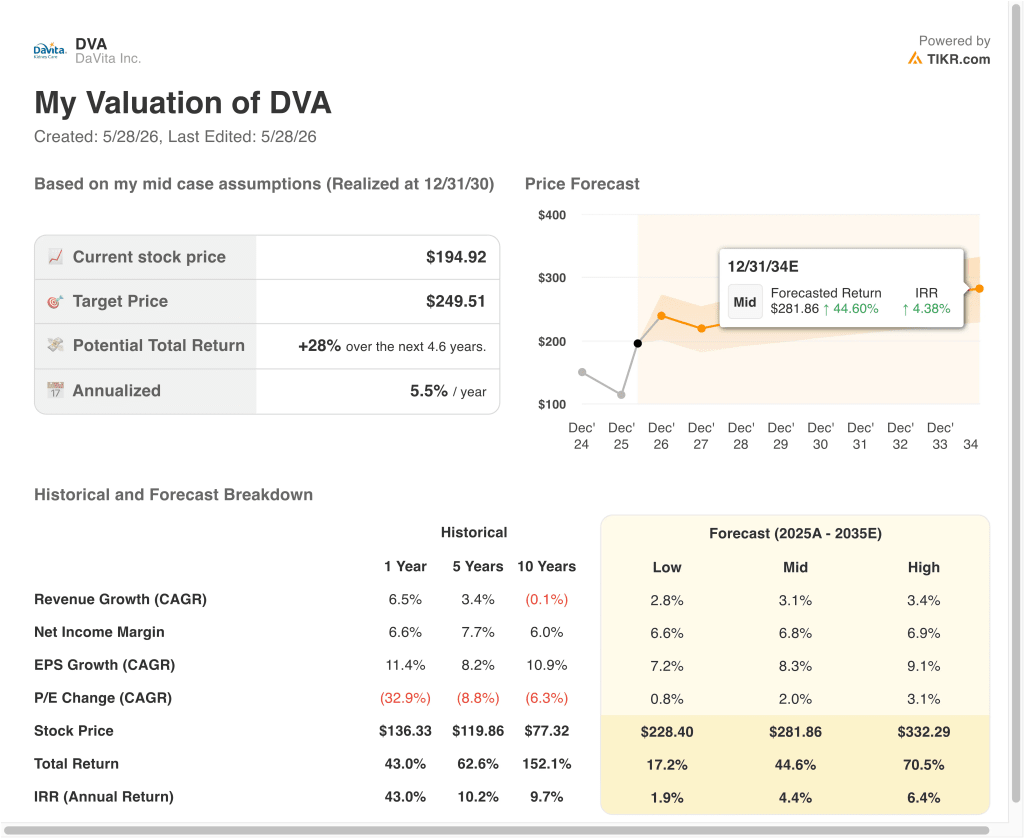

Different scenarios for DVA stock through 2034 show varied outcomes based on treatment volume growth, reimbursement rate changes, and payer mix improvement (these are estimates, not guaranteed returns):

- Low Case: Reimbursement rates disappoint, and volume growth slows below expectations → 1.9% annual returns

- Mid Case: Treatment volumes grow steadily, and payer mix holds relatively stable → 4.4% annual returns

- High Case: Commercial pay volumes rise, and margin improvement accelerates above the base case → 6.4% annual returns

Going forward, DaVita’s extraordinary 70% YTD rally has likely absorbed much of the near-term upside potential. Even the near-term 2028 model projects only 6.8% annualized returns, which falls below the 10% threshold many investors consider compelling.

The stock’s long-term path depends primarily on reimbursement policy stability, treatment volume growth, and management’s ability to service a substantial debt load as interest rates evolve.

See what analysts think about DVA stock right now (Free with TIKR) >>>

Should You Invest in DaVita?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DVA, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DVA alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!