Key Takeaways:

- Corning announced a multiyear partnership with Nvidia in May 2026, including equity investment and plant construction funding to expand U.S. optical connectivity capacity by 10x across three new facilities.

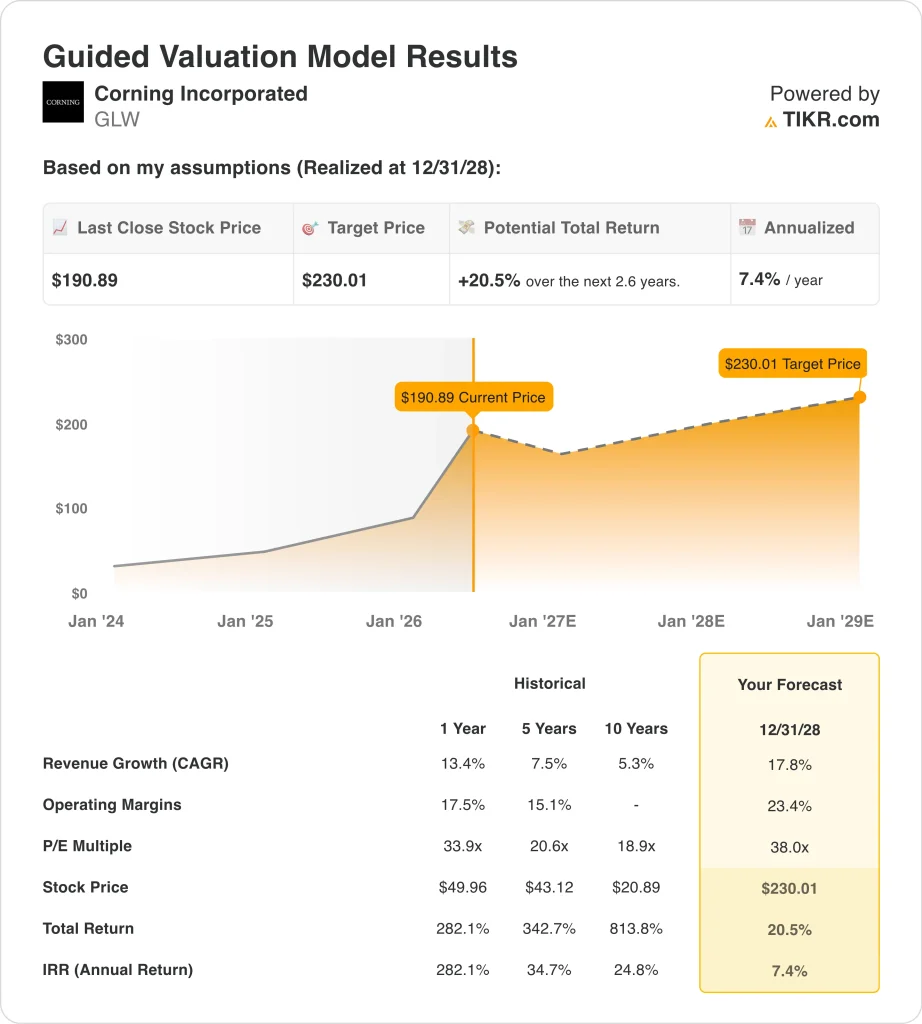

- GLW stock could rise from $191 to around $230 per share by December 2028, based on our valuation assumptions.

- That implies a total return of around 21% and an annualized return of around 7% over the next 2.6 years.

What Happened?

Corning Incorporated (GLW) has become one of the market’s most compelling stories in 2026. The stock gained 288% over the past year. Shares reached a 52-week high of $212, up from a low of just $49. The rally reflects a fundamental re-rating of Corning’s role in the global AI infrastructure buildout.

The most significant catalyst was a landmark multiyear partnership with Nvidia announced in May 2026. NVIDIA is funding the construction of three new Corning optical connectivity plants and making an equity investment in the company. Corning targets a 10x expansion of U.S. optical connectivity capacity as a result. Management also set an ambitious goal of reaching a $20 billion annualized sales run rate by the end of 2026.

Corning also signed a memorandum of understanding with BOE Technology in May 2026. Q1 2026 core EPS of $0.70 beat the IBES estimate of $0.69. The company has beaten quarterly EPS estimates in each of the past four reported quarters. Globalfoundries and Corning announced a collaboration to deliver detachable fiber connector solutions in September 2025, further expanding the optical connectivity product lineup.

Management presented its Springboard plan and generative AI strategy at an investor event in May 2026. The forward two-year revenue CAGR consensus stands at 17.4%. CFO and COO representatives presented at the J.P. Morgan Global Technology conference in May 2026. Here’s why Corning stock could offer solid capital returns through 2028 as its core business drivers support shareholder value.

What the Model Says for GLW Stock

We analyzed the upside potential for Corning stock based on its accelerating fiber optic capacity expansion, the transformative Nvidia partnership, and rising demand for optical connectivity infrastructure from AI data centers and global broadband networks.

Based on estimates of 17.8% annual revenue growth, 23.4% operating margins, and a normalized P/E multiple of 38.0x, the model projects Corning stock could rise from $191 to around $230 per share.

That would be a 20.5% total return, or a 7.4% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for GLW stock:

1. Revenue Growth: 17.8%

Corning operates across five segments: Optical Communications, Display Technologies, Specialty Materials, Environmental Technologies, and Life Sciences. Optical Communications is the fastest-growing segment, driven by AI infrastructure demand. The one-year revenue CAGR of 13.4% marks a significant reacceleration from prior years.

The Nvidia partnership is the most significant revenue catalyst in Corning’s recent history. A 10x expansion in U.S. optical connectivity capacity, funded with Nvidia’s construction support and equity investment, positions Corning to capture a large share of AI data center fiber demand.

Based on analysts’ consensus estimates, we used 17.8% annual revenue growth. This reflects the accelerating Optical Communications segment, the Nvidia partnership capacity ramp, and continued demand from both data centers and fiber broadband deployments globally.

2. Operating Margins: 23.4%

Corning’s LTM EBIT margin of 15.5% reflects solid profitability across its diversified portfolio. Gross margins of 36.4% are consistent with a mix of technology-intensive and commodity-linked products. Operating leverage is expected to be significant as the Nvidia-backed plants come online and fixed costs spread over a larger revenue base.

The Springboard plan presented to investors in May 2026 outlines a pathway to higher margins through product mix improvement and manufacturing scale. Management’s consistent EPS beats in recent quarters support confidence in the margin expansion thesis.

Based on analysts’ consensus estimates, we used 23.4% operating margins. This reflects meaningful expansion from current LTM levels as the Optical Communications segment scales and new plant capacity ramps under the Nvidia partnership.

3. Exit P/E Multiple: 38x

Corning currently trades at an NTM P/E of around 57x and an LTM P/E of around 92x. These premium multiples reflect the market’s repricing of Corning from a mature industrial company to a high-growth AI infrastructure beneficiary. The historical P/E for Corning was significantly lower, closer to 20x, before the AI connectivity theme emerged.

A 38.0x exit multiple reflects a view that Corning sustains elevated growth rates but that some multiple normalization occurs as the AI excitement matures. This still represents a significant premium to the company’s pre-AI valuation.

Based on analysts’ consensus estimates, we used a 38.0x exit multiple. This accounts for the durable competitive advantages in specialty glass and fiber optics, the transformative Nvidia partnership, and the expectation that AI infrastructure demand sustains strong capacity utilization through the forecast period.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for GLW stock through 2030 show varied outcomes based on AI data center fiber demand and optical connectivity capacity utilization (these are estimates, not guaranteed returns):

- Low Case: Capacity ramp faces delays, and AI fiber demand grows below expectations → 7.5% annual returns

- Mid Case: Nvidia partnership delivers on schedule, and AI data center demand meets consensus → 11.3% annual returns

- High Case: Capacity fills faster than planned, and Corning wins additional hyperscaler partnerships → 14.8% annual returns

Going forward, Corning’s stock performance will track closely with the pace of AI infrastructure buildout and the execution of the new optical connectivity plants coming online. The mid-case return of 11.3% annually over the long term suggests the stock could still be attractive at current prices for patient investors with a multi-year horizon.

The key risk is that current multiples already price in significant optimism about the AI fiber opportunity, so execution timing matters greatly.

See what analysts think about GLW stock right now (Free with TIKR) >>>

Should You Invest in Corning?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GLW, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GLW alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!