Key Takeaways:

- Dollar General named Jerry “JJ” Fleeman as its next CEO in March 2026, succeeding veteran Todd Vasos effective January 1, 2027, as the company works to stabilize operations.

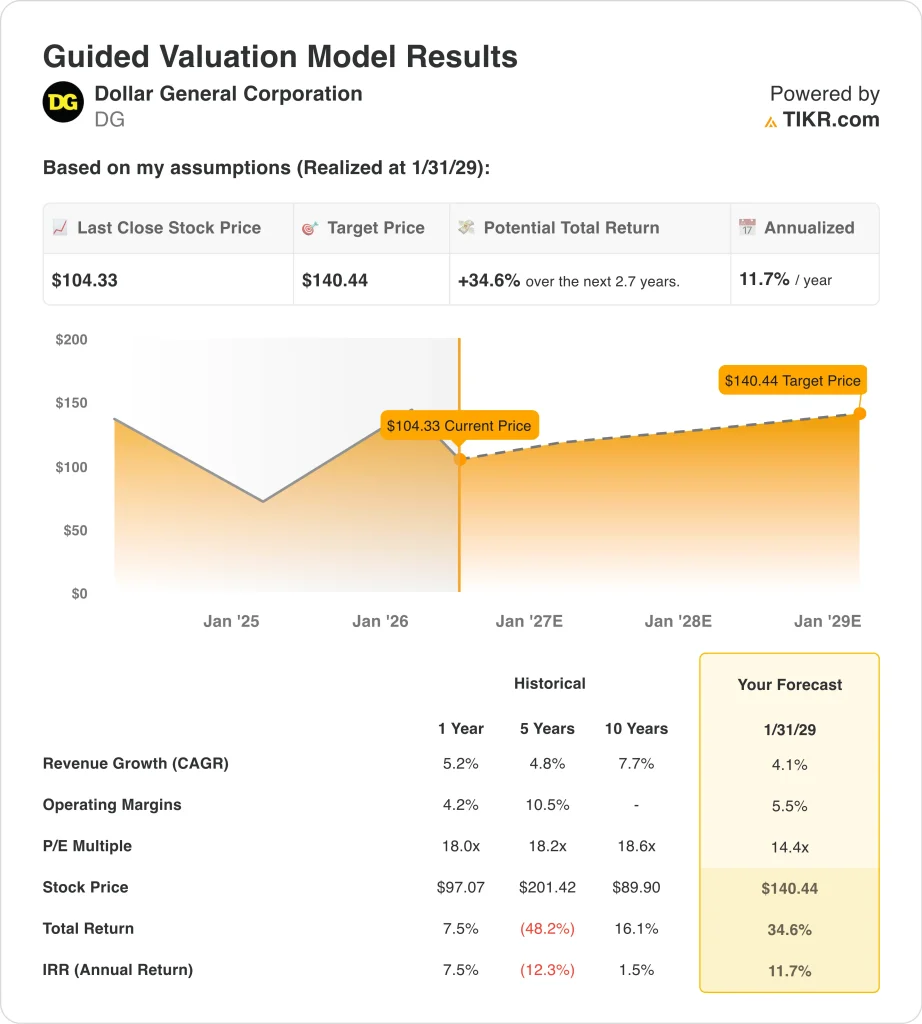

- DG stock could rise from $104 to around $140 per share by January 2029, based on our valuation assumptions.

- That implies a total return of around 35% and an annualized return of around 12% over the next 2.7 years.

What Happened?

Dollar General Corporation (DG) has endured a difficult stretch heading into 2026. The stock fell by over 32% in just three months. Shares traded near a 52-week low of $95, far below the 52-week high of $158. Investors are rethinking the setup after a CEO transition and a weak earnings backdrop.

Q4 FY2026 EPS came in at $1.93, and Q3 EPS was $1.28, both below historical profitability levels. Full-year net sales reached $42.7 billion per the company’s 2025 annual report. Revenue growth has been modest, with the one-year CAGR at 5.2%. Operating margins compressed to 4.2% on an LTM basis.

The company announced in March 2026 that Jerry “JJ” Fleeman will succeed Todd Vasos as CEO effective January 1, 2027. Fleeman currently leads Ahold Delhaize USA, a major U.S. grocery retailer. The leadership change initially rattled investors, but the appointment signals a focus on large-scale operational execution and cost control. Dollar General is also rolling out AI-enabled in-store audio and beauty promotions to improve traffic and basket size.

Analyst consensus puts the price target at around $140, well above the current price. The forward two-year revenue CAGR estimate stands at 4.1%, which is modest but achievable. Q1 FY2027 results are scheduled for June 2, 2026, providing an early glimpse of the new direction. Here’s why Dollar General stock could offer solid capital returns through 2029 as its core business drivers support shareholder value.

What the Model Says for DG Stock

We analyzed the upside potential for Dollar General stock based on its recovery potential in store-level profitability, its leadership transition under a new CEO, and its defensive positioning among value-focused U.S. consumers.

Based on estimates of 4.1% annual revenue growth, 5.5% operating margins, and a normalized P/E multiple of 14.4x, the model projects Dollar General stock could rise from $104 to around $140 per share.

That would be a 34.6% total return, or an 11.7% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for DG stock:

1. Revenue Growth: 4.1%

Dollar General operates over 20,000 stores across the United States, serving a core customer base of budget-conscious shoppers. The five-year revenue CAGR of 4.8% reflects consistent organic store growth even during periods of economic stress. One-year revenue growth of 5.2% shows the top line is still expanding at a healthy clip.

The company targets lower-income and rural consumers, giving it a defensive profile in weaker economic environments. New store openings and same-store sales improvement both contribute to the long-term growth narrative.

Based on analysts’ consensus estimates, we used a 4.1% revenue growth rate. This reflects Dollar General’s steady store base expansion and a modest same-store sales recovery as operational conditions normalize under new leadership.

2. Operating Margins: 5.5%

Dollar General’s LTM EBIT margin stands at 5.3%, well below the 10.5% operating margin level achieved over the prior five years. Margin compression has been a key investor concern, driven by rising shrinkage (inventory loss from theft), higher labor costs, and supply chain disruptions. Recovery toward more historical levels is a central part of the bull thesis.

The incoming CEO brings a background in large-scale retail operations, and that expertise could accelerate cost control and supply chain improvement. Midterm margin recovery depends heavily on how quickly leadership stabilizes operations.

Based on analysts’ consensus estimates, we used 5.5% operating margins. This reflects a partial recovery from current compressed levels, supported by ongoing cost actions and operational improvement under the new CEO.

3. Exit P/E Multiple: 14.4x

Dollar General currently trades at an LTM P/E of around 15x and an NTM P/E of around 14x. These multiples have compressed significantly from the historical range above 20x. Valuation has reset alongside the earnings decline and management uncertainty.

A 14.4x exit P/E is consistent with a business that has partially recovered its margin profile but not yet re-earned a premium multiple. If the new CEO successfully restores profitability, multiple expansions beyond this level become possible.

Based on analysts’ consensus estimates, we used a 14.4x exit multiple. This reflects a cautious but constructive view on the operational recovery trajectory, balanced against ongoing macro risks for the core low-income consumer.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for DG stock through 2031 show varied outcomes based on margin recovery progress and leadership execution (these are estimates, not guaranteed returns):

- Low Case: Margin recovery stalls and consumer spending stays pressured under macro headwinds → 7.1% annual returns

- Mid Case: New CEO drives steady cost improvements and same-store sales stabilize → 9.9% annual returns

- High Case: Rapid operational turnaround and margin expansion above consensus expectations → 12.4% annual returns

Going forward, Dollar General’s stock trajectory hinges on the incoming CEO’s ability to restore profitability and rebuild investor confidence. The defensive nature of the business model provides a floor, but multiple expansions require visible margin improvement. Investors following this story should treat the June 2026 Q1 FY2027 earnings release as an important early signal.

See what analysts think about DG stock right now (Free with TIKR) >>>

Should You Invest in Dollar General?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DG, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DG alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!