Key Stats for Lumentum Stock

- 52-Week Range: $72 to $1,086

- Current Price: $855

- Street Mean Target: $1,105

- Street High Target: $1,400

- Analyst Consensus: 15 Buys / 4 Outperforms / 5 Holds

- TIKR Model Target (June 2031): $3,089

Lumentum Stock Surges Into Its Nasdaq-100 Debut on Record Q3 Revenue and a $2 Billion Nvidia Bet

Lumentum Holdings (LITE), the San Jose-based maker of optical and photonic components for AI data centers, jumped roughly 17% on May 11, 2026, following its announcement that it would join the Nasdaq-100 index effective May 18 — a move that came just days after the company reported record fiscal Q3 revenue of $808.4 million, up 90% year-over-year.

The index inclusion was not the fundamental story. It was the confirmation of one.

Lumentum Holdings joined the S&P 500 in March 2026 and has risen over 1,000% in the past year as hyperscalers shifted from copper interconnects to high-speed optical networking inside their AI training clusters.

The revenue line reflects that shift directly. Components revenue reached $533 million in Q3, up 77% year-over-year, driven by narrow linewidth laser assemblies (up over 120% year-over-year for the ninth consecutive quarter) and pump lasers (up 80% year-over-year). Systems revenue hit $275 million, up 121% year-over-year, as cloud transceiver production scaled out of Lumentum’s expanded Thailand facility.

The margin story is the part the market underappreciates.

Non-GAAP gross margin expanded to 47.9% in Q3, up 540 basis points sequentially and 1,270 basis points year-over-year. Non-GAAP operating margin reached 32.2%, up 700 basis points sequentially and more than 2,100 basis points year-over-year. CEO Michael Hurlston noted on the earnings call: “Although we’re trailing what we’ve done in our previous instantiations, I do think there’s a lot of room for improvement on the gross margin line.”

Hurlston has run this playbook before. At his previous company, he expanded gross margins from 39% to over 60% in 18 months. Lumentum’s margin trajectory is following a similar path from a similar trough.

In March 2026, Nvidia made a $2 billion direct investment in Lumentum, locking in a substantial share of its indium phosphide laser capacity for co-packaged optics. That investment, now reflected on the balance sheet as a $3.17 billion cash position, is both validation of LITE’s technology and a constraint on how quickly management can serve other customers.

The supply-demand imbalance on EMLs (electro-absorption modulated lasers, the high-speed laser chips that drive transceiver performance) exceeded 30% during Q3 and has since widened. For pump lasers serving scale-across networks, the imbalance is described as “significantly” higher. Management is actively rationing output across customers while simultaneously signing long-term agreements to underwrite the CapEx required to close the gap.

Q4 guidance calls for revenue of $960 million to around $1.01 billion, with non-GAAP operating margin expanding further to 35% to 36%. The $985 million midpoint would mark another all-time quarterly record.

Is Lumentum Stock Undervalued in 2026? What Wall Street’s Targets Actually Say

The analyst table tells a clear story. At the end of March 2026, the mean price target for Lumentum stock was around $696. By May 29, it had risen to around $1,105. The current price of around $855 sits roughly 22% below that mean.

Fifteen of 24 analysts rate LITE a Buy. Four rate it Outperform. Five hold. Zero rate it Sell. That distribution — zero sell-side sellers across 24 covering analysts — is unusually uniform for a stock trading near 1,000% above its 52-week low.

The street high target of $1,400 implies around 64% upside from current levels.

The bull case rests on sequencing. Right now, Lumentum’s revenue is almost entirely driven by EML laser chips and transceivers. The four growth drivers management has identified — optical circuit switches (OCS), optical scale-out CPO, optical scale-up CPO, and 1.6T transceiver upgrades — are contributing modestly at best in Q4 and are expected to layer in through calendar 2026 and into 2027. CEO Hurlston even said at the J.P. Morgan Tech Conference in May: “We have very little contribution as yet in our numbers on any of the big growth drivers.”

OCS is the most visible near-term catalyst. Lumentum announced a multiyear, multibillion-dollar purchase agreement for its optical circuit switch technology in early 2026. Supply chain constraints are limiting the ramp, but management has outlined $400 million in OCS revenue targeted for the second half of calendar 2026. Scale-up CPO, which replaces copper links between AI chip clusters rather than inside individual racks, represents what management describes as a demand signal “somewhere north of 10x” greater than scale-out CPO.

The risk the bears track is well-defined. Insider selling has been substantial, with multiple executives and directors disposing of shares through May across a range of pre-arranged trading plans. Second, a portion of Lumentum’s indium phosphide capacity is now committed to Nvidia under the long-term agreement, which narrows flexibility if other hyperscalers accelerate demand faster than Lumentum can add supply. Third, the transceiver business is currently running below peer margins, which management has acknowledged and is working to close through vertical integration of its own CW lasers.

TIKR’s Model on Lumentum Stock Points to a Multi-Year Compounding Case

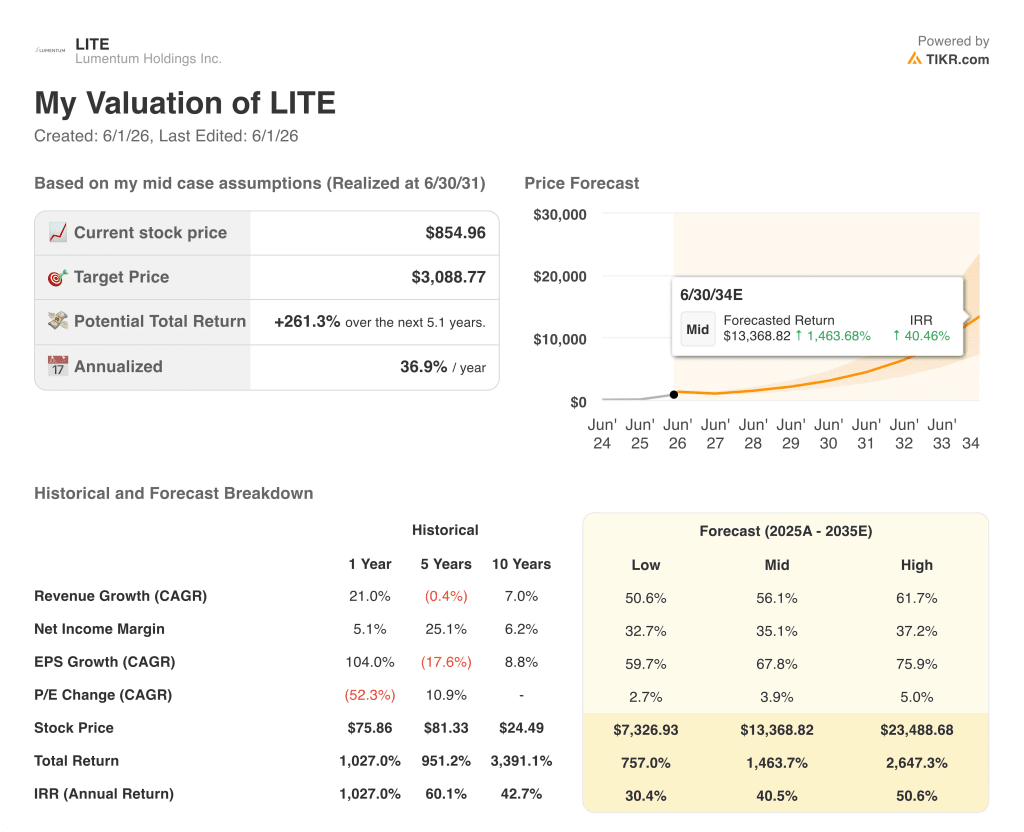

TIKR’s base case values Lumentum Holdings at approximately $3,089 by June 2031, implying around 261% total return from the current price of around $855, or roughly 37% annualized over about five years.

The low case puts the stock at approximately $7,327 by June 2034, representing around 757% total return at an annualized rate of roughly 30%. That scenario assumes a revenue CAGR near 51% and net income margins of around 33%.

The mid case reaches around $13,369 by June 2034, with a total return of roughly 1,464% and an annualized rate of approximately 41%, anchored to around 56% revenue CAGR and net income margins near 35%.

The high case reaches approximately $23,489 by June 2034, representing around 2,647% total return at roughly 51% annualized, assuming a revenue CAGR near 62% and net income margins of around 37%.

LITE appears significantly undervalued relative to TIKR’s base case. At around $855, the stock is pricing in a business that is generating record results today but has not yet received credit for the four growth drivers management identifies as only beginning to contribute.

Is Lumentum stock a buy right now?

Fifteen of 24 covering analysts rate Lumentum stock a Buy, with a mean price target of around $1,105 — roughly 29% above the current price of around $855.

The stock has pulled back from its all-time high of around $1,086 despite Q3 results showing 90% year-over-year revenue growth, record margins, and Q4 guidance calling for another quarterly record.

TIKR’s mid-case model puts the stock at approximately $3,089 by June 2031, implying around 261% total return from current levels.

What is the price target for LITE stock?

The Street mean target for Lumentum stock stands at approximately $1,105 as of late May 2026, with the high target at $1,400.

That high target implies around 64% upside from the current price of around $855. The range across 24 analysts reflects strong conviction, with zero sell ratings across the coverage universe and four growth drivers — OCS, scale-out CPO, scale-up CPO, and 1.6T transceivers — that management says have barely begun contributing to results.

Should You Invest in Lumentum Holdings Inc.?

You can build a free watchlist to track Lumentum Holdings Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Lumentum Holdings Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

Access Professional Tools to Analyze LITE stock on TIKR for Free →