Key Stats for PSX Stock

- Past-30-Day Performance: 7%

- 52-Week Range: $111 to $191

- Valuation Model Target Price: around $203

- Implied Upside: 15%

Analyze your favorite stocks like Phillips 66 with TIKR (It’s free) >>>

What Happened?

Phillips 66 stock rose about 7% over the last 30 days, recently trading near $177 per share as investors warmed back up to one of the stronger refining and cash-return stories in the energy sector. The stock remains below its 52-week high of $191, but the move suggests the market is giving PSX more credit for high refinery utilization, improving margins, and a balance sheet plan that still supports dividends and buybacks.

The stock moved higher because investors became more confident that Phillips 66 can benefit from tighter global fuel markets, stronger refining margins, and better chemicals pricing while still returning cash to shareholders. Jefferies raised its price target to $191 from $173 while keeping a Hold rating, and Mizuho upgraded Phillips 66 to Outperform from Neutral with a new $212 target, up from $170, citing improving refining operations, stronger execution, and more leverage to refining and chemicals margins. Those updates helped support the rally because they framed PSX as a margin recovery and cash-return story, not just a short-term refining trade.

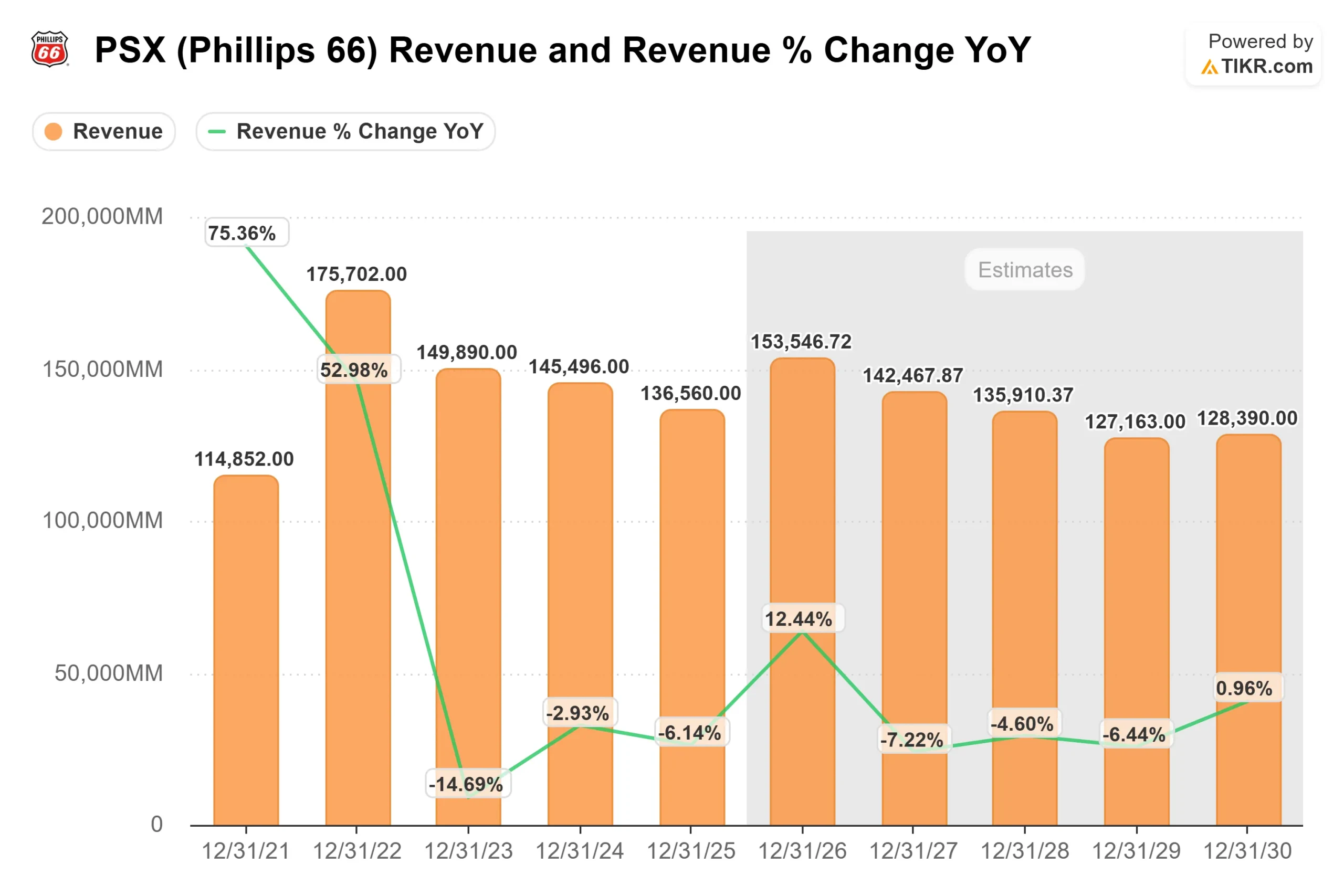

Phillips 66’s recent Q1 earnings call gave investors a mixed but useful read on the business, with reported earnings of $207 million, adjusted earnings of $200 million, adjusted EPS of $0.49, and refining operating at 95% capacity utilization with an 87% clean product yield. Refinery utilization measures how much of the company’s refining capacity is being used, while clean product yield shows how much output comes from higher-value fuels like gasoline, diesel, and jet fuel.

CEO Mark Lashier said, “The current environment is attractive across all our businesses,” pointing to tight global refining supply, high U.S. utilization, stronger chemicals margins, and commercial opportunities from energy market volatility.

The bigger question now is whether Phillips 66 can turn this stronger backdrop into steadier earnings through the rest of 2026. The company is being compared most closely with refiners such as Valero Energy, Marathon Petroleum, and HF Sinclair, while larger energy names like Chevron and Exxon Mobil help frame how investors are pricing fuel demand and capital returns across the sector. That matters for investors because PSX’s next move will likely depend on refining margin durability, chemicals recovery, midstream execution, debt reduction, and continued dividends and buybacks.

Value Phillips 66 instantly (Free with TIKR) >>>

Is PSX Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth: roughly flat

- Operating Margins: around 6%

- Exit P/E Multiple: 11x

Phillips 66’s valuation case is not built on major revenue growth, since refining revenue often moves with commodity prices rather than steady unit growth.

The bigger question is whether the company can turn high refinery utilization, stronger refining margins, and lower operating costs into better earnings.

The business could produce stronger results if refining margins stay constructive, chemicals margins recover, and the company’s commercial teams keep using its logistics network to capture value from tight global supply.

See analysts’ growth forecasts and price targets for Phillips 66 (It’s free) >>>

Midstream is another important driver because pipelines, gas processing, and NGL fractionation can make future cash flows less dependent on refining cycles, which puts PSX partly in conversation with infrastructure-heavy peers such as Enterprise Products Partners and ONEOK.

Based on these inputs, the model estimates a target price around $203, implying about 15% total upside over the model period, suggesting Phillips 66 appears modestly undervalued at current prices.

At current levels, Phillips 66 looks undervalued, with 2026 performance likely driven by refining margin durability, chemicals recovery, midstream growth, debt reduction, and steady dividends and buybacks.

How Much Upside Does PSX Stock Have From Here?

Investors can estimate Phillips 66’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Phillips 66 in under 60 seconds with TIKR (It’s free) >>>