Stock buybacks have become one of the primary ways companies return cash to shareholders. In recent years, buyback authorizations have regularly exceeded dividend payments, making repurchases a critical component of total shareholder returns.

Yet unlike dividends, which provide clear and immediate value, buybacks can either create or destroy value depending on how they are executed. The same repurchase program that enriches long-term shareholders in one scenario impoverishes them in another.

The debate around buybacks often misses this nuance. Critics argue that buybacks manipulate earnings per share, reward executives at shareholder expense, and divert capital from productive investment.

Defenders counter that returning excess cash to shareholders is exactly what management should do when internal opportunities are limited. Both sides have valid points, but neither captures the complete picture. Buybacks are a tool, and like any tool, their value depends entirely on how they are used.

The key variable is price. A company repurchasing shares well below intrinsic value transfers wealth from selling shareholders to remaining shareholders. Every dollar spent on buybacks generates more than a dollar of business value, creating an immediate gain for holders.

A company repurchasing shares at a price well above intrinsic value does the opposite, spending shareholder capital to acquire less than a dollar of value for each dollar spent. The same action that creates value in one case destroys it in the other.

Evaluating buybacks requires examining valuation at the time of repurchase, whether shares are actually being retired or merely offsetting dilution, how buybacks compare to alternative uses of capital, and whether management incentives align with shareholder interests.

This guide explains how to assess whether a company’s buybacks are genuinely benefiting shareholders and how to use TIKR to identify the patterns that distinguish value creation from value destruction.

Valuation at Time of Purchase

The math of buybacks is simple. When a company repurchases shares below intrinsic value, remaining shareholders own a larger percentage of the business at a lower cost than the business is worth. When a company repurchases shares at a price above intrinsic value, remaining shareholders own more of a business worth less than the capital consumed. Price relative to value determines whether buybacks help or hurt.

This seems obvious, yet many companies ignore it entirely. They repurchase shares aggressively when stock prices are high and cash is plentiful, then halt buybacks when prices fall and cash is needed for operations. This pattern is precisely backward from a value-creation standpoint. It amounts to buying high and selling low, destroying shareholder value with each transaction.

The best capital allocators do the opposite. They repurchase aggressively during market downturns or when their stock is temporarily out of favor, then conserve cash when valuations are stretched. This countercyclical approach requires management to have a clear view of intrinsic value and the discipline to act against market sentiment. Few leadership teams possess both qualities, which is why most buyback programs fail to create meaningful value.

Examine the company’s repurchase history relative to its stock price. If buybacks peaked when the stock was at all-time highs and ceased when the stock fell 40%, management was buying high and stopping low. If buybacks accelerated during periods of stock weakness, management demonstrated the discipline that creates value. The pattern over multiple years reveals whether leadership treats buybacks as value creation or as a default use of excess cash.

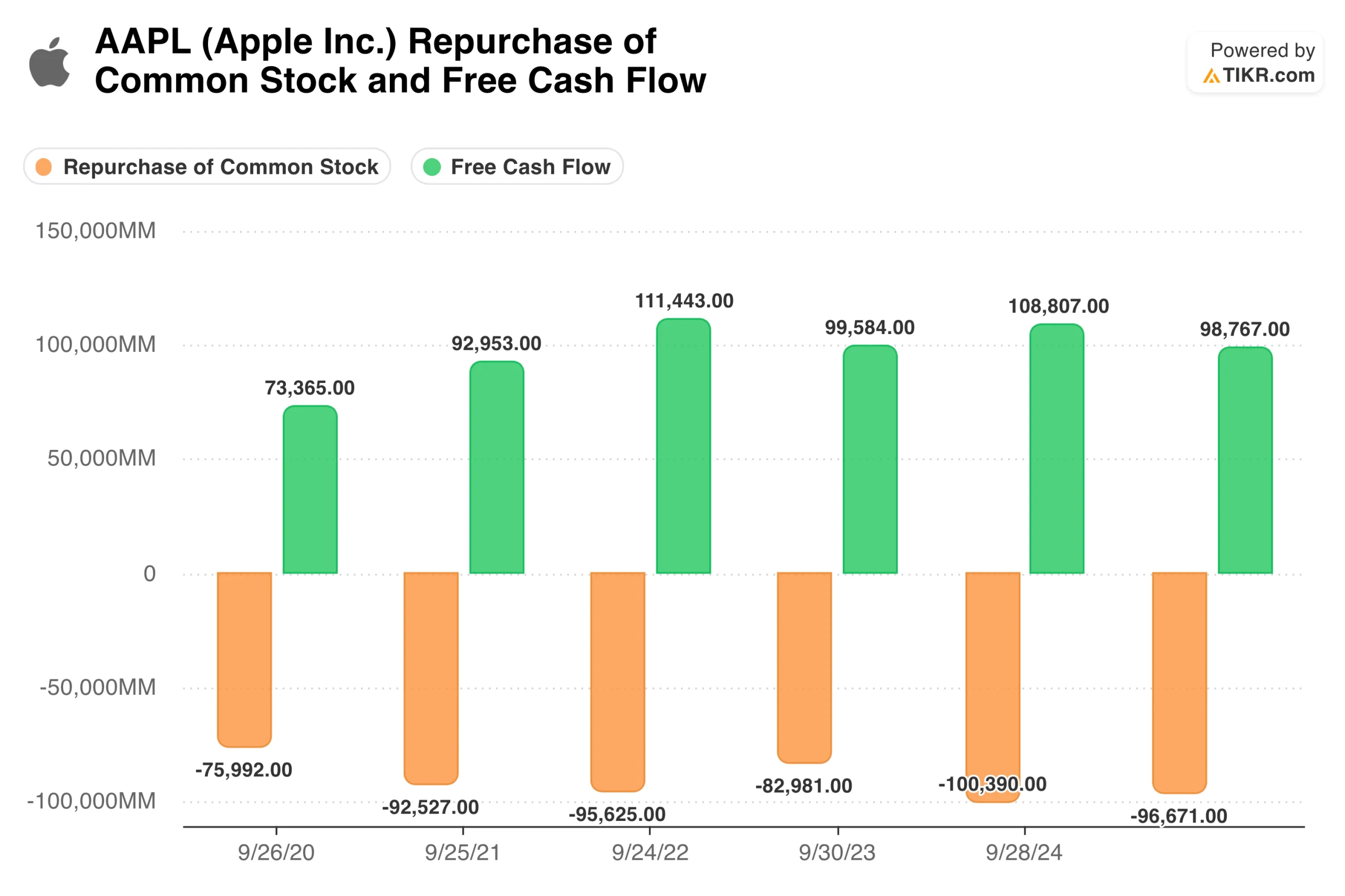

TIKR tip: Compare the company’s historical buyback activity with its stock price chart, as shown for Apple (AAPL) above. TIKR’s Cash Flow Statement shows share repurchases by period, which you can overlay with price history to see whether management bought at attractive or unattractive valuations.

Screen over 75,000 global stocks to find companies buying back their stock (Free with TIKR) >>>

Actual Share Count Reduction

A buyback program benefits shareholders only if it reduces the number of shares outstanding. Many companies announce large repurchase authorizations and execute them fully, yet share count remains flat or even increases over time. The buybacks are real, but they merely offset dilution from stock-based compensation rather than shrinking the equity base.

This pattern is particularly common in technology companies, where equity compensation accounts for a significant portion of employee pay. A company might repurchase $500 million of stock annually while issuing $600 million in stock-based compensation. The headline buyback sounds impressive, but shareholders end up with a larger share count than they started with. The buyback program is essentially a transfer from shareholders to employees disguised as a capital return.

Track the actual share count over time rather than relying on announced repurchase amounts. A company that has reduced shares outstanding by 3% annually for a decade has genuinely returned capital to shareholders through buybacks. One that has maintained flat share count despite consistent repurchases has merely neutralized dilution. Both might announce similar buyback programs, but only one is actually shrinking the pie that shareholders divide.

The dilution-adjusted buyback yield provides a cleaner picture than gross repurchases. Calculate the net change in shares outstanding as a percentage of the starting count. A company spending 4% of its market cap on buybacks but experiencing 2% annual dilution has a net buyback yield of only 2%. The gross figure overstates the actual return to shareholders by half.

TIKR tip: Review shares outstanding over multiple years in TIKR’s Detailed Financials. Compare the trend in share count to reported buyback amounts. A shrinking share count confirms buybacks are creating value. A flat or rising count despite repurchases indicates dilution is consuming the returns, something that Apple has shown over time, according to the above chart.

Review a company’s financial statements and analyst estimates with TIKR for free >>>

Share Buybacks Compared to Other Capital Allocation Options

Capital allocation is about choosing among alternatives. Every dollar spent on buybacks is a dollar not spent on reinvestment, acquisitions, debt reduction, or dividends. Buybacks create value only when they represent the best available use of that capital. A company that repurchases stock while neglecting high-return investment opportunities is making a mistake even if the shares are attractively priced.

The reinvestment question comes first. If a company can deploy capital into its business at returns well above its cost of capital, it should generally do so rather than buy back stock. A retailer with opportunities to open profitable new stores, a software company with products to develop, or a manufacturer with capacity to expand should invest before returning capital. Buybacks make sense when internal opportunities are limited or when returns on incremental investment have declined.

Debt reduction sometimes offers better risk-adjusted returns than buybacks. A company with significant leverage might create more value by paying down debt than by repurchasing equity, particularly if interest rates are high or credit spreads are wide. Reducing debt improves financial flexibility, lowers interest expense, and reduces the risk of distress during downturns. A certain return from debt reduction can exceed the uncertain return from buybacks at questionable valuations.

Dividends provide an alternative that lets shareholders make their own allocation decisions. A dividend puts cash in shareholders’ hands to deploy as they see fit. A buyback assumes that repurchasing shares is the best use of that cash, which requires management to be correct about valuation. For companies without a clear view of intrinsic value, dividends may be the more honest way to return capital.

TIKR tip: Examine returns on capital in TIKR’s Ratios section alongside buyback activity. A company with a high ROC and abundant reinvestment opportunities should invest rather than repurchase. Buybacks make more sense when the ROC is mature, and investment opportunities are limited.

Evaluate return on capital to find stocks with solid financials to buy today (Free with TIKR) >>>

Management Incentives and Motivations

Management teams have incentives that may not align with shareholders’ interests regarding buybacks. Understanding these motivations helps distinguish value-creating repurchases from self-serving ones.

Earnings per share targets create problematic incentives. When executive compensation is tied to EPS targets, management can meet them by reducing share count rather than growing earnings. A company that cannot grow its business might repurchase shares aggressively simply to maintain EPS growth and trigger bonus payments. The buybacks serve management rather than shareholders, particularly when executed at unattractive valuations.

Stock option programs create additional conflicts. Executives holding options benefit from higher stock prices regardless of how those prices are achieved. Buybacks that reduce share count and boost EPS can lift stock prices in the short term even if they destroy long-term value. Management captures gains from option exercises, while shareholders bear the cost of overpaying for repurchased shares.

The timing of buybacks around equity grants can reveal motivations. Some companies accelerate repurchases before the end of measurement periods to recognize compensation, or slow them when executives are selling. These patterns suggest management is using buyback timing to benefit insiders rather than to maximize value for all shareholders. Consistent execution regardless of compensation cycles indicates better alignment.

Examine whether management communicates a clear framework for repurchase decisions. Do they articulate a view on intrinsic value and how it compares to the current price? Do they explain why buybacks represent the best use of capital versus alternatives? Leaders who carefully consider capital allocation can explain their rationale. Those using buybacks as a default or for earnings management typically cannot.

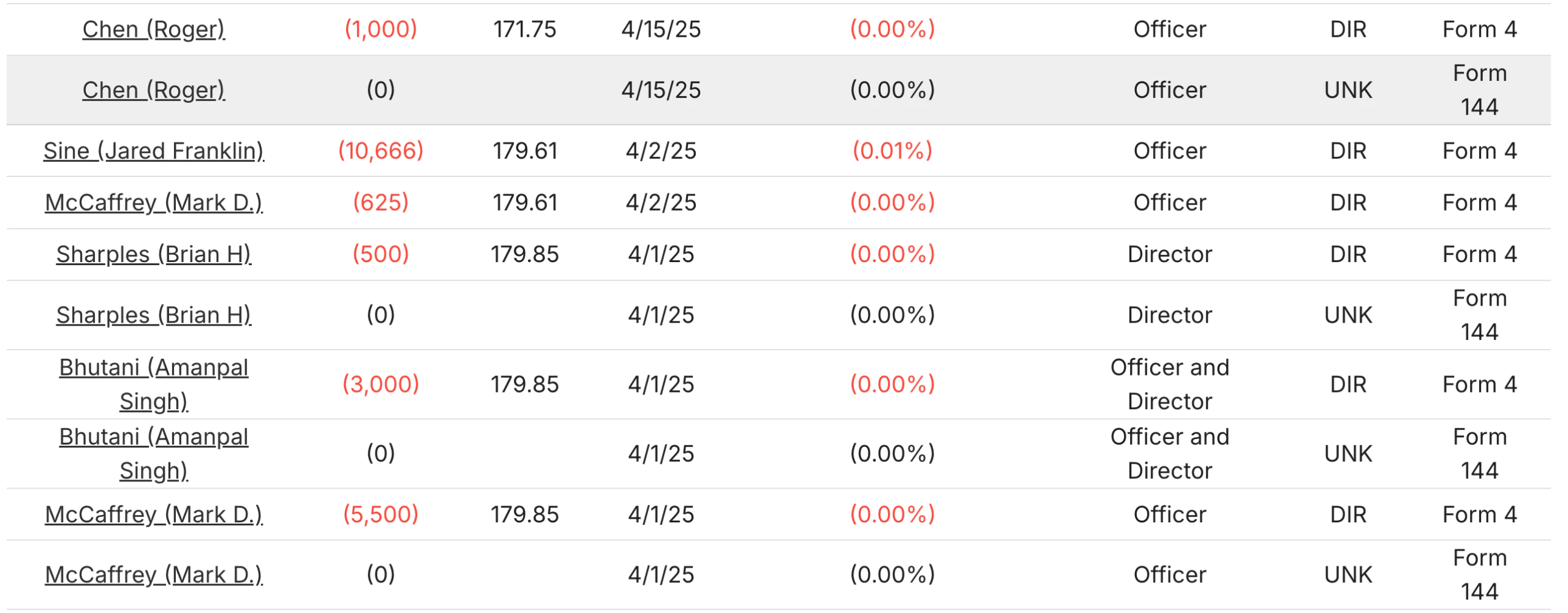

TIKR tip: Review executive compensation structures in proxy filings and compare buyback timing to equity grant and vesting schedules. TIKR’s Ownership tab shows insider transactions, like recent ones from Apple, that may coincide with repurchase activity, allowing you to compare and contrast the information.

Cash Flow Sustainability

Buybacks should be funded by sustainable free cash flow rather than debt or asset sales. A company that borrows to repurchase shares is increasing financial risk to boost per-share metrics. A company that consistently generates free cash flow in excess of reinvestment needs can repurchase shares without straining its balance sheet.

Calculate whether the company generates enough free cash flow to fund its buyback program comfortably. A business producing $1 billion in annual free cash flow can sustain $500 million in annual repurchases indefinitely while still investing in growth, paying dividends, and maintaining financial flexibility. One producing $500 million in free cash flow but repurchasing $800 million annually is either depleting cash reserves or taking on debt to fund repurchases.

Cyclicality matters for sustainability. A company might generate ample free cash flow at the peak of its cycle but minimal cash flow at the trough. If buybacks are sized to peak cash generation, they become unsustainable when conditions normalize. The best programs are sized to trough cash generation, allowing acceleration when times are good but maintaining a baseline that persists through downturns.

Debt-funded buybacks deserve particular scrutiny. Taking on leverage to repurchase shares is a bet that the stock is undervalued by more than the cost of debt. This bet sometimes pays off, but it increases financial risk and reduces flexibility for future opportunities. Companies that routinely borrow to fund repurchases are prioritizing near-term EPS growth over long-term financial stability.

TIKR tip: Compare free cash flow to buyback spending in TIKR’s Cash Flow Statement over multiple years. Sustainable programs show repurchases consistently below free cash flow generation. Unsustainable programs show repurchases exceeding free cash flow, funded by rising debt.

Screen stocks for free cash flow for over 75,000 global stocks with TIKR (It’s free) >>>

Patterns That Indicate Value Creation

Certain patterns suggest a buyback program is genuinely creating value for long-term shareholders rather than serving other purposes.

Countercyclical execution indicates disciplined capital allocation. A company that accelerated repurchases during the 2020 market panic or the 2022 selloff was buying when prices were low. One that halted buybacks during those periods and resumed when prices recovered was buying high. The willingness to act against sentiment, purchasing more when others are fearful, distinguishes value-creating programs from mechanical ones.

Consistent reduction in share count over extended periods confirms that buybacks are actually returning capital rather than merely offsetting dilution. A company that has shrunk its share count by 30% over a decade has meaningfully increased each remaining share’s claim on the business. The compounding effect of sustained share reduction can be substantial.

Management communication that emphasizes value over volume suggests thoughtful execution. Leaders who discuss intrinsic value, explain their valuation framework, and describe how repurchase decisions are made are more likely to execute intelligently. Those who emphasize the size of authorization or the total dollars spent without reference to value may be optimizing for appearances rather than returns.

Insider buying alongside corporate repurchases aligns interests. When executives, like those at GoDaddy (GDDY), buy or sell shares with their own money at the same time the company is buying back stock, as was the case in April 2025, incentives are aligned. They are betting their personal capital on the same thesis that guides corporate repurchases. This alignment provides confidence or concern that management genuinely believes shares are undervalued.

TIKR tip: Use TIKR’s Ownership tab to check whether insiders are buying shares personally during periods of corporate repurchase activity. Alignment between personal and corporate buying suggests genuine conviction about valuation.

The TIKR Takeaway

Stock buybacks can be powerful tools for value creation or mechanisms for value destruction, depending entirely on how they are executed. The difference between a great buyback program and a poor one lies in valuation discipline, actual share count reduction, comparison to alternative uses of capital, management incentives, and sustainability of funding.

The best buyback programs repurchase shares when prices are below intrinsic value, reduce share count rather than merely offset dilution, represent the highest-return use of available capital, align management incentives with shareholder interests, and are funded by sustainable free cash flow. Programs that lack these characteristics may boost near-term EPS while destroying long-term value.

TIKR provides data to systematically evaluate buyback quality. The Cash Flow Statement reveals repurchase amounts over time. Share count trends show whether buybacks are actually reducing equity. ROC and reinvestment metrics indicate whether capital has better alternative uses. Insider transaction data reveals whether management is aligned with corporate repurchase activity.

Not all buybacks are created equal. Understanding which ones create value and which ones destroy it helps you identify companies where capital allocation works in your favor and avoid those where it works against you.

Find undervalued stocks in less than 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Value Any Stock in Under 60 Seconds with TIKR

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios, so you can quickly determine whether a stock is undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- Discover which stocks billionaire investors are purchasing, so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!