Key Stats for NXP Semiconductors Stock

- Past-Week Performance: 7%

- 52-Week Range: $148 to $255

- Valuation Model Target Price: $361

- Implied Upside: 53%

Value your favorite stocks like NXP Semiconductors N.V. with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

NXP Semiconductors stock rose about 7% this week, finishing near $237 per share, as investors reacted to stronger-than-expected earnings, improved forward guidance, and a wave of analyst price target revisions. Shares held most of their gains through the week, signaling sustained buying interest rather than a short-term reaction.

The stock moved higher because NXP delivered earnings above guidance and issued better-than-expected Q1 revenue outlook, reinforcing confidence that the inventory correction in automotive and industrial markets is largely behind the company.

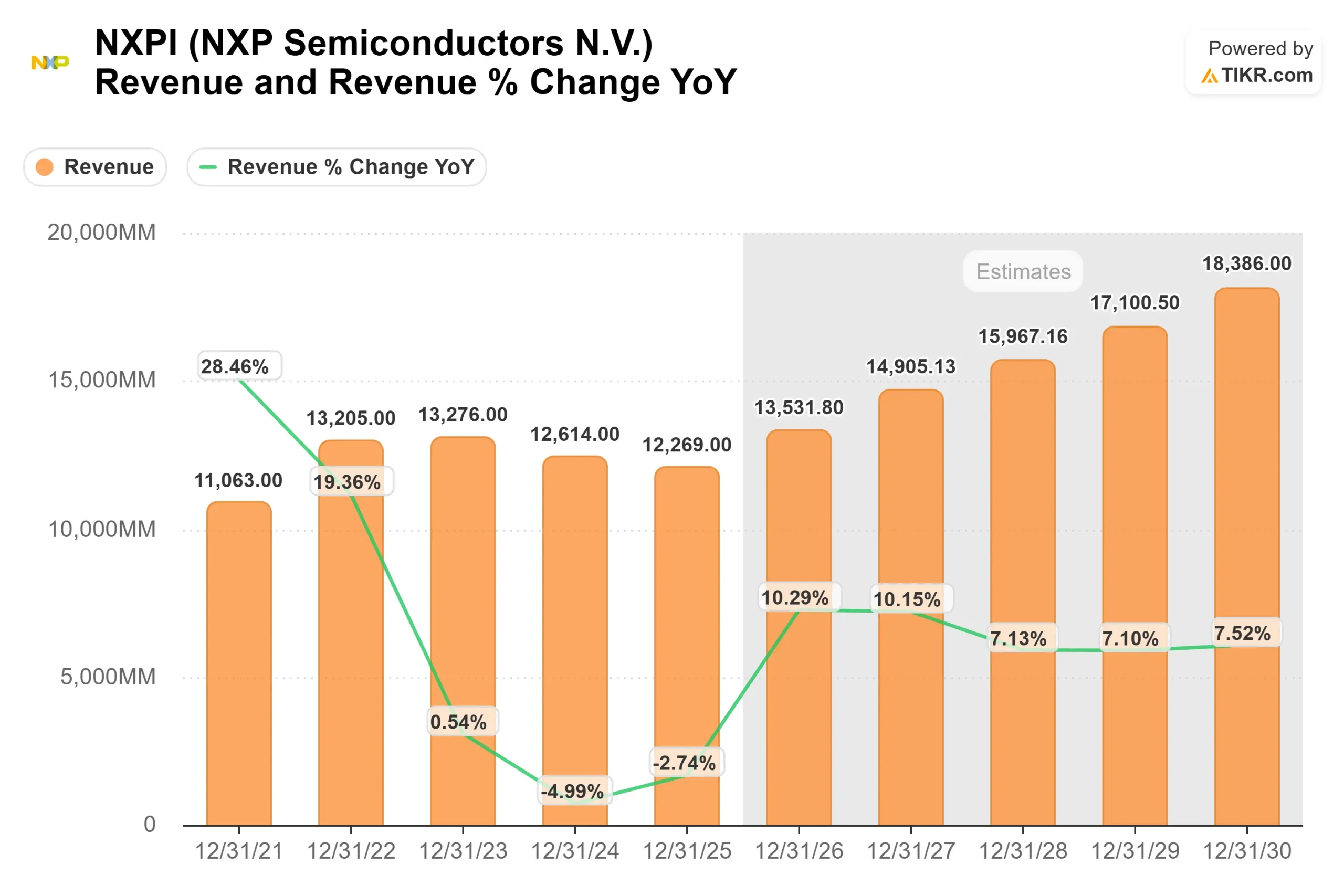

NXP reported Q4 2025 revenue of $3.34 billion, up 7% year-on-year and 5% sequentially, with non-GAAP operating margin of 34.6% in line with guidance and non-GAAP EPS of $3.35, which came in $0.07 above the midpoint.

Management guided Q1 2026 revenue to $3.15 billion, up 11% year-on-year and down 6% sequentially, and stated that all regions and end markets are expected to grow versus last year.

CEO Rafael Sotomayor said, “we believe the NXP-specific secular drivers for our business are now outweighing the broader industry cyclical headwinds.”

Analyst reactions were mixed but constructive. TD Cowen lowered its price target to $250 from $285 while keeping a Buy rating. Evercore ISI cut its target to $260 from $292 and maintained Outperform.

Citigroup reduced its target to $255 from $285 and kept a Buy rating, and Mizuho trimmed its target to $255 from $285 while maintaining Outperform.

At the same time, KeyCorp raised its target to $300 from $280 and kept an Overweight rating, while JPMorgan lifted its target to $250 from $245 with a Neutral stance. The Street average target now stands near $254, with a Moderate Buy consensus.

Institutional positioning remains strong. ProShare Advisors trimmed its stake by 18.3% in the third quarter, selling 78,404 shares and ending with 350,095 shares worth about $79.73 million, or roughly 0.14% of the company.

Envestnet Asset Management increased its stake by 1.7% to 337,265 shares valued at about $76.8 million, and institutional investors now own approximately 90.5% of NXP.

See analysts’ growth forecasts and price targets for NXP Semiconductors N.V. (It’s free) >>>

Is NXP Semiconductors Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 9.2%

- Operating Margins: 36.3%

- Exit P/E Multiple: 16.3x

Revenue growth expectations reflect a cyclical trough in 2024 and 2025 followed by reacceleration beginning in 2026.

Analyst estimates show revenue rising from $12.27 billion in 2025 to nearly $15.97 billion by 2028 and over $18.39 billion by 2030, implying a return to mid-to-high single digit growth as automotive content gains and industrial demand normalize.

Electrification, advanced driver assistance systems, automotive Ethernet, radar, and software-defined vehicle architectures continue increasing semiconductor content per vehicle. That allows revenue expansion even if global vehicle production remains flat.

Industrial and IoT momentum tied to edge processing, factory automation, healthcare systems, energy storage, and physical AI platforms broadens the growth base beyond traditional automotive cycles.

This supports the view that future returns depend more on content expansion, design win conversion, and mix improvement than on macro recovery alone.

Automotive accelerated growth drivers are returning to model levels after inventory digestion, and multiyear software-defined vehicle programs create structural revenue visibility.

Based on these inputs, the model estimates a target price of $361, implying about 53% total upside over roughly 2.9 years, or approximately 16% annually, indicating the stock appears undervalued at current prices.

At current levels, NXP appears undervalued, with future performance driven by structural semiconductor content growth, improving mix, and disciplined capital allocation rather than aggressive revenue acceleration.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>