Key Takeaways:

- AI Backlog Scale: Broadcom disclosed $73 billion of AI backlog scheduled over the next 18 months, positioning Broadcom’s custom XPU and AI networking portfolio as the primary growth engine into 2026.

- Enterprise Networking Expansion: Broadcom announced its first enterprise Wi-Fi 8 access point and switching platform on February 3.

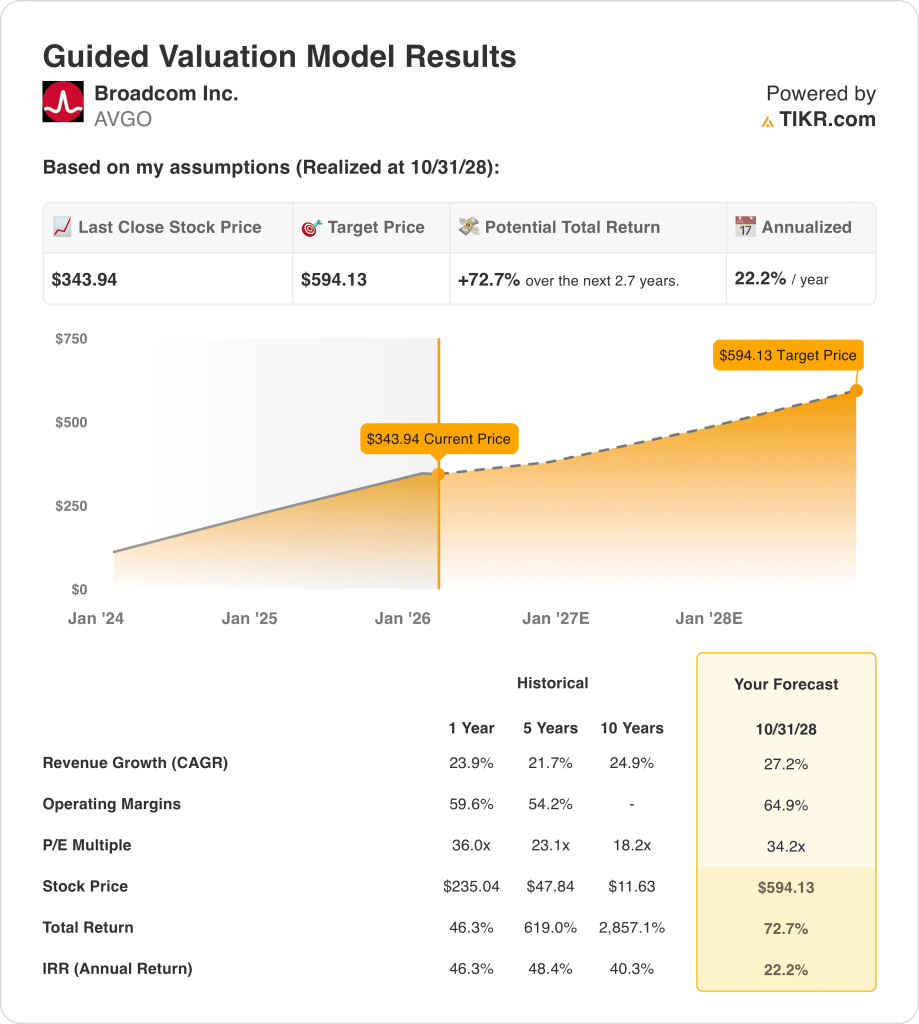

- Target Price Framework: Broadcom stock could reach $594 by October 2028 as the model underwrites 27% revenue CAGR through 2028, 65% operating margins, and a 34x exit P/E on scaled AI and software mix.

- Return Math: Broadcom’s $594 target implies 73% total upside from the $344 current price, translating to about 22% annualized returns over roughly 3 years if the margin and multiple assumptions hold.

Broadcom Inc. (AVGO) sells semiconductors and infrastructure software, supplying networking chips, custom accelerators, storage connectivity, and VMware-based cloud software to hyperscalers and large enterprises worldwide.

In fiscal 2025, revenue reached $64 billion with $37 billion from semiconductors and $27 billion from infrastructure software, while AI revenue hit $20 billion to anchor growth across data center compute and networking demand.

Also last year, Broadcom stock’s revenue reached $18 billion with 78% gross margins implying about $14 billion of gross profit, while $2 billion of operating expenses supported roughly $12 billion of operating income and a 66% operating margin.

Management guided fiscal Q1 2026 revenue of $19 billion, including $8 billion from AI semiconductors, with CEO Hock Tan stating, “Directionally, we expect AI revenue to continue to accelerate and drive most of our growth”.

Meanwhile, last week, the company introduced an enterprise Wi-Fi 8 access point and Trident X3+ switching platform, alongside capital returns including a $1 quarterly dividend of $1 per share annualized and $8 billion of repurchases remaining through 2026.

At $344 today versus a modeled $594 value by October 2028 based on 34x earnings and 65% operating margins, the key question is whether the market’s current 36x multiple already embeds the expected step-up in AI-driven growth through 2026.

What the Model Says for AVGO Stock

Broadcom’s dominant position across AI silicon and software platforms enables high earnings conversion, as fixed-cost leverage and limited incremental investment requirements amplify profit growth at scale.

The model assumes 27.2% revenue growth, 64.9% operating margins, and a 34.2x exit multiple, resulting in a $594.13 target price.

That outcome implies 72.7% total upside and a 22.2% annualized return, exceeding typical equity opportunity costs over the modeled horizon.

Based strictly on modeled returns and risk compensation, the valuation framework signals a Buy with capital appreciation as the primary outcome.

A 22.2% annualized return stands well above a standard 10% equity hurdle which offers sufficient compensation for execution and valuation risk and supporting a Buy focused on capital appreciation rather than preservation.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Broadcom stock:

1. Revenue Growth: 27.2%

Broadcom stock delivered 23.9% revenue CAGR over the past 1 year, and AI semiconductor demand accelerated while the infrastructure software base remained scaled.

Current execution rests on $73 billion of disclosed AI backlog, and AI semiconductor revenue reached $20 billion in fiscal 2025 as management guided acceleration into fiscal 2026.

The 27.2% growth assumption depends on uninterrupted hyperscaler spending and sustained XPU adoption, and downside emerges quickly if AI orders defer or networking demand slows.

This assumption exceeds the 1-year historical revenue growth of 23.9%, and the model therefore assumes acceleration rather than continuation of Broadcom’s recent growth profile.

2. Operating Margins: 64.9%

Broadcom stock has historically converted scale into profitability, producing 59.6% operating margins over the past 1 year through disciplined cost control and high gross margin software exposure.

Recent results show operating income of roughly $12 billion on $18 billion of quarterly revenue, supported by software margins above 90% and semiconductor margins near 68%.

The 64.9% margin assumption requires sustained operating leverage as AI system revenue scales, while cost creep from advanced packaging, system sales, or integration complexity would pressure margins quickly.

This is above the 1-year historical operating margin of 59.6%, indicating the model assumes incremental margin expansion rather than margin stability as the business scales.

3. Exit P/E Multiple: 34.2x

An exit P/E multiple capitalizes terminal earnings power, and it captures durability and maturity as it prices risk beyond the forecast period.

The model applies a 34.2x multiple to normalized earnings, and it embeds margin expansion and AI scale benefits within the earnings base rather than the valuation.

At the end of the forecast, earnings quality depends on AI revenue concentration and backlog conversion, and the multiple contracts if growth decelerates faster than expected.

This level sits above the NTM P/E market assumption of 33.51x, and the model assumes valuation stability because earnings already embed margin expansion and AI scale while customer concentration and system mix limit further multiple expansion.

What Happens If Things Go Better or Worse?

Broadcom stock results depend on AI infrastructure demand, enterprise software monetization, and management discipline through the 2030 forecast horizon.

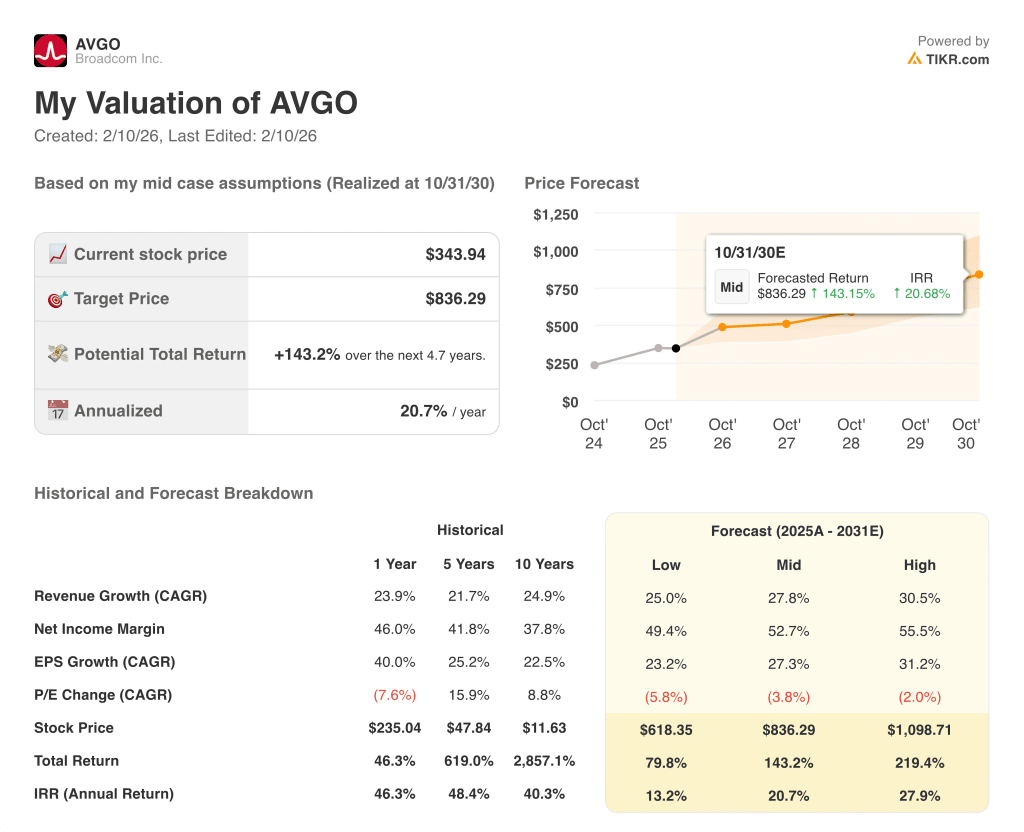

- Low Case: If AI orders normalize and software growth slows, revenue grows around 25% and margins hold near 49% → 13.2% annualized return.

- Mid Case: With AI demand sustained and VMware monetization steady, revenue growth near 27.8% and margins rise toward 52.7% → 20.7% annualized return.

- High Case:

How Much Upside Does Broadcom Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!