Key Takeaways:

- Exact Sciences Expansion: Abbott Laboratories gained German antitrust approval on January 30, 2026 for the Exact Sciences acquisition, adding a cancer diagnostics growth vector that supports management’s 7% 2026 organic sales framework.

- Libre Recall Overhang: Abbott Laboratories faced an FDA update on February 4, 2026 tied to FreeStyle Libre 3 removals, after Abbott reported 860 serious injuries and 7 deaths connected to the recall issue as of January 7, 2026.

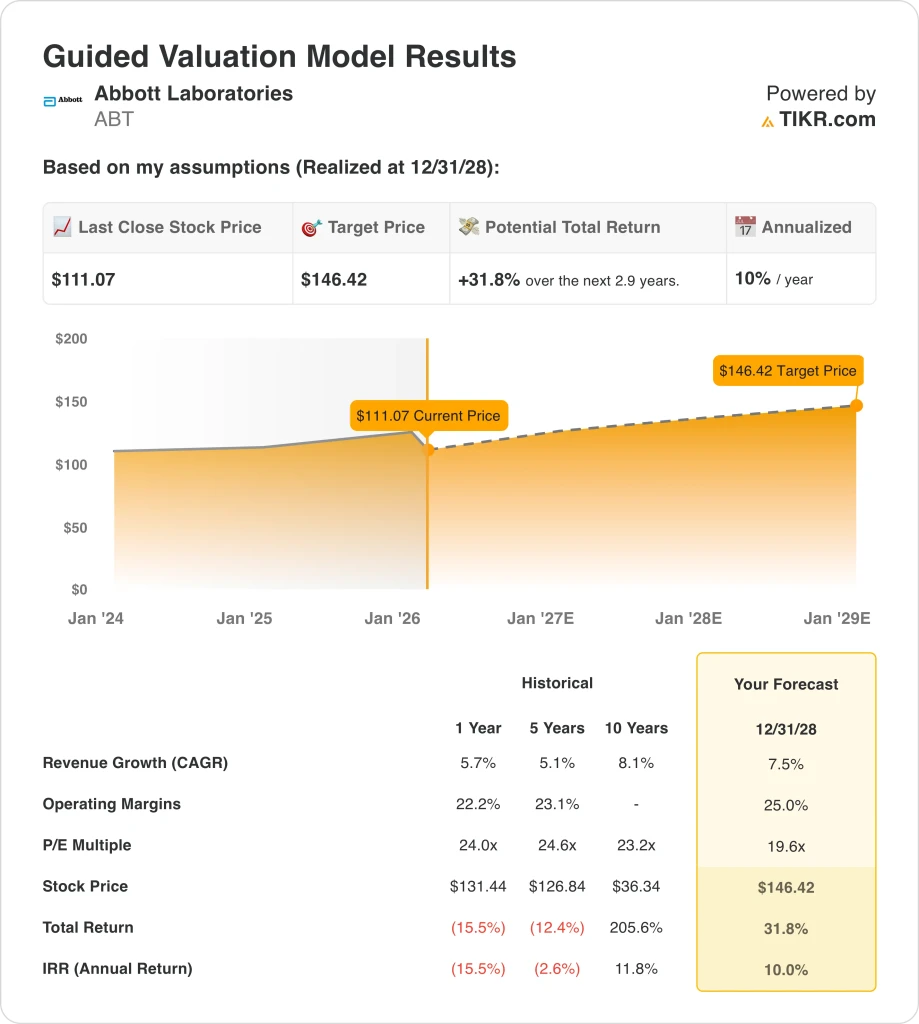

- Target Price Setup: Abbott Laboratories could reach $146 by 2028 if revenue compounds about 8% and operating margins scale to 25% while the exit multiple compresses to a 20x P/E as growth normalizes.

- Return Math: Abbott Laboratories implies 32% total upside from the $111 current price to the $146 target across roughly 3 years, translating to about 10% annualized returns under the model’s assumptions.

Abbott Laboratories (ABT) sells healthcare products across 4 divisions, spanning medical devices, diagnostics testing systems, nutrition brands, and established pharmaceuticals that serve hospitals, clinics, and consumers across 160 countries.

In 2025, revenue reached $44 billion and gross profit totaled $25 billion, reflecting a 57% gross margin that supports reinvestment while insulating earnings from mix and pricing pressure across multiple end markets.

At the same time. operating expenses were $17 billion and operating income was $8 billion, leaving operating margins near 19% and showing how cost discipline matters when top-line growth runs about 6%.

On the Q4 2025 earnings call, CEO Robert Ford said, “Path is not sustainable in the long term, so we began to make changes in the fourth quarter.”

Management guided about 7% organic sales growth and roughly $6 adjusted EPS for 2026, while targeting 50 to 70 basis points of annual operating margin expansion through gross margin lift and P&L leverage.

Meanwhile, last January 30,, Germany cleared the planned Exact Sciences deal with a February 20, 2026 shareholder vote pending which positions Abbott for a larger diagnostics footprint as COVID testing headwinds fade versus 2025.

Moreover, just last week, the FDA posted that Abbott Diabetes Care removed certain FreeStyle Libre 3 sensors after Abbott cited 860 serious injuries and 7 deaths, creating a reputational and execution test inside an $8 billion CGM franchise.

With the stock at $111 and the valuation model using a 20x 2028 P/E to reach $146, investors are left debating whether a 25% margin endpoint is conservative or aggressive as execution risks stay visible in 2026.

What the Model Says for ABT Stock

Abbott stock has large diagnostics and medical device businesses that generate steady cash, but slow-growing healthcare markets and the need for ongoing investment make strong upside harder to achieve.

The model assumes 7.5% revenue growth, 25.0% operating margins, and a 19.6x exit multiple, leading to a $146.42 target price by 2028.

That scenario results in 31.8% total upside and a 10.0% annualized return, which aligns with standard equity return expectations but does not reward added business and regulatory risk.

The model signals a Sell, as a 10.0% annualized return does not exceed the return investors typically demand for a company with Abbott Laboratories’ risk profile.

With returns only matching a typical 10% equity hurdle rate, the valuation favors capital preservation over meaningful growth, offering limited justification for incremental capital allocation under the model.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Abbott stock:

1. Revenue Growth: 7.5%

Abbott’s revenue expanded about 6% over the last year, reflecting a diversified healthcare mix where diagnostics and devices offset slower nutrition and pharma cycles.

Current execution is supported by mid-single-digit organic growth guidance for 2026, stabilization in diagnostics post-COVID, and sustained double-digit expansion in medical devices contributing most incremental revenue.

The forward path requires continued device adoption and successful integration of Exact Sciences, while slower nutrition recovery or regulatory disruption would quickly pull growth below modeled levels.

This is above the 1-year historical revenue growth of 6%, indicating that the model assumes modest acceleration despite Abbott’s mature end markets.

2. Operating Margins: 25%

Abbott stock delivered operating margins near 22% over the last year, showing steady efficiency gains but still carrying cost intensity from R&D, manufacturing, and regulatory compliance.

Current performance benefits from scale leverage, easing input costs, and management’s stated target of 50 to 70 basis points of annual margin expansion across gross profit and operating expenses.

Achieving 25% margins requires disciplined cost control and sustained pricing power, with downside emerging quickly if growth slows while fixed investment levels remain elevated.

This is above the 1-year historical operating margin of 22%, indicating that the model assumes continued efficiency improvement rather than margin stability.

3. Exit P/E Multiple: 19.6x

Abbott stock has traded near a 24x P/E over the last year because earnings remain stable and the medical device mix supports a valuation premium.

The exit multiple reflects a mature earnings base capitalized on net income, with the model already embedding margin expansion and steady growth rather than cyclical rebound or structural re-rating.

At 19.6x, valuation tolerance depends on consistent execution, as any earnings miss or regulatory setback would likely compress multiples rather than allow upside expansion.

This is below the 1-year historical P/E multiple of 24x, indicating that the model assumes valuation compression consistent with a more mature, normalized growth profile.

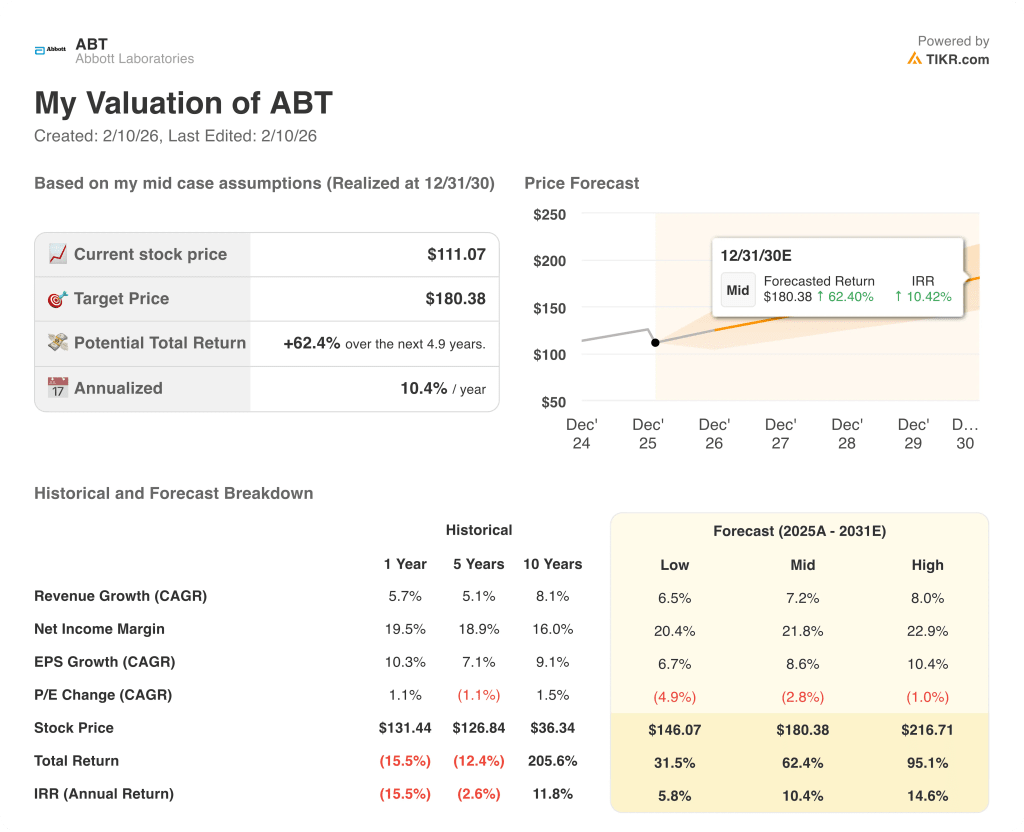

What Happens If Things Go Better or Worse?

Abbott stock outcomes depend on medical device execution, diagnostics stabilization, nutrition recovery, and management discipline, setting a range of paths through 2030.

- Low Case: If device momentum slows and nutrition lags, revenue grows 6.5% and margins hold near 20.4% → 5.8% annualized return.

- Mid Case: With core devices steady and diagnostics normalized, revenue grows 7.2% and margins rise toward 21.8% → 10.4% annualized return.

- High Case: If device adoption accelerates and cost control holds, revenue reaches 8.0% and margins approach 22.9% → 14.6% annualized return.

How Much Upside Does Abbott Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!