Key Stats for Williams Companies Stock

- Past-Month Performance: 12%

- 52-Week Range: $52 to $69

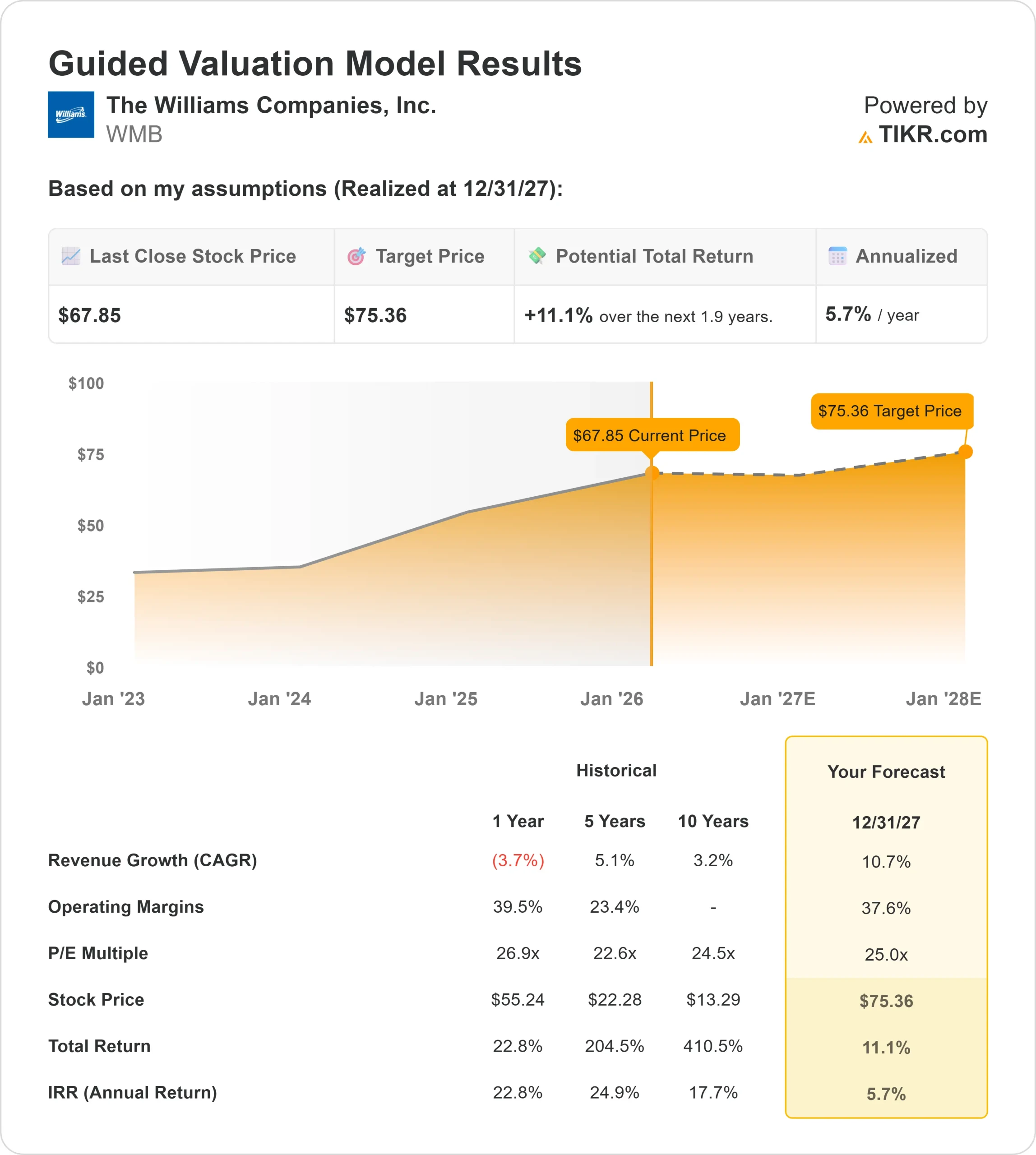

- Valuation Model Target Price: $75

- Implied Upside: 11%

Value your favorite stocks like Williams Companies with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

The Williams Companies, Inc. stock rose about 12% this month, finishing near $68 per share, as investors reacted to strong earnings execution, major strategic announcements, and renewed institutional buying. The move reflected growing confidence in Williams’ ability to convert rising U.S. natural gas demand into durable, fee-based cash flows through its pipeline and storage network.

Shares moved higher this month after Williams reported stronger operating momentum and reaffirmed full-year guidance, reinforcing confidence in earnings visibility.

The company posted third-quarter adjusted EBITDA of $1.92 billion, up 13% year over year, driven by record results in its Transmission, Power & Gulf segment as expansion projects came online and Gulf volumes surged.

Williams also reiterated its 2025 adjusted EBITDA midpoint of $7.75 billion, signaling that growth remains on track as new infrastructure enters service.

Management announcements added further momentum. Williams disclosed the $398 million sale of its Haynesville upstream asset to JERA and unveiled a fully contracted LNG and pipeline partnership with Woodside supported by 20-year take-or-pay contracts, shifting cash flows further toward long-duration, infrastructure-based earnings.

CEO Chad Zamarin said the strategy allows Williams to “high grade from upstream cash flows into high-quality pipeline and LNG terminal cash flows,” reinforcing the company’s shift toward more predictable returns.

Institutional activity also supported the stock during the month. Multiple funds increased positions in the third quarter, including Kinsale Capital, ALPS Advisors, Jones Financial Companies, BI Asset Management, M.D. Sass, and J.W. Cole Advisors, contributing to institutional ownership of roughly 86%.

That accumulation signaled growing conviction in Williams’ long-term infrastructure strategy and helped sustain the stock’s upward move.

See analysts’ growth forecasts and price targets for Williams Companies (It’s free) >>>

Is Williams Companies Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 10.7%

- Operating Margins: 37.6%

- Exit P/E Multiple: 25x

Revenue growth expectations reflect improving pipeline utilization as expansion projects come online and demand continues to pull volumes through Williams’ system.

Growth is supported by rising LNG exports, increasing power generation needs tied to data centers, and incremental throughput across Transco and Gulf Coast infrastructure rather than exposure to short-term commodity pricing.

Earnings durability is reinforced by Williams’ fee-based contract structure, where a large portion of cash flows are backed by long-term take-or-pay agreements.

That setup allows higher volumes and new projects to translate into steadier cash generation instead of cyclical swings, supporting margin stability even during periods of natural gas price volatility.

Based on these inputs, the valuation implies a target price of about $75, suggesting roughly 11% total upside over the next two years, indicating the stock appears undervalued at current levels.

Results over the next year hinge on execution across several high-impact areas. Expansion projects along Transco, incremental storage capacity additions, and tighter pipeline corridors in the Gulf Coast and Southeast regions support volume growth and earnings visibility as demand continues to rise.

At the same time, disciplined capital allocation and balance sheet management allow Williams to fund growth projects while sustaining dividends.

At current levels, Williams appears undervalued, with future performance driven by infrastructure utilization, project execution, and long-term natural gas demand rather than short-term market sentiment.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>