Key Takeaways:

- AI Transformation: Salesforce’s Agentforce platform has closed 18,500 deals since launch, with 9,500 paid transactions.

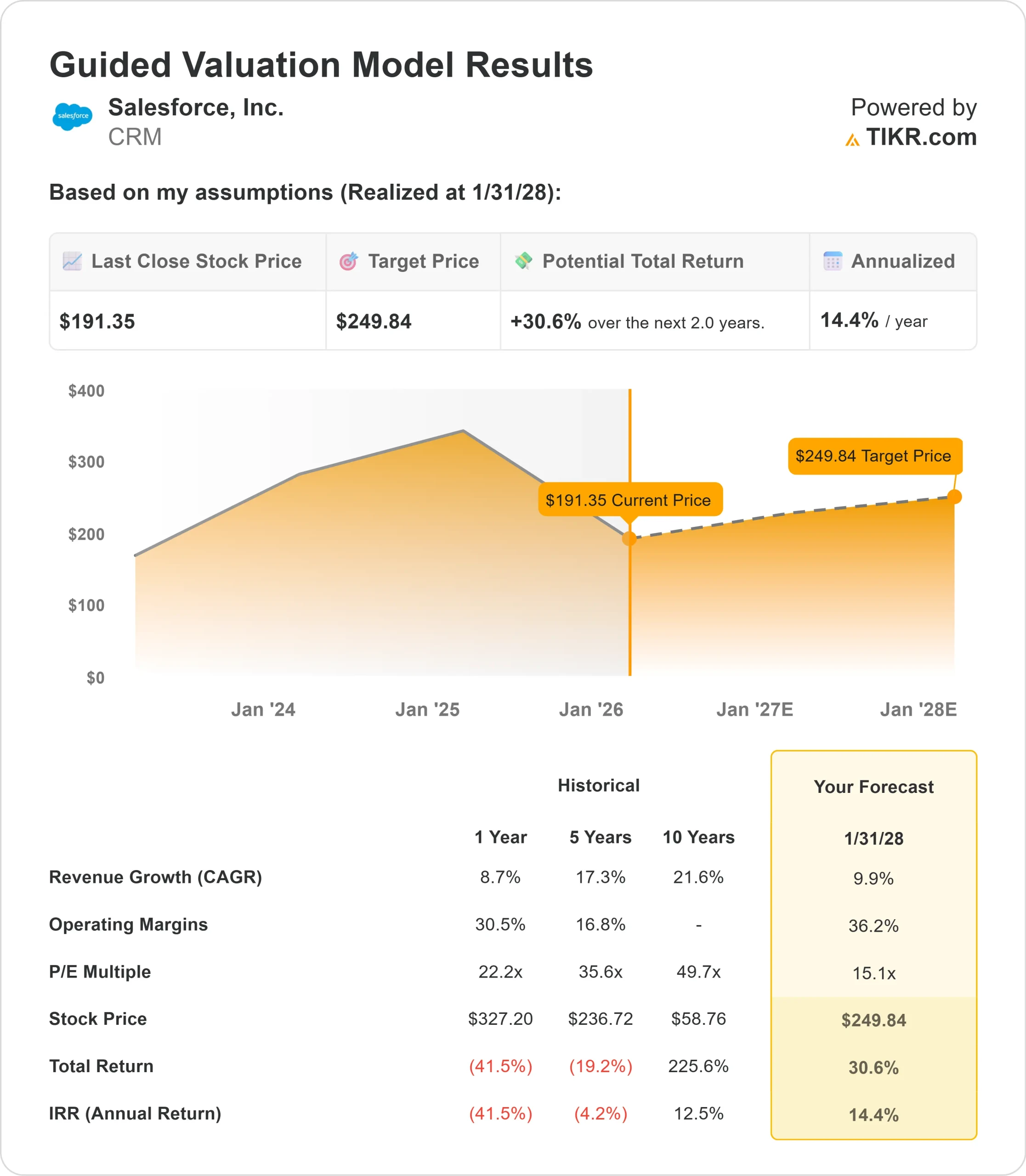

- Price Projection: Based on current execution, CRM stock could reach $250 by January 2028.

- Potential Gains: This target implies a total return of 31% from the current price of $191.

- Annual Return: Investors could see roughly 14% growth over the next 2 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Salesforce (CRM) delivered strong third-quarter fiscal 2026 results that exceeded expectations, driven by the explosive adoption of its Agentforce AI platform.

Revenue grew 9% year-over-year to $10.26 billion, while current remaining performance obligation (cRPO) jumped 11% to $29.4 billion.

CEO Marc Benioff highlighted the company’s transformation into what he calls the “agentic enterprise,” where AI agents work alongside humans to drive productivity gains.

- Agentforce has processed over 3.2 trillion tokens through Salesforce’s large language model gateway, with October alone seeing 540 billion tokens, up 25% month-over-month. Token usage is a direct measure of AI adoption, and no other enterprise software company matches these numbers.

- The company’s AI and data business, which includes Agentforce and Data 360, generated nearly $1.4 billion in annual recurring revenue (ARR), up 114% year over year.

- Agentforce reached $540 million in ARR, up 330% year over year. More tellingly, customers in production with Agentforce increased 70% quarter over quarter, signaling real adoption beyond pilot programs.

- From Sales Cloud to Service Cloud, Slack to Tableau, each application now includes autonomous agents that can reason, learn, and take action.

- Companies like Williams-Sonoma have deployed customer service agents to handle 60% of chat interactions, while the IRS has automated 98% of manual activities in its Chief Counsel office, reducing case processing time from 10 days to 30 minutes.

- The acquisition of Informatica, completed three months ahead of schedule, strengthens Salesforce’s data foundation.

- Combined with Data 360 and MuleSoft, this creates a $10 billion data infrastructure business that delivers accurate, real-time information to AI agents. In Q3 alone, Data 360 ingested 32 trillion records, up 119% year-over-year.

Perhaps most important for future growth, Salesforce increased sales capacity by 23% this year while training the entire sales force on Agentforce.

This investment in distribution capacity, combined with flexible pricing models ranging from per-conversation fees to enterprise license agreements, positions the company to capture demand as customers move from AI experimentation to production deployment.

Major wins in Q3 included CVS Health, General Motors, Costco, and TD Bank. GM is now scaling Slack across 96,000 employees in just 9 months while using Agentforce across automotive cloud, data, and service operations.

Life Sciences Cloud bookings tripled year-over-year as Salesforce takes market share from competitors, with 120 industry leaders selecting the platform in recent months.

See analysts’ full growth forecasts and estimates for CRM stock (It’s free) >>>

What the Model Says for Salesforce Stock

We analyzed Salesforce as it transforms from a traditional CRM vendor into an AI platform company powering the agentic enterprise.

The company benefits from multiple expansion drivers: core cloud growth, AI agent adoption, data platform monetization, and new markets like IT service management.

Management expects to reaccelerate revenue growth within 12 to 18 months as Agentforce adoption scales.

For the first time since fiscal 2022, net new annual contract value (ACV) growth outpaced total ACV growth in Q3, indicating improving business quality.

Using a forecast of 9.9% annual revenue growth and 36.2% operating margins, our model projects the stock will rise to $250 within 2 years. This assumes a 15.1x price-to-earnings multiple.

That represents significant compression from Salesforce’s historical P/E averages of 22.2x (one year) and 35.6x (five years). The lower multiple reflects a conservative stance, as the market awaits full monetization of AI and Agentforce’s ability to sustain triple-digit growth.

The real value lies in Salesforce’s unique position, combining enterprise-grade customer data, proven applications, and AI capabilities that customers cannot easily replicate.

Early adopters who tried building proprietary AI solutions are now returning to platforms like Salesforce after discovering the complexity of enterprise AI deployment.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CRM stock:

1. Revenue Growth: 9.9%

Salesforce’s growth centers on Agentforce adoption among its 150,000 customer base. The company closed over 18,500 Agentforce deals in its first year, with 362 customers already refilling consumption tanks in Q3 alone, compared to just 3 customers two quarters earlier.

More than 50% of new Agentforce and Data 360 bookings came from existing customers expanding their investments.

As companies realize they cannot build enterprise AI in-house, Salesforce captures wallet share through multi-cloud deals, with 70% of top wins involving five or more clouds.

2. Operating margins: 36.2%

Salesforce delivered 35.5% non-GAAP operating margin in Q3, up 240 basis points year-over-year. The company has steadily improved profitability while investing heavily in AI and sales capacity.

CFO Robin Washington emphasized continued focus on operational efficiency, noting that internal Agentforce deployments are already driving productivity gains.

As Customer Zero, Salesforce’s own sales development agent has worked hundreds of thousands of leads, generating tens of millions in incremental pipeline.

3. Exit P/E Multiple: 15.1x

The market currently values Salesforce at 22.2x earnings. We assume modest P/E compression to 15.1x as the company proves out its AI strategy.

This conservative multiple accounts for execution risk in scaling Agentforce and potential customer caution around AI spending.

As revenue reacceleration becomes evident and AI contributions become more transparent, Salesforce should command a premium multiple given its position as the leading enterprise AI platform.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

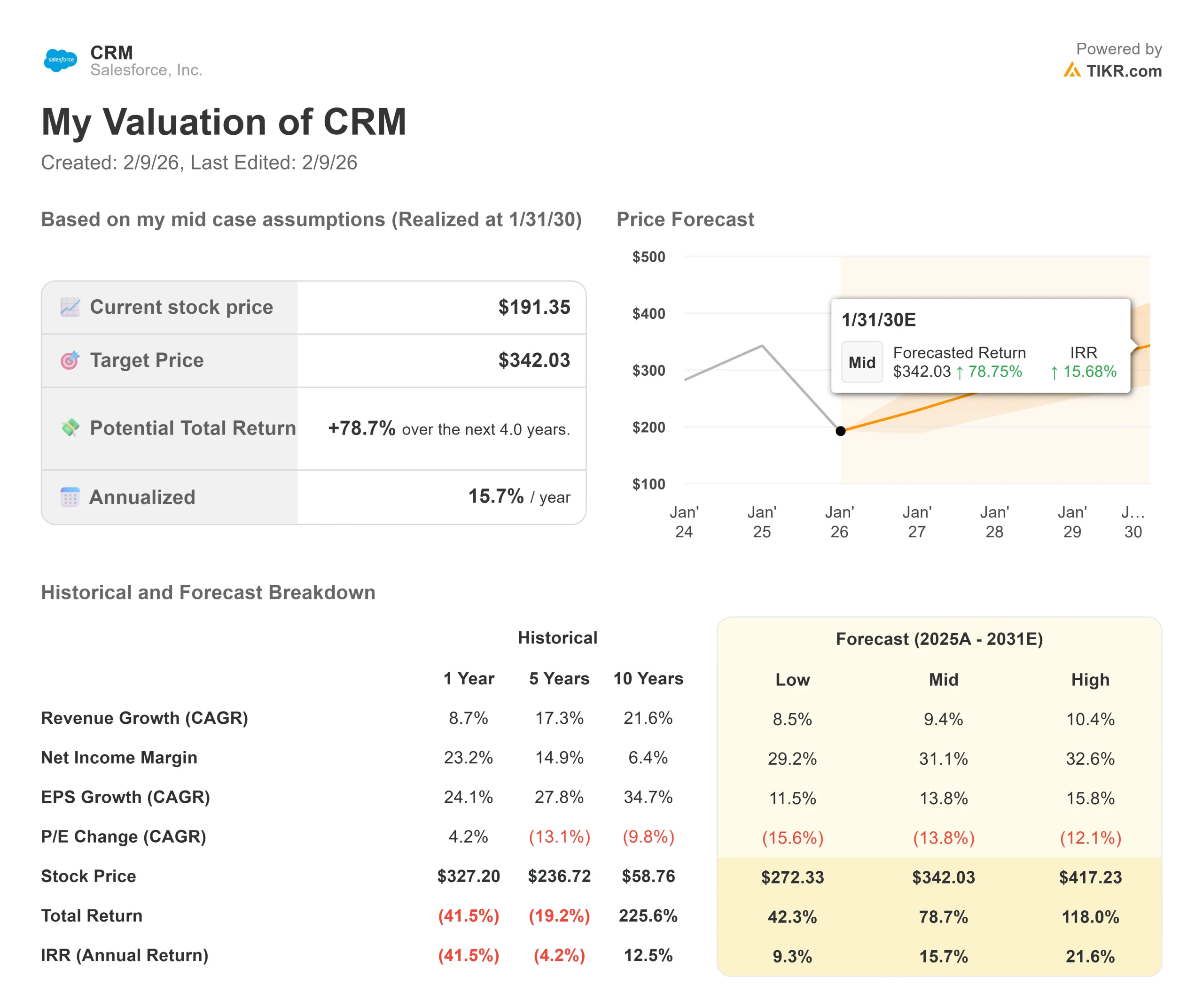

Enterprise software faces economic cycles and technology transitions. Here’s how Salesforce stock might perform under different scenarios through January 2030:

- Low Case: If revenue growth moderates to 8.5% and net income margins compress to 29.2%, investors still see a 42.3% total return (9.3% annually).

- Mid Case: With 9.4% growth and 31.1% margins, we expect a total return of 78.7% (15.7% annually).

- High Case: If Agentforce adoption accelerates to drive 10.4% revenue growth while Salesforce maintains 32.6% margins, returns could hit 118.0% total (21.6% annually).

See what analysts think about CRM stock right now (Free with TIKR) >>>

The range reflects execution on AI agent deployment, successful navigation of consumption-based pricing, and the company’s ability to monetize its data platform.

In the bear case, customers slow AI spending, or competitors gain traction.

In the bull case, the agentic enterprise becomes the dominant enterprise computing paradigm with Salesforce as the clear platform leader.

How Much Upside Does Salesforce Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!