Key Takeaways:

- Regulatory Overhang: Netflix faces heightened scrutiny in 2026 as U.S. regulators review the proposed Warner deal, introducing execution risk alongside Netflix’s 2025 revenue growth of nearly 16%.

- Strategic Positioning: Netflix’s expanding global content slate and pricing discipline support net income margins above 30% in the mid-case, reinforcing scale advantages despite antitrust pressure.

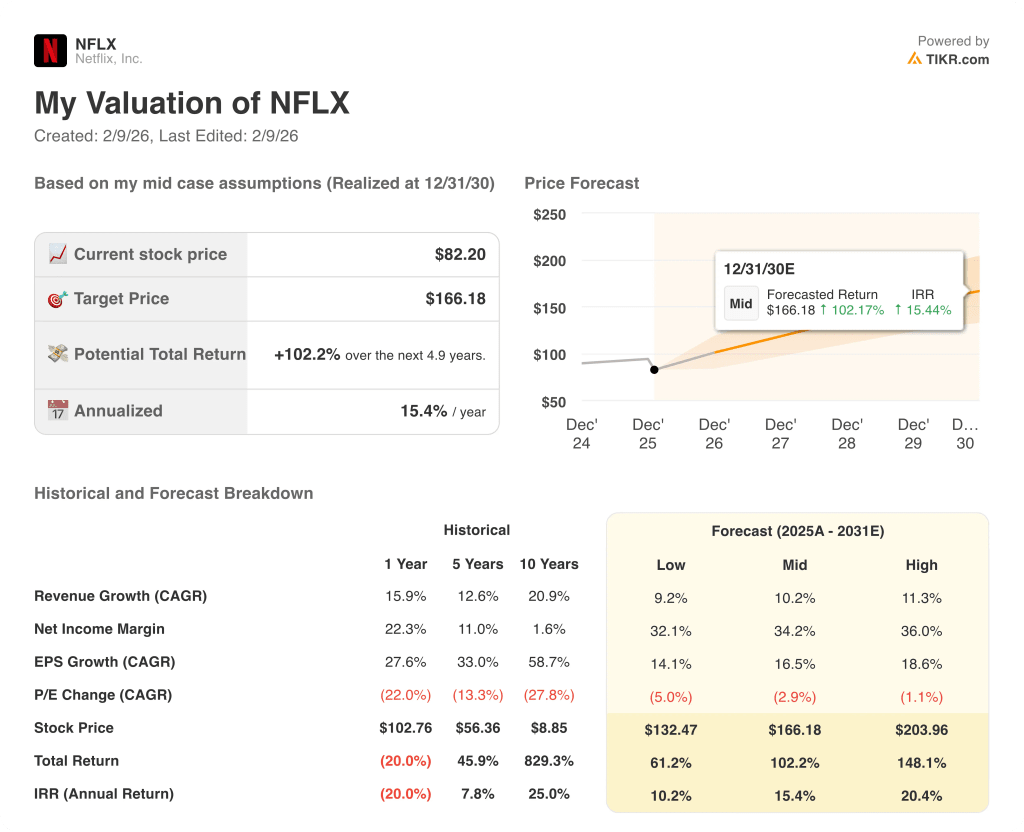

- Price Target: Based on 10% revenue growth, 34% net margins, and multiple normalization, Netflix stock could reach $166 by 2030 under the mid-case framework.

- Return Profile: The $166 target implies 102% total upside from the $82 price today, translating into a 15% annualized return for Netflix investors.

Netflix, Inc. (NFLX) is a global subscription-based entertainment company that monetizes original and licensed content across TV, film, games, and live programming, generating $45 billion in revenue in 2025 from more than 190 countries.

In 2025, Netflix generated $22 billion in gross profit, held operating expenses near $32 billion, and delivered operating income of $13 billion, lifting operating margins to nearly 30%.

This margin expansion followed strong pricing execution and subscriber growth, with revenue increasing 16% year over year and normalized net income reaching $11 billion.

Strategically, Netflix entered 2026 at the center of industry consolidation debates, as Warner Bros. Discovery reaffirmed confidence in regulatory approval for a Netflix merger rejected by 93% of shareholders in a rival $108 billion Paramount bid.

Regulatory attention intensified when the U.S. Justice Department opened an investigation into whether Netflix engaged in anticompetitive behavior tied to the proposed transaction.

The company framed its position clearly during the dispute, with a Netflix co-chief stating that only a “very small” number of Warner shares supported Paramount’s offer.

The stock now reflects a tension between a business compounding earnings above 15% annually and a valuation reset driven by antitrust uncertainty, leaving the path to $166 by 2030 dependent on execution rather than sentiment.

What the Model Says for NFLX Stock

Netflix’s global scale, high content leverage, and limited incremental capital needs support elevated expectations despite regulatory scrutiny and industry consolidation pressures.

The model assumes 10.2% revenue growth, 34.2% net margins, and exit multiple compression of 2.9%, producing a $166.18 target price by 2030.

The 102.2% total upside and 15.4% annualized return exceed typical opportunity costs and compensate for regulatory, execution, and competitive equity risk.

The model signals a Buy, as a 15.4% annualized return surpasses equity hurdle rates and supports capital appreciation under disciplined valuation logic.

With a modeled 15.4% annualized return above a typical 10% equity hurdle, the valuation compensates for regulatory and execution risk, favors capital appreciation over preservation, and justifies a Buy based on risk-adjusted capital allocation discipline.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Netflix stock:

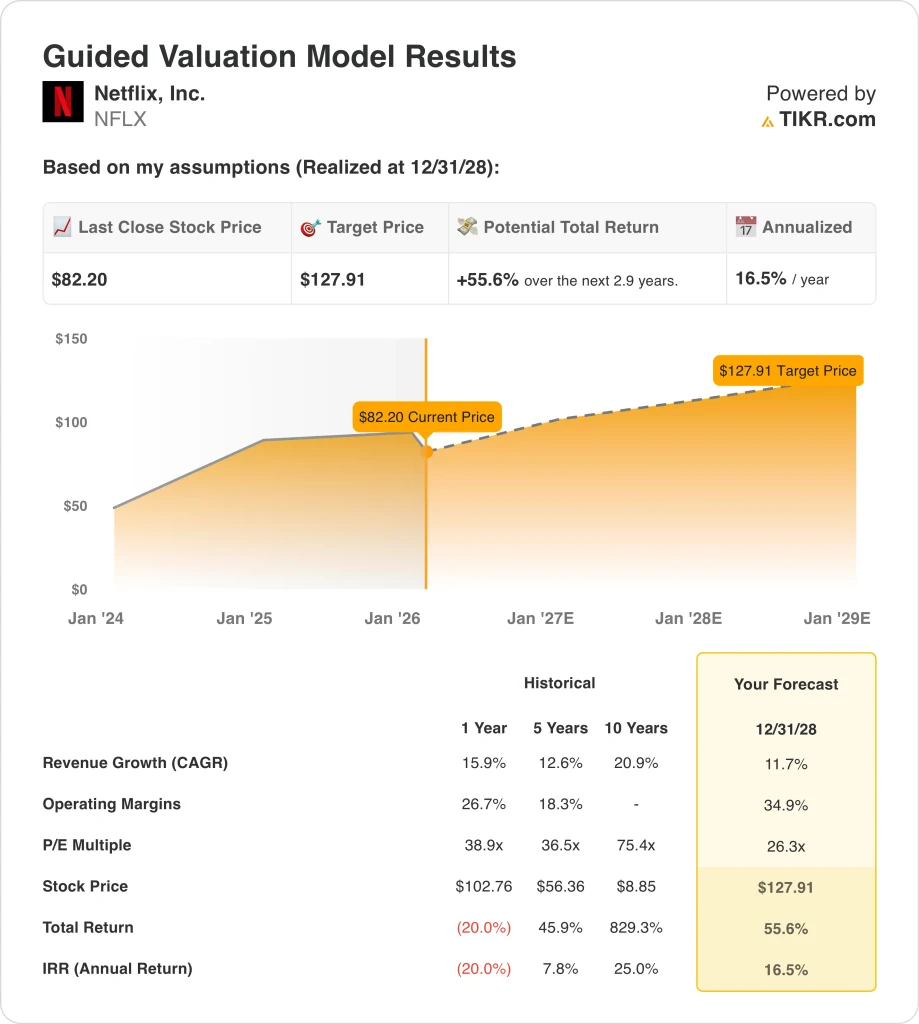

1. Revenue Growth: 11.7%

Netflix stock’s revenue grew 16% over the last year as subscriber growth, pricing actions, and advertising traction offset a maturing North American streaming base.

Current execution reflects revenue of $45 billion with double-digit growth supported by ad-tier scaling, password-sharing enforcement, and steady international subscriber additions.

Sustaining 11.7% growth requires continued ad monetization and content efficiency, while weaker engagement or pricing resistance would pressure topline momentum quickly.

This is below the 1-year historical revenue growth of 16%, indicating the model assumes moderation consistent with scale and global streaming maturity.

2. Operating Margins: 34.9%

Netflix stock’s operating margins expanded to 27% last year as content amortization discipline and revenue leverage improved profitability across regions.

Current results show operating income of $13 billion and margins near 30% which are all supported by slower content spend growth and rising average revenue per user.

Reaching 34.9% margins requires tight content budgeting and stable subscriber churn, while higher production costs or competitive bidding would erode margin progress.

This is above the 1-year historical operating margin of 27%, indicating the model assumes further efficiency gains rather than cost reinvestment acceleration.

3. Exit P/E Multiple: 26.3x

The 26.3× exit multiple capitalizes durable earnings from a scaled global platform with predictable subscription cash flows and lower capital intensity.

The model already embeds margin expansion and revenue growth, which limits justification for multiple expansion beyond normalized large-cap media valuations.

Any disappointment in subscriber growth or regulatory pressure would compress the multiple quickly, as valuation support rests on sustained execution rather than sentiment.

This is below the 1-year historical P/E of 39×, indicating the model assumes valuation normalization rather than re-rating despite improved profitability.

What Happens If Things Go Better or Worse?

Netflix stock paths depend on subscriber monetization, advertising scale, content discipline, and regulatory outcomes, setting up divergent execution-driven results through 2030.

- Low Case: If subscriber monetization slows and content costs stay rigid, revenue grows 9.2% with margins near 32.1% → 10.2% annualized return.

- Mid Case: With ad-tier traction and controlled spending, revenue grows 10.2% and margins reach 34.2% → 15.4% annualized return.

- High Case: If advertising scales efficiently and engagement stays strong, revenue grows 11.3% and margins approach 36.0% → 20.4% annualized return.

How Much Upside Does Netflix Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!